Resource Roundup Part 1: Metals

A special thanks to Darrel for inviting me to be a guest on the Vancouver Resource Investment Conference YouTube Channel. To organize my thoughts, and so any new subscribers can find past material more easily, I am creating this resource roundup.

The Commodity Supercycle:

But first I wanted to check in on the main thesis for why I have been spending so much time over the last year looking at resource companies:

The idea of a commodity supercycle is that years, or even decades, of underinvestment into material extraction leads to a period where commodity prices are high, and resource owners make outsized profits for as long as it takes to bring on new supply. Not to get too far into the weeds, but this is probably caused by low interest rates. I know that seems counterintuitive because low interest rates are supposed to stimulate investment, but it only does so for the longest and shortest time horizon projects, usually tech and real estate. Materials investments usually have about a ten year time horizon, the resource deposits might be quite large, but the plan is to only spend to prove enough resources as are needed for the next ten years. If you talk to mining CEO’s, they reminisce that they got a lot done in the early 2000’s, and it was all at a 9% cost of borrowing. When interest rates were even lower, mining companies didn’t expand. Friedrich Hayek called this phenomenon “both ends pulling against the middle,” as only the longest term and shortest term projects get funded.

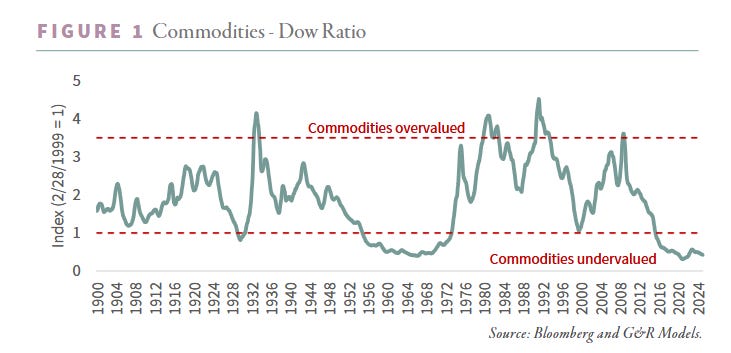

We did have fifteen years of zero interest rate policy (ZIRP), so when is this commodity supercycle showing up? A lot of my mining stocks feel like they have already started taking off, but it’s probably not too late to add more as this is a very long cycle and will take years if not decades to correct. But the real party might not even have started, you can see from the chart below, commodities stayed undervalued compared to the Dow from around 1954 to 1974. This current period of suppressed commodity valuations only started around 2014.

But not every type of commodity had underinvestment during ZIRP. Shale oil, being a short time horizon investment, was stimulated, and we are still suffering the hangover. If energy does have years of outperformance, it won’t be for the same reasons as copper or coking coal. Energy might have years of outperformance, not because energy was underinvested in for years, but because shale decline rates are so steep. I’m not saying there won’t be an energy boom, and I am heavily invested in energy personally, but it isn’t a prime candidate for the commodity supercycle. And the lower prices have driven painful sector outflows, which have been excruciating these last two years.

Other things that are not prime candidates for the commodity supercycle are resources that can have their supply increased quickly. Things that can be mined in-situ such as lithium are not ideal. This includes, blasphemous to say it, uranium. The supply restriction on uranium mining is due to local government permitting, shortages of skilled labor, and perhaps management failures, but not the physical speed at which new uranium mines can be brought online, as compared to copper or platinum mines. It might be the case that uranium prices can stay high for a year or two or three, but it probably can’t have the sustained high prices that metals like copper and platinum have the potential to obtain. I do still own a couple of uranium companies, but in my mind the miners are short term holdings.

The King of Commodities:

In my mind, the absolute king of commodities is gold. This is because not only are new mines slow to bring online, but the stockpile of gold represents so many years of production. Precisely because gold is not an industrial metal, and it is used as a competing money, there is around 212,000 metric tons of gold in circulation. But only about 3,650 metric tons of gold were mined last year. In other words, current annual production would double the gold stockpile in a bit under sixty years. For platinum, annual production is greater than current stockpiles.

What this means is that the ability of miners to oversupply the gold market is almost non-existent, but the ability of miners to eventually oversupply the platinum market is pretty much guaranteed. The number of years for which miners can enjoy high prices could be much longer for gold than for any other metal. It will probably be the case that the demand for gold will revert back to historical norms before the supply of gold mined adjusts enough to suppress the price.

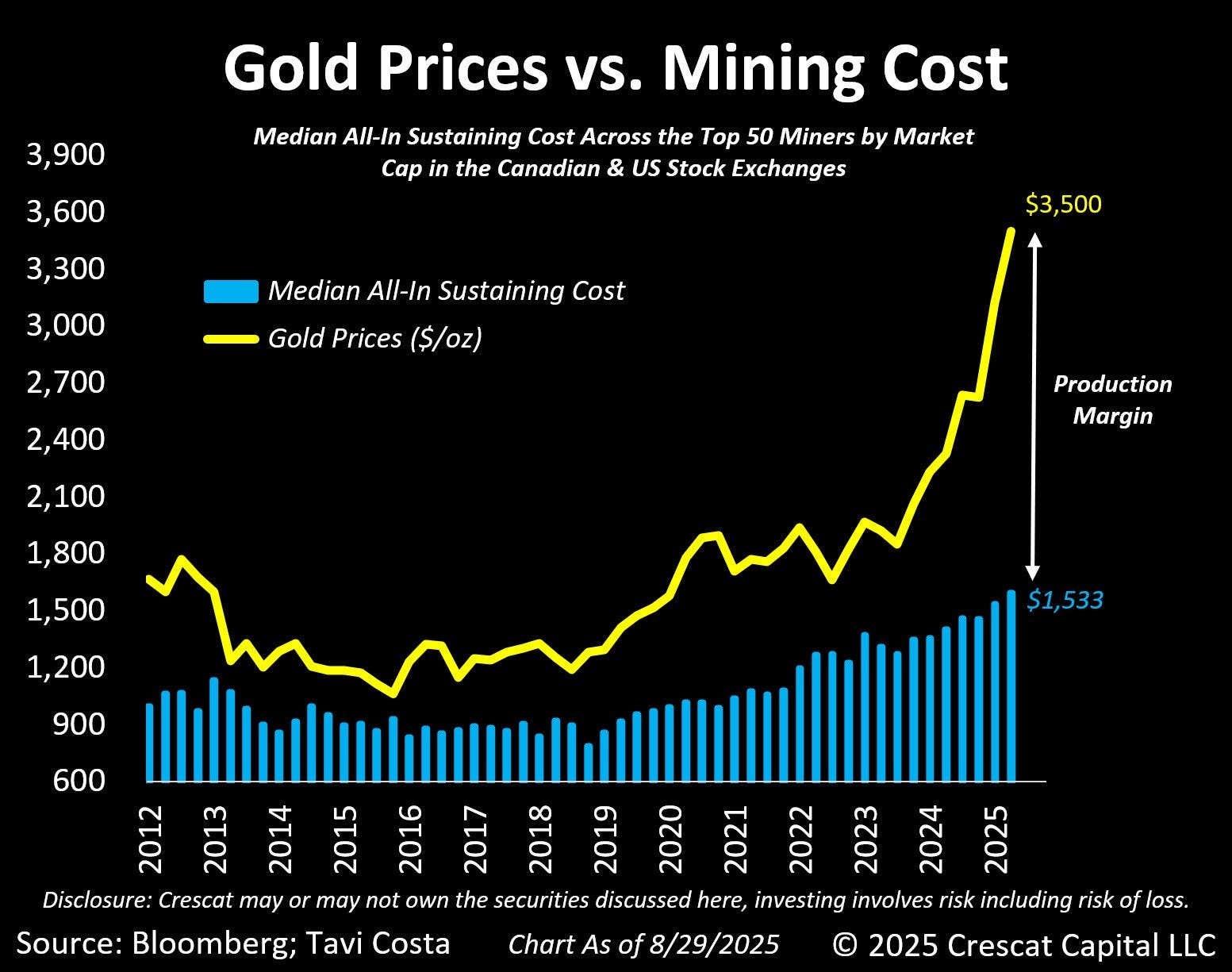

But investors have been scarred from investing in gold miners in the past. This is because past gold cycles were driven by costs rising, while this current rally is driven by demand rising. When the price of gold is pushed up by rising costs, the miners don’t have outsized profits, but when the price of gold is pulled up by demand, they do.

This current gold price rally is being driven by central bank demand for gold. Gold is being used as a central bank reserve asset due to the world transitioning from having a single superpower to having a rivalry between the US and China. In this multipolar world, there is increased demand for a reserve asset that is unaligned with either superpower. And at the current pace, central banks have many years left to go to accumulate the reserves they need. Even now, portfolio managers are still underweight gold, and there hasn’t yet been a retail frenzy.

My primary gold miner is Equinox (EQX), and you can find my writeup from 2024 here:

Why I chose Equinox Gold $EQX for my gold exposure.

I am devoting a part of my portfolio to gold because gold, oil, and land outperformed the last time we had sustained inflation and sustained inflation is very likely while congress is running a deficit of 7% of GDP. Also, when the US confiscated Russian financial reserves, the entire global south started looking for an alternative for international set…

I have written about several other gold miners as well, but my current focus is on three junior miners with excess mill capacity, as they can increase production at a much lower cost than their peers.

The three junior gold miners with the most growth potential (Paywalled)

The price of gold is in an interesting place right now. While I had thought there would be a pullback, it has instead chosen to chop sideways. Technical analysis is never my strong suit, but I have seen it happen often enough that when volatility compresses, it then breaks out one way or another. The volatility of the gold price movements has been compressing, and should give us an answer whether it will break up or down, probably within the next few weeks.

My Largest Commodity Exposure:

While gold is the king of commodities, my largest exposure is with my strongest thesis. I was not entirely certain that central bank gold buying would be this strong. But I have enormous confidence that platinum group metals will be dramatically undersupplied at some point in the next however many years.

It wasn’t very long ago that the consensus was that we would all be driving electric cars within the next decade. I fell for it as well, until I scratched the surface. The nickel demand, and the electricity demand for transitioning to battery electric vehicles meant that any sort of near term transition was impossible. The CEO of Toyota, Akio Toyoda, was correct, the consumer of today wants hybrids, and hybrids are likely to be the dominant consumer choice for ten or twenty years. Although vindicated later, Akio was still forced to step down as CEO, it’s hard for one man to stand against a narrative, even a false one.

But hybrids need 15% more catalysts in their catalytic converters than internal combustion vehicles. Not only is it not the case that we don’t need platinum group metals anymore, but we need more platinum group metals than ever. This became my largest commodity exposure because it was the contrarian thesis I had the most confidence in. To find value there has to be disagreement, and in platinum group metals there was significant disagreement.

My platinum miner of choice is Sibanye Stillwater (SBSW), my writeup on them can be found here:

Why I love Sibanye Stillwater $SBSW, and thus I hate myself. (Reprise)

Today’s crosspost idea comes from Hugo Navarro at Undervalued and undercovered who just did a writeup on Sibanye Stillwater (SBSW). I started my original writeup on SBSW as follows:

I also looked into a platinum tailings company, Sylvania Platinum (SLP.L), and what is very interesting about both SBSW and SLP.L is that they have the highest concentrations of rhodium in their peer group. You can read more about why I think rhodium is important here:

Another Mud Pumper: Sylvania Platinum $SLP.L $SLP; Elegy for Stillwater, Catharsis for Sibanye $SBSW

Once again the market has taken Sibanye Stillwater (SBSW) out to the woodshed, and I am reminded of the AI poetry with which I started my first writeup on SBSW; “I love Sibanye Stillwater, and Thus I Hate Myself.” I think I knew that the bottom wasn’t in yet when I started the article in this way, and I am not a skilled enough trader to catch the bottom, so instead I catch the falling knife.

The Safest Bet in Metals:

The most consensus metal must be copper. Everyone knows and everyone agrees that the electrification of everything, the AI electricity demand, the growth in consumption in the global South all point to needing more copper. I made a two part series and decided that the copper miners for me were Hudbay Minerals (HBM), and Taseko Mines (TGB).

Niche Metals:

There are other metals that are interesting, some have military uses, some have uses in electronics. They are all fun, but none are certain enough to hold such a large weight in the portfolio as gold, platinum, or copper. Here are some past writeups on various niche metals:

What’s the Best Silver Strategy? Andean Precious Metals $APM.V or Sprott Physical Silver $PSLV

I haven’t written about silver yet, it’s a complicated metal, part industrial, and part monetary. Not completely dissimilar to platinum, but with its own unique quirks.

Tin Baron or Tin Barren: Alphamin Resources $AFM.V $AFMJF, Metals X $MLX.AX $MLXEF

Hey ChatGPT, create a version of “If I Only Had the Nerve,” but make it about Alphamin Resources (AFM.V).

A Canadian Nickel Junior Rollup: Magna Mining $NICU.V

When I start to look at a company, it’s not always immediately obvious what other people are so enthusiastic about. But when a savvy investor such as Brandon Beylo at Macro Ops tells me their number one pick, I spend the time to dig a little deeper.

Chinese Export Controls and Penny Dreadfuls: Almonty Industries $AII.TO, Fireweed Metals $FWZ.V, Taseko Mines $TGB

In December of 2024, China banned the export of germanium, gallium, and antimony. In February of 2025, China put export restrictions on tellurium, indium, tungsten, molybdenum, and bismuth. The export of those last five elements are possible with a special permit.

Coming soon for part II: Energy

There are reasons to be bearish uranium mid term, but I’m not sure greenfield uranium mines can be brought to production quickly is one of them.