Chinese Export Controls and Penny Dreadfuls: Almonty Industries $AII.TO, Fireweed Metals $FWZ.V, Taseko Mines $TGB

In December of 2024, China banned the export of germanium, gallium, and antimony. In February of 2025, China put export restrictions on tellurium, indium, tungsten, molybdenum, and bismuth. The export of those last five elements are possible with a special permit.

While it is possible that Trump delivers some sort of grand Mar-a-Lago accord with China, and those export restrictions are removed, it is also possible that this cutting off of critical minerals progresses. What would be the next step? A complete ban on the recent five? If new export controls are placed, which materials would be most likely to be targeted in the future?

It might be possible to skate to where the hockey puck is going, but one of the nice things about small cap stocks is that there are often stragglers who miss the initial move so that less nimble investors such as myself can find them.

Gallium and Germanium:

Ramaco Resources (METC, METCB) have a large deposit of rare earths that are particularly rich in gallium and germanium, although it will be several years until first commercial production.

Why are there Windmills on their Homepage?: Ramaco Resources $METC $METCB

Hello and welcome back to “Coal, the new whale oil.” For a quick refresher on the macro thesis, feel free to check out the first in the series.

Antimony:

For paying subscribers, the antimony exposure was discussed here:

Paywalled Small Cap Gold Mining Stock with a Stealth Antimony Asset

Thanks to Premski_SGP for turning me on to this one. I am usually happy to give away my own ideas for free, but I think Premski is still building his position, so I’ll go ahead and hide this one behind the paywall.Value Degen’s Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Bismuth:

Bismuth isn’t so much mined as extracted as a smelting byproduct, so our environmental regulations that sent smelters abroad have sent our bismuth production abroad as well. Fortunately, our ally Japan still smelts. Unfortunately, I couldn’t find any small cap stocks with good bismuth exposure. Oh well, stocks aren’t Pokémon, I don’t need to catch ‘em all.

Indium and Tellurium:

Indium and Tellurium are rare elements, and there aren’t any North American mines in development, however, there are some explorers with proven deposits who are just waiting to be acquired by a developer. I do not like “penny dreadfuls” as Rick Rule calls them. This is not the kind of company that I like to buy, but they might be a fun lottery ticket for someone else.

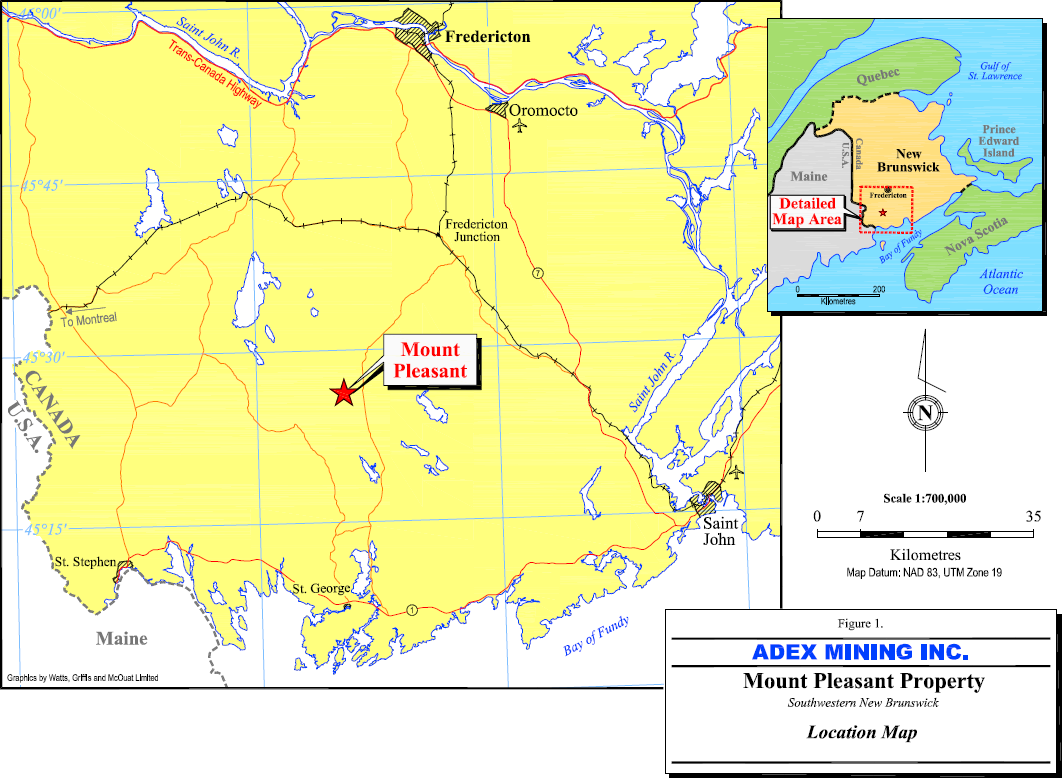

Adex Mining (ADE.V) controls the Mount Pleasant Mine in New Brunswick, Canada, the world’s largest proven indium reserve, which is also a tungsten, molybdenum, tin, and zinc deposit. Some pre feasibility studies were done in 2014, and not much has changed since then. They haven’t even updated their website in a decade.

American West Metals (AW1.AX) has a much more modern website than Adex, with an investor presentation as recent as last quarter. American West owns the fully permitted West Desert deposit in Utah, with proven reserves of 23.8 million ounces of Indium. Now they are probably waiting for the right acquirer or joint venture partner to develop it. This is only one of three ore bodies that American West controls, so it might not be their top priority. But now that the export controls are in place, it might get some attention.

First Tellurium Corp (FTEL.CN) is yet another explorer stage junior miner with an amazing deposit, and no plan or ability to develop it. In this case there are two tellurium deposits, Deer Horn in British Columbia, and Klondike in Colorado. Again, not my favorite style of investing, but if you are a North American tellurium enthusiast, this is your only option.

Teck Resources (TECK) produces some indium as a byproduct of its zinc mining operations. But at a $21 billion market capitalization, even if indium prices were to triple, it wouldn’t make much of a difference to TECK’s earnings.

Boliden (BOL.ST) is a Swedish base metals miner who is actively mining tellurium already. Unfortunately, with a market capitalization of over $8 billion, even if tellurium prices were to triple, it wouldn’t make much of a difference to Boliden’s earnings either.

Tungsten:

Unlike the previous metals, Tungsten has a small cap miner that is in current production: Almonty Industries (AII.TO). One of my subscribers was even nimble enough to buy some shares on the European exchanges before Americans woke up to the news of the export controls. The stock is up from 1.20 CAD to 1.76 CAD in three trading days. Congratulations, I am not that nimble.

Almonty, at first glance, is not much without the export controls, 27 million CAD trailing twelve month revenue for a 620 million CAD enterprise value company. Long term debt of nearly 4x revenue, and not a single quarter of profitability within the last 18 months. The CEO owns 10% of the company, which is a plus, and they are building out a second mine in South Korea to go with their original Portuguese asset.

Sangdong mine in South Korea is likely to be a game changer for Almonty. It is the largest inferred tungsten deposit ever discovered, and Almonty has an offtake agreement with a price floor, but no ceiling for 15 years. Production is scheduled to start in Q1 of 2025, and it is projected to generate $24 million CAD of annual cash flow while in stage 1, but of course that is at past tungsten prices. Estimated cash costs per mtu (10kg) are $110, and with the $235 floor on the offtake agreement, that would represent about $64 million of new annual revenue, about tripling Almonty’s trailing twelve month numbers. Sangdong is projected to ramp up to $300 million annual revenue and $64 million annual cash flow at the offtake floor prices by 2027.

The current FOB tungsten price is $296, well above the $235 price floor. Where that price will go is anybody’s guess, antimony prices tripled after the export ban. At $400 / mtu tungsten, the Sangdong mine adds $66 million of cash flow in stage 1, and $140 million annual cash flow in stage III by the end of 2027.

I have to say, with the huge price runup in the last few days, I thought I might have missed my chance, but Almonty is a solid opportunity even at today’s prices. At the current price floor, the market capitalization is about 5x 2027 cash flows, but at $400 tungsten, that’s 3x cash flows, and at $500 tungsten, Almonty is trading at 2x 2027 cash flows. The 15 year offtake agreement with a price floor provides a significant derisking, making Almonty a very asymmetric investment. Looking farther ahead, there are still two more development properties, as well as a synergistic molybdenum deposit in Sangdong. I would be happy to buy some shares at the current price if I weren’t prioritizing the paywalled antimony miner at the moment.

Tungsten has many more penny dreadfuls than indium and tellurium, but the one that stands out from the rest is Fireweed Metals (FWZ.V). Fireweed is very interesting with an 18% ownership stake by the Lundin family, and Adam Lundin as the chairman, despite operating in the Northwest Territories’ “moose pasture.” The current CEO was from Filo Corp, which just successfully sold itself to the Lundin family for $4.5 billion. Fireweed has two deposits, the first is zinc, silver, gallium and germanium, and the second is tungsten. Fireweed claims that their tungsten, while only about 60% the size of Sangdong, is almost double the grade. A final investment decision is targeted for early 2028. In my original writeup on copper, I argued that often the best thing to do is just to piggyback along with experts who have a successful history. At a 289 million CAD market capitalization, a similar $4.5 billion sale to the Lundin family would be a 20x, minus whatever dilution is necessary to get there from here.

How to punt into copper exploration like a muppet if you are late to the party: Ivanhoe Electric $IE, Filo Corp $FIL

If you haven’t heard about the copper thesis, you have likely been living under a rock. Former head of commodities at Goldman Sachs, Jeff Currie, has called copper the best trade of his career. Stanley Druckenmiller says copper is in the tightest position he’s ever studied.

Molybdenum:

Molybdenum is interesting because the US is not really all that short on it. Moly is often found as a byproduct of copper mining, and since the US only recently deindustrialized, and the average age of our copper mines is about 75 years old, we still have quite a few in operation. We may have sent our smelting capacity to Japan and South Korea, but we still have more than a few copper mines putting out 30% of the worlds’ molybdenum.

That said, any metal can be subject to a squeeze if there is tight demand and supply is inelastic. Moly is used to add strength to steel so that less of it can be used, which means that as steel prices rise in the next cycle, so will moly prices. But, most copper mining is done by the larger mining companies, leaving relatively few interesting junior miners in the moly space. Copper mines are notoriously slow to build, so the supply of molybdenum should be relatively inelastic, but the demand is anybody's guess.

I was shocked to find out that I already owned one of the highest torque moly producers, Taseko Mines (TGB). Taseko’s flagship Gibraltar mine is a copper / molybdenum project, although Taseko rarely mentions this, and one has to dig pretty deeply to even find molybdenum mentioned in their press releases. Last quarter, TGB brought in about $10 million in revenue from their moly byproduct, and operating income was only $19 million. If moly prices doubled, TGB’s net income would have a lot of responsiveness to that price change.

The primary reason I have been buying a bit of TGB recently is that their Florence in-situ copper mine should be coming online later this year, with another year to fully ramp up production. If the market looks about six months ahead, then I am hopefully buying just before the market notices. If the small cap is overlooked, then the stock price won’t respond until cash flows start coming in from the Florence project.

Taseko also owns a large niobium deposit, and unlike the penny dreadfuls, Taseko has the cash flow and mining expertise to do something about it themselves.

There is also, of course, Greenland Resources (MOLY.NE), who’s stock price has nearly doubled since the betting market started pricing in a Trump victory last September. The only thing worse than a junior mining exploration company is a junior mining exploration company whose price has already doubled as a meme stock. But perhaps Trump will acquire Greenland and promote spending on the Greenland economy and mineral extraction. Stranger things have happened.

The future:

Thinking ahead to where the hockey puck is going next, if China keeps on escalating export bans, there are a lot of potential metals that could be affected. I asked different large language models with several different prompts, and here is the answer, which it hopefully didn’t hallucinate.

Very High Probability of Export Ban:

Neodymium, Dysprosium, Terbium, Lithium, Cobalt, Graphite / Graphene, Silicon Carbide

Moderate Probability of Export Ban:

Titanium, Zirconium, Nickel, Tin, Vanadium, High Purity Polysilicon, Platinum Group Metals

Interestingly enough, I already have some small allocation to several mining stocks that have exposure to some of those potential export ban beneficiaries:

Neodymium - exposure through IDR, UUUU,

Dysprosium and Terbium - exposure through IDR

Lithium - exposure through SBSW

Cobalt - small exposure through NICU.V

Graphite

Silicon Carbide

Titanium - exposure through UUUU

Zirconium - possible exposure through UUUU

Nickel - exposure through NICU.V

Tin - exposure through MLX.AX

Vanadium - exposure through UUUU

Polysilicon

Platinum Group Metals - exposure through SBSW

I have not yet started a position in MLX.AX, although I have written about them. As for the rest, the bingo card is not completely filled out, nor does it need to be. Financial goals can be reached without investing in everything.

My primary goal until their earnings call at the end of February is to add to my antimony miner. After that, I still have this nagging sensation that Burford Capital (BUR) will reach a deal with Argentina within 2025, and now TTEC could announce “deal or no deal” any week.

But after those more urgent capital allocation needs, I would be happy to add to my positions in TGB, UUUU, NICU.V, IDR, and possibly start a position in MLX.AX. My position in SBSW is pretty much at the maximum allocation. If the prices haven’t moved away from me, I am considering starting a position in Fireweed and Almonty as well. There is a lot to choose from, and once again, I have more ideas than capital.

Nice writeup, but how did you come up with the 4.5bn analogy for the sale of FWZ to the Lundins? Is it simply looking at the filo sales price? Or have you actually compared the resources and businesses? FWZ seems like the obvious and sensible thing for the US and Canada to provide a concessional loan to if they want to establish a western world W supply, as the US has done with the sweet loan to Perpetua, but the threat of tariffs between the US and Canada complicated things.

Oh, since people here seem to like royalty companies, worth mentioning that elemental Altus picked up a royalty on the mactung deposit, so if you buy EAR for a largely Au/Cu royalty exposure, you get a secret W bonus.