Why I love Sibanye Stillwater $SBSW, and thus I hate myself. (Reprise)

Crosspost Community

Today’s crosspost idea comes from

at who just did a writeup on Sibanye Stillwater (SBSW). I started my original writeup on SBSW as follows:Hey ChatGPT, dunk on Sibanye Stillwater (SBSW) in the style of “A Lover’s Complaint” by Sir Thomas Wyatt.

I mine for gold, yet find but empty stone,

In wealth's pursuit, the depths bring only strife.

I delve and dig, yet riches stay unknown,

And in their place, but echoes of a life.

The earth, she groans beneath my weighty tread,

Her veins, once pure, now bleed a poisoned flow.

I seek prosperity, but find instead

The bitter taste of dreams laid low.

With every stroke, I chase a fleeting gleam,

Yet shadows grow, and hopes begin to fade.

The promised wealth is but a distant dream,

And in its place, the cost of choices made.

Sibanye's halls are filled with empty cheer,

A golden lure that hides the tarnished truth.

For in the quest for gain, there's naught but fear,

And in its wake, the loss of wisdom's youth.

Thus I bemoan, in tones both sharp and sweet,

A miner's plight, where earth and sky compete.

For all I sought, in grandeur's fleeting light,

Is lost, as I wage war through day and night.

In shadows deep, I find my heart's own blight,

As Sibanye’s promise fades to darkest night.

I desire to perish, and yet I ask health;

I love Sibanye Stillwater, and thus I hate myself.

You can find my original writeup here:

Why I love Sibanye Stillwater $SBSW, and thus I hate myself.

Hey ChatGPT, dunk on Sibanye Stillwater (SBSW) in the style of “A Lover’s Complaint” by Sir Thomas Wyatt.

And you can find Hugo’s new writeup here:

If you want the TLDR (Too Long; Didn’t Read) thesis, Platinum Group Metals (PGMs), platinum, palladium, and rhodium are used in catalytic converters, and those commodities suffered as the electric vehicle narrative became zeitgeist, high interest rates suppressed automobile sales, and a flood of Russian palladium to fund the Ukraine War all coincided to destroy PGM prices. But, as I first learned from Trader

, hybrid vehicles use about 15% more PGMs than traditional internal combustion vehicles, and for at least the next couple of decades, battery electric vehicles are likely to take a back seat to hybrids. We are now in a global interest rate cutting cycle, which should buoy automobile sales. And with a potential end to the Ukraine War, Russia can go back to stockpiling Nornickel’s palladium until the next time they need to crack open the piggy bank. Things could be setting up nicely for a rebound of PGM prices once the pent up stockpiles are worked down. Year to date, both Platinum and Palladium are up over 10%, but that is off of a very low base, and the three major PGM miners are still losing money at these prices.The CEO of Sibanye Stillwater just announced his upcoming retirement sometime later this year. Neal Froneman gets a lot of hate on Twitter, probably because the stock price has fallen. But I believe he is an excellent negotiator. The acquisition of 50% of DRDGOLD (DRD) with SBSW’s tailings, and 40% of Neo Energy Metals (NEO.L) with their uranium deposit represent an incredible level of skill. There aren’t many people who know how to make a deal by giving away something of low value to themselves, and ask for a lot of something of low value to the other person, but get an enormous amount of value. Without patting myself on the back too hard, I predicted the NEO.L acquisition pretty accurately:

Why DRDGOLD $DRD is the blueprint for how Sibanye Stillwater $SBSW will handle its 60 million pounds of uranium reserves.

DRDGOLD (DRD) is the 50% owned subsidiary of Sibanye Stillwater (SBSW), and it processes the tailings of various South African gold mines in order to extract their proven reserves of 5.79 million ounces of gold. A tailings dump is the pile of crushed rock left behind after a mine has been operating for decades, and they can be enormous.

With a change in management comes the potential for a change in strategy. As SBSW has so many components, lithium, zinc, gold, platinum group metals, PGM recycling, battery recycling, and even a claim on a copper deposit in Tasmania, a lot of value could be unlocked by spinning off certain segments. It remains to be seen if the new CEO feels this way. The old theory was that South Africa could be a bridge between the East and West, and that SBSW could play both sides. Also, by being 1/3 gold, 1/3 PGMs, and 1/3 battery metals, something would always be up while the others were down. These last two years, everything has been down together, and now South Africa’s government appears to be a bit more kleptocratic, so maybe both theories have been falsified. I’m not holding my breath for a spinoff, but a lot of value could be unlocked that way. Alternatively, if everything has been down together, perhaps we will enter a period where everything is up together, PGMs, lithium, zinc, and gold, all high at the same time. Those earnings would rip everyone’s faces off.

In my original writeup on SBSW, I was highly critical of their ESG approach, but in hindsight, this was a mistake. In the US, ESG is a wasteful luxury, but in the 3rd world, it is a necessary part of life. If SBSW didn’t build schools and libraries in their local communities, then the locals wouldn’t help keep an eye out for the organized crime syndicates which steal copper wire. When the locals have nothing to start with, you have to give them something to lose in order to align incentives. This isn’t necessary in the developed world.

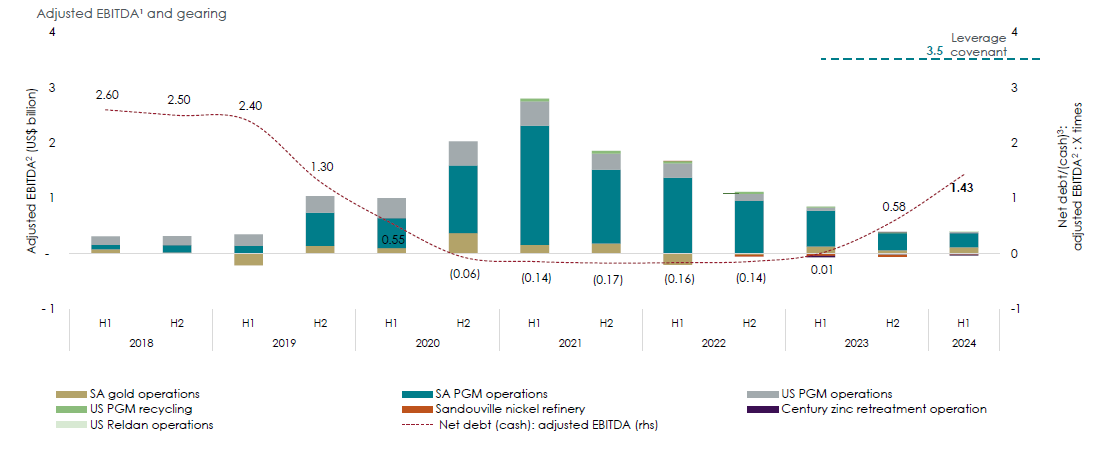

Sibanye Stillwater currently sits at a market capitalization of $2.7 billion. That’s about $2.25 billion for SBSW when you remove the value of their 50% stake in DRDGOLD. That is a cheap company. That is approximately the exact amount of their 2021 GAAP net income. And 2021 was before the buildout of the lithium mine, the acquisition of the zinc mine, and the recent acquisition of a complementary platinum recycling company, Reldan. In 2021, at that peak revenue, SBSW had an $18 stock price, today it sits at $3.83. In 2021, the gold mining production wasn’t adding much to SBSW’s EBITDA. Now that the gold price is hovering around $2,900 an ounce, those 600,000 ounces per year will likely add another $400 million of annual EBITDA. If you value SBSW only on their gold production at $2,900 per ounce gold, you get a market capitalization to EBITDA of 5.6x, not terribly expensive. And this is a company that had over $2 billion of EBITDA from PGMs in 2021.

I don’t know what else to say, it’s a bundle of cyclical commodities, and the thing about cyclical commodities is that you want the ones with the balance sheet to survive the down cycle. In this instance, SBSW de-levers in good times, and re-levers in bad times. In other words, they do exactly what they are supposed to do. Good times will come again, and I can’t tell you if that will be in 2025, 2026, 2027, or later. But when those good times come again, SBSW will probably see a $25 stock price on a year with $3 billion of net income. I think management nailed it on an earnings call a few quarters ago, PGMs are just such rare and useful metals.

As far as why someone should choose SBSW over their other PGM competitors, well, the other thing about cyclical commodities is that the high cost producers have the most torque. SBSW’s stock price fell more than their competitors one the way down, and it will rise relatively more than their competitors one the way back up. It is true that SBSW sold some royalty streams to Franco Nevada in order to raise cash during this downturn. Personally, I would have preferred if they didn’t build out Europe’s largest lithium mine, I think greenfield projects in mining are foolish when a company can buy so much so cheaply at the bottom of the cycle. But the Zinc mine acquisition and the Reldan acquisition were excellent.

For SBSW’s three major South African PGM mines, they acquired them for $1.5 billion, those mines have since generated $10.4 billion in EBITDA, but $1.8 billion was plowed back into them in maintenance capex. That leaves $8.6 billion of cash flow since 2016 on a $1.5 billion initial investment in 8 years. It is genuinely hard to 5x your money in 8 years, but Neal Froneman did it with Sibanye Stillwater. His retirement is well deserved. My only complaint is that lithium mine, and it still just might come back and surprise me.

There is another potential catalyst for platinum specifically, pun intended. As the price of gold ratchets higher and higher, a lot of hard money enthusiasts are preparing for silver, the poor man’s gold, to catch up. Historically, silver rallies after gold, but it rallies to a larger degree, the silver market is smaller, and has the greater capacity to squeeze. As we see the platinum price now at nearly 1/3rd of the gold price, something might upset past patterns. I think it is very possible that this time around, platinum could become the poor man’s gold instead of silver. The US has become so wealthy, GDP per capita of over $60,000 in Arkansas, that when people can’t afford a $4,000 or $5,000 ounce of gold, they might prefer to buy an ounce of platinum rather than to lug around a kilogram of silver. This time, silver might not squeeze the same way it did in the 1980 or in 2011. This time it might be platinum that squeezes, especially now that Costco is selling it.

For perspective, several hundred million ounces of silver are mined every year. About 80 to 100 million ounces of gold are mined every year, and about 5 million ounces of platinum are mined every year. If $4,000 gold causes Costco customers to trade down, not to silver but to platinum, the platinum price could catch up to gold incredibly rapidly. And if it does, SBSW’s all in sustaining cost won’t really matter much in the grand scheme of things as a $2,200 platinum price would add an additional $1 billion of annual EBITDA.

Is it really so far-fetched to think that platinum won’t spend a few years above $2,200 an ounce? It spent several years above $1,500 an ounce from 2010 to 2013, and $2,200 an ounce is just an inflation adjustment of the 2010 platinum price.

So I still hold my SBSW, about 3% of my portfolio. They don’t have a clean balance sheet. Their assets are a bit of a Frankenstein’s monster. South Africa is a political basket case. But I am happy with my purchase, and now I wait.

Sibanye Stillwater (SBSW) $3.83: $25 by end of year 2027

| A guest post by

|

Order a Portillos Italian beef sandwich, lie down in bed for a couple of hours and the urge to buy SBSW will soon pass.

Good reminder about the operating leverage of high-cost miners to a rising price. In addition to valuing miners on cash flow multiple, ever considered them as NPV of P&P reserves?