A Canadian Nickel Junior Rollup: Magna Mining $NICU.V

When I start to look at a company, it’s not always immediately obvious what other people are so enthusiastic about. But when a savvy investor such as Brandon Beylo at Macro Ops tells me their number one pick, I spend the time to dig a little deeper.

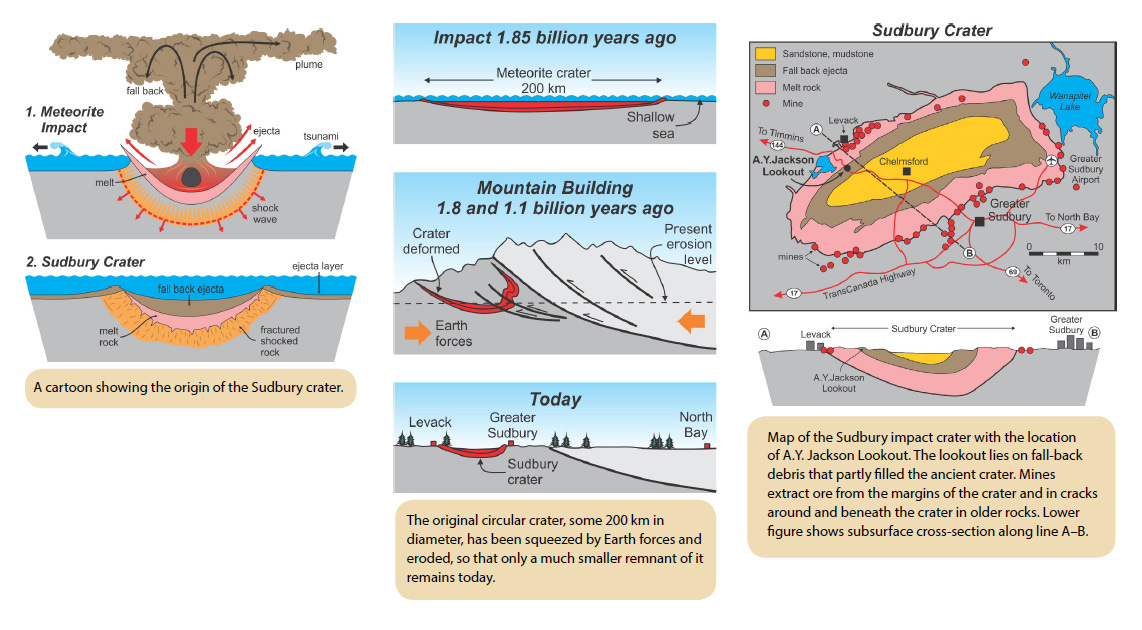

Magna Mining (NICU.V) is a junior exploration company in Sudbury, Canada, operating in a basin that has been mined for copper and nickel for the last 140 years. The Sudbury Basin is an impact crater from a 10 km wide asteroid that hit the earth around 2 billion years ago, which means that it is one of the few places that heavier metals such as platinum and palladium can be found as well. It is 60 km long, 20 km wide, and 10 km deep, in freedom units that would be 37 miles by 12 miles by 6 miles.

The negative aspect of mining an area with a 140 year history is that the easy stuff has already been had. But on the positive side, the area has an infrastructure of roads, processing plants, skilled labor, etc., which means that development costs should be much lower than in the proverbial “moose pasture.” In my original writeup on copper, I claimed that I didn’t like exploration stage companies, and I still don’t, but Brandon has now found two junior miners that fund exploration through cash flow of operating mines as opposed to dilutive equity raises, Idaho Strategic Resources (IDR), and now Magna Mining. This new business model is intriguing, if the return on exploration capital is high, which it very likely will be.

Time to Feed the Gold Bugs: Idaho Strategic Resources $IDR

The New Year’s fitness challenge slowed a bit yesterday, midcaps tend to get a lot more attention than small caps. This of course fuels my belief that small caps are more likely to be mispriced, I can’t even get my readers too excited about them. For yesterday’s article, I owe you 3 pushups and 16 sit ups. I am down to 283 pounds from 287 at the star…

Even though the Sudbury basin has been mined for 140 years, technology is constantly improving to lower costs and increase efficiencies, and if the commodity supercycle thesis is accurate, copper prices should rise due to the electrification of everything, the data center buildout, and the urbanization of Africa and South Asia. Not only has extraction and processing been improving, but exploration technology has been improving as well. How thoroughly were holes drilled and ore bodies probed in the 1880’s, the 1920’s, and the 1960’s? And with a geological formation six miles deep, core drilling beyond a couple thousand meters only began in the last few decades. While there are a lot of doomers going on about decreasing ore grades, many that work in mining believe the greatest deposits have yet to be found.

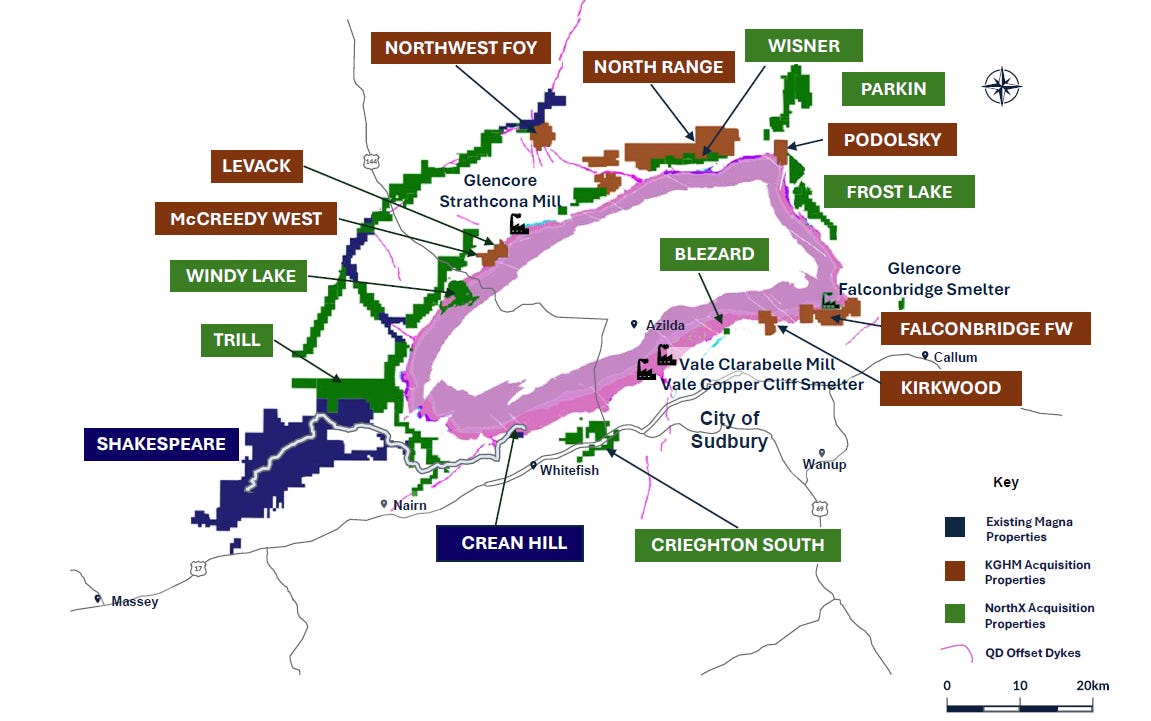

Just like Idaho Strategic, Magna Mining is a sub-scale miner following ore veins underground, as opposed to open pit mining. This method is not attractive to the majors, not because of the all-in-sustaining-cost of extraction, but because of the scale. And because of the lack of interest from the majors, the underground vein mining deposits are able to be acquired for a pittance. Magna Mining just acquired from KGH of Poland one producing mine, two care and maintenance mines, one past producing mine, and three exploration properties, as well as seven properties from NorthX, two past producing mines and five exploration properties. The total purchase price from KGH was 5.3 million CAD cash, 2 million CAD Magna stock, 2 million CAD deferred to December 31st of 2026, and contingent payments of 24 million CAD if some of those assets become productive. The total purchase price from NorthX was 1 CAD, or approximately $0.68 USD, and the property remediation liabilities. Pocket change for 15 properties. Also, Magna’s expansion isn’t finished, several majors have marginal assets in the Sudbury basin that could probably be purchased for a song over the next few years, and while I am not a fan of dilution for exploration costs, I don’t mind a bit of it for accretive acquisitions. Even these marginal properties, when synergies are obtained by acquiring adjacent parcels, and if enough are stitched together, can someday become an asset that a major would be interested in acquiring. And there are already adjoining properties such as Shakespeare / Trill, and Wisner / North Range.

Nickel was not originally on my radar, about 65% of annual nickel production is used to make stainless steel, so that would put it in the industrial cyclical materials sector, but in 2023, 15% of production was used to make batteries, so that would potentially give it a secular technological growth story. For someone who doesn’t have a clear prediction of which metal will outperform, it’s not a terrible strategy to just fill out the bingo card with a bit of everything, diversification is to handle the unknown, and I don’t know which metal will outperform. But one aspect of the Sudbury basin is that there are so many different branching ore veins with different compositions that Magna Mining has the flexibility to focus on whatever is fetching a higher price that quarter. If copper prices are relatively high, there is a deposit that is primarily copper. If platinum group metals are relatively high, there is an ore vein that is better for PGMs. But most of the economic value of the Sudbury basin is from the nickel in the ore.

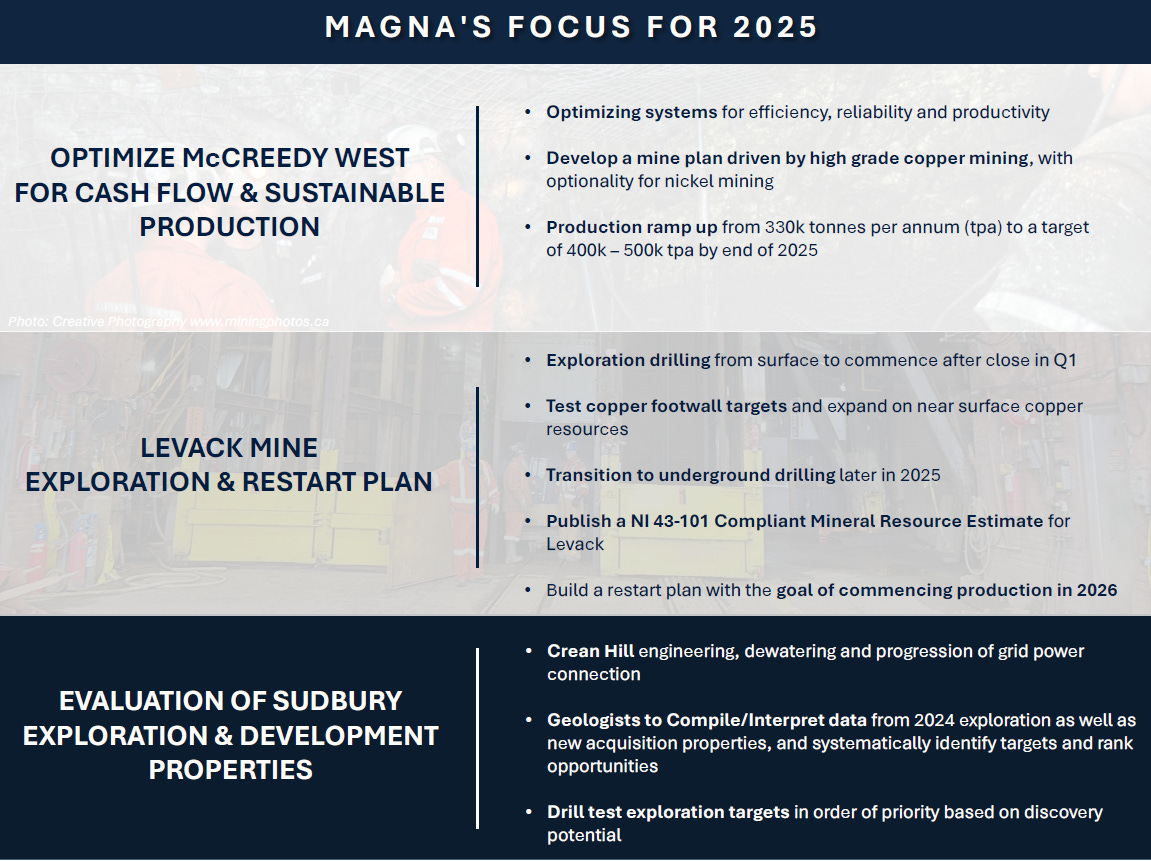

The operating mine, McCreedy West, produced 317,000 tons of ore in 2023, and Magna has a plan to double production in the next two years, which would lead to a 13 year usable life and a 40 million CAD annual cash flow at current metals prices. This is not particularly exciting with Magna trading at a 336 million CAD market capitalization, but, Magna is not really in the business of producing ore. In a recent interview, Magna’s CEO let the cat out of the bag if you can read between the lines, Magna is in the business of producing a mining company to sell to the majors at the top of the next cycle. The majors are notorious for overpaying for assets when metal prices are high, so why not build out an attractive asset for them to acquire.

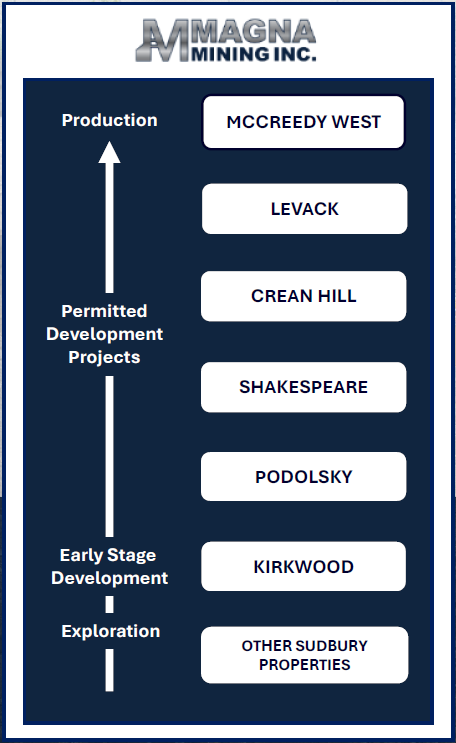

Magna has already announced a 30 million CAD drilling program to start proving ore quality at their exploratory properties. And at the expensive part of the cycle, mining companies can trade for between 10% and 20% of the value of the ore in the ground. McCreedy West, with over 9 million tons of ore indicated, has metal that is worth about about $2.4 billion at current prices, which would lead to about $240 million of market capitalization in a boom cycle. This is just about where Magna Mining trades today, which leads me to believe that the stock price should follow 10% of the in-ground value of producing mines only. There are fourteen other properties, four of them permitted, to explore and to prove deposits to increase the sale value of Magna. Maybe each individual property isn’t interesting to one of the majors, but when they are all stitched together, explored, developed, and producing, the company together would be polished up and ready for sale. As a shareholder, I would not anticipate cash flows from the mining to be returned to shareholders, those cash flows are going toward exploration and development to prepare Magna for that eventual sale.

Across three of the fifteen properties, Magna has 48 million tons of ore “indicated” as defined by Canadian regulation 43-101, with 1.29% average nickel concentration and 2.64% average copper concentration. That metal would have a market value of $11.7 billion at today’s prices, but of course there are costs associated with mining, processing, smelting, etc. If Magna traded at 10% of the in-ground value, that would be a market capitalization of $1.7 billion, about 7.5x of the current market capitalization. The $30 million exploration program will go on to prove even more reserves in the other properties. To start repricing toward that value, Magna needs to bring those properties into operation, and Magna has a plan in place to do just that.

Management has a production plan to restart production of Levack mine by sometime in 2026, the current indicated resources would indicate that should add around $160 million to the market capitalization of Magna, again assuming 10% of the in-ground ore value of a producing mine becomes the market capitalization. And best of all, this should be funded by generated cash flow, and not through further dilution.

Putting a two year price target on Magna, only based on the restart of the Levack mine, would be a market capitalization of 571 million CAD, up from the current 336 million CAD. That would imply a share price of 2.94 CAD up from the current 1.71, a 71% increase within two years, without considering any changes to copper or nickel prices. Looking farther out, as the cash flows increase, mines can be explored and developed faster and faster. Giving Magna five, seven, or ten years to keep on acquiring, exploring, and developing properties, could lead to extraordinary returns. Without mineral reports, these farther out price targets are very rough, but for the seven properties that have any data at all, we get an estimated market capitalization for Magna of $1.5 billion. Of course, at $10 nickel and $6 copper, that number becomes $2.25 billion. That is almost exactly a 10x return from the current share price. And there is upside if any of the drilling programs hit the mother lode.

Magna mining has the potential to be a 10x return or better over the next five to seven years, assuming $10 nickel, $6 copper, and all seven mines with mineral data are brought back into production. Not including the value of the other 8 properties, and whatever new mineral reserves can be proven with future drilling programs. I think this is what Brandon Beylo sees in Magna Mining, a management team doing a nickel mining rollup, stitching together marginal assets and bringing them into production until they are large enough to sell to a major at the top of the next cycle for a couple billion dollars.

It is hard to buy a stock that has already gone up by 4x in the last twelve months. And it is possible that the market provides a dip to buy here or there, especially with this current tariff kerfluffle. But a 10x, even if it takes 7 years is still an internal rate of return of 39%, far in excess of expectations for the S&P 500.

Magna Mining (NICU.V) 1.71 CAD: 2.94 CAD by end of year 2026

Magna Mining (NICU.V) 1.71 CAD: 17.09 CAD by end of year 2031