Time to Feed the Gold Bugs: Idaho Strategic Resources $IDR

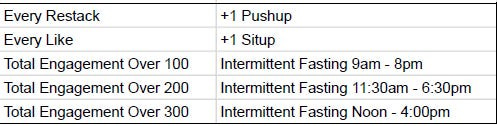

The New Year’s fitness challenge slowed a bit yesterday, midcaps tend to get a lot more attention than small caps. This of course fuels my belief that small caps are more likely to be mispriced, I can’t even get my readers too excited about them. For yesterday’s article, I owe you 3 pushups and 16 sit ups. I am down to 283 pounds from 287 at the start of January, although I suspect this has more to do with catching a cold than doing 6 to 10 pushups a day.

As a quick reminder, for the month of January, I will do 1 pushup for every restack and 1 sit up for every like that each writeup receives. If the combined number of likes and restacks reaches certain milestones, it will create a narrowing window of intermittent fasting.

I’ve seen Idaho Strategic Resources’ (IDR) name pop up on social media over the last year, several times from Brandon Beylo. I always had a reason to avoid it, the market capitalization was too small, the price had run up too much already, etc. Subconsciously, I probably didn’t write about it because it wasn’t my original idea. Things don’t look as attractive when I don’t find them on my own. But, after a recent selloff, my dumpster diving nature tells me that this is worth a closer look.

Idaho Strategic Resources was formerly the New Jersey Mining Company. (No, not that New Jersey.) New Jersey is the name of IDR’s gold processing mill in the Coeur D'Alene mineral belt of Idaho. The current CEO, John Swallow, was not the founder, but has been buying into the company since 2009, became the president in 2013, and assumed the CEO position in 2017. He now owns about 9% of the company, which makes this incentive alignment about as good as can be found. He has sold some shares recently, but it’s hard to fault a guy for taking some profits after 15 years. His son Travis also works at the company.

At first glance, IDR is just another junior gold miner. If you’ve been reading this substack for a while, you will know that I don’t like exploration stage mining companies. But Idaho Strategic is a production based explorer, that is, their exploration spend does not come from issuing stock and diluting shareholders, but from the cashflow of their existing producing gold mines. This new twist on the exploration business model is very interesting to me. I don’t have to play the game of trying to time it to the moment when the company is finished diluting, I can be wrong on the timing, and sit back and let the company execute its plan.

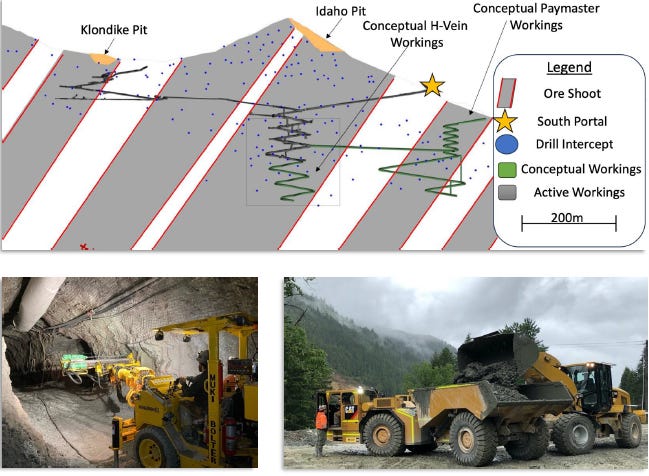

Idaho Strategic’s existing and producing gold mines are hard rock, narrow vein, underground tunnels. Management claims that this is the reason why these deposits were passed over by the larger mining companies who were only interested in large, open-pit style deposits. Management has identified six different ore shoots that should allow for consistent production over many years.

Beyond that, Idaho Strategic fancies itself more than just a gold miner, their exploration spend has extended into rare earths and thorium. IDR claims to be the largest rare earth landholder in the United States with their Mineral Hill, Diamond Creek, and Lemhi Pass assets. These deposits contain 19 out of the 50 strategic minerals outlined by the US Geological Survey. Thorium is particularly interesting to me because almost nobody is talking about it, but if we are really serious about nuclear energy, thorium is an excellent fuel source that doesn’t create plutonium as a byproduct. The plutonium byproduct is the reason why we focused on uranium in the first place during the cold war, by focusing on thorium it would mitigate the risk of the proliferation of humanity-ending nuclear weapons. The narrative isn’t there yet, but any rational policy would prioritize thorium fission reactors for the world. If you are interested in buying a producing and growing gold miner, but also getting a handful of lottery tickets along with it, these are some hot lottery tickets.

But the rare earths and thorium are too far into the future to underwrite the investment in Idaho Strategic for my preferences. Regarding the gold mine itself, production has been around 10,000 to 15,000 ounces per year, with an all-in-sustaining cost of around $1,300 an ounce. Some quick arithmetic reveals a business that would have around $13 million to $19 million of gross profit at current gold prices. Trailing twelve month results are not too far off from that. With a market capitalization of $139 million, you would be paying around 10x forward EBITDA.

Gold production at Idaho Strategic should come close to doubling in the next two years. Management is building a new facility at their Golden Chest Mine to process backfill, but they are building a facility large enough to house a future processing mill. Once the backfill plant is completed, Idaho Strategic plans to add a second shift. I wouldn’t go so far as to presume that a double shift would double output, that rarely happens. New hires need to learn the job, and something about working overnight tends to bring out low productivity, whether through selection bias, or causality, I don’t know. So that 10x 2025 EBITDA has a decent chance of being 5x to 6x 2026 EBITDA, which is not terribly expensive. It isn’t outright cheap, but IDR’s landholdings probably prevent it from ever being outright cheap again.

In 2013, IDR had about 240 acres. Today they have 8,600 acres for gold exploration, with 1,500 acres privately owned, and 18,000 acres for rare earths. The land that isn’t owned outright are claims on federal lands. One of the great tragedies of the United States is that by the time settlers reached Colorado, the mentality had shifted from being for the people, to being for the government. The old John Locke theory of homesteading land was eschewed in favor of Federal Leaseholds. This mentality shift has stymied the growth and development of the Western half of the United States. And this lingering national ownership of the land is a downside to operating in Idaho. If I had Trump’s ear, I would try to persuade him to transition ownership of the majority of this federal land to the farmers and miners that are currently leasing it. Maybe even give them a zero percent mortgage and use the proceeds to pay down some national debt. An interesting quirk of being an underground miner is that the 1,500 owned acres gives the rights to mine underground on adjacent federal lands, and IDR focuses on underground, narrow vein mining.

The landholdings of Idaho Strategic, and the size of the mineral deposits which CEO John Swallow accumulated for the last eleven years, are so vast, that he admits that IDR is too small to develop it alone. News of a rare earth joint venture, with a larger partner footing the capex, is a distinct possibility in the near to medium term. And while thorium isn’t front of mind in the US, it does already have traction in Europe and Asia. So some of these lottery tickets might not be as far into the future as I made them out to appear.

In May of 2024, Idaho Strategic Resources signed an Memorandum of Understanding with Radiant Technologies, the Andreessen Horowitz small modular reactor startup. The MOU was for the deployment of a nuclear reactor to power IDR’s mining facilities. That Radiant SMR will be fueled by uranium, so not an indication of the viability of the thorium deposits, but the relationship came about through enormous activity between IDR’s leadership and the government regulators. This should indicate that things could move somewhat quickly in the US regarding rare earth elements and nuclear power generally. There is even the possibility of the government paying for half of drilling costs starting early in 2025, this has led management to slow down their organic drilling operations while waiting for the half-off sale.

I don’t expect any return of capital to shareholders from Idaho Strategic, instead, I expect cashflow to be split between expanding gold production, exploring for new gold deposits on their 8,600 acres, occasionally drilling samples of their 18,000 acres of rare earth deposits, and hopefully buying some more acreage here and there.

So, in summary, you have a junior gold miner which is using production to self-fund growth, exploration, and land purchases. It was an overnight success that took about fifteen years, but now is at a stage where growth could take place very quickly. It has some of the strongest incentive alignment possible, with a CEO who acquired their shares on the open market, and his family works for the company. And is the largest rare earth element landowner in the United States just at the time that China is placing retaliatory restrictions on rare earth exports. The recent price collapse from $17 a share to $10 a share is a gift that I won’t take for granted.

Putting a price target on Idaho Strategic is a bit of a fool’s errand, as it clearly doesn’t trade in line with peers with regards to sales, book value, or earnings ratios. I would be punting to say that as current gold production doubles into 2026, the stock price should double as well. This ignores the vast acreage of rare earth elements, as well as the exploration projects at the Eastern Star or the Murray Gold Belt. It also doesn’t take into account the future price of gold, which if you are even interested in this company means that you predict it should be somewhat higher in the future. Just for the sake of having a price target, I’ll say double by the end of 2026, but we all know that’s a punt.

Idaho Strategic Resources (IDR) $10.22: $20 by end of year 2026

1 push-up per restack sounds cheap… how about 10? And say 3 sit-ups per like? 😆

💪💪💪

hard to discount back the value of those rare earth metals to present...

so...any other FOAs laying around?