Why I chose Equinox Gold $EQX for my gold exposure.

If I knew the market was this inefficient, I might have waited.

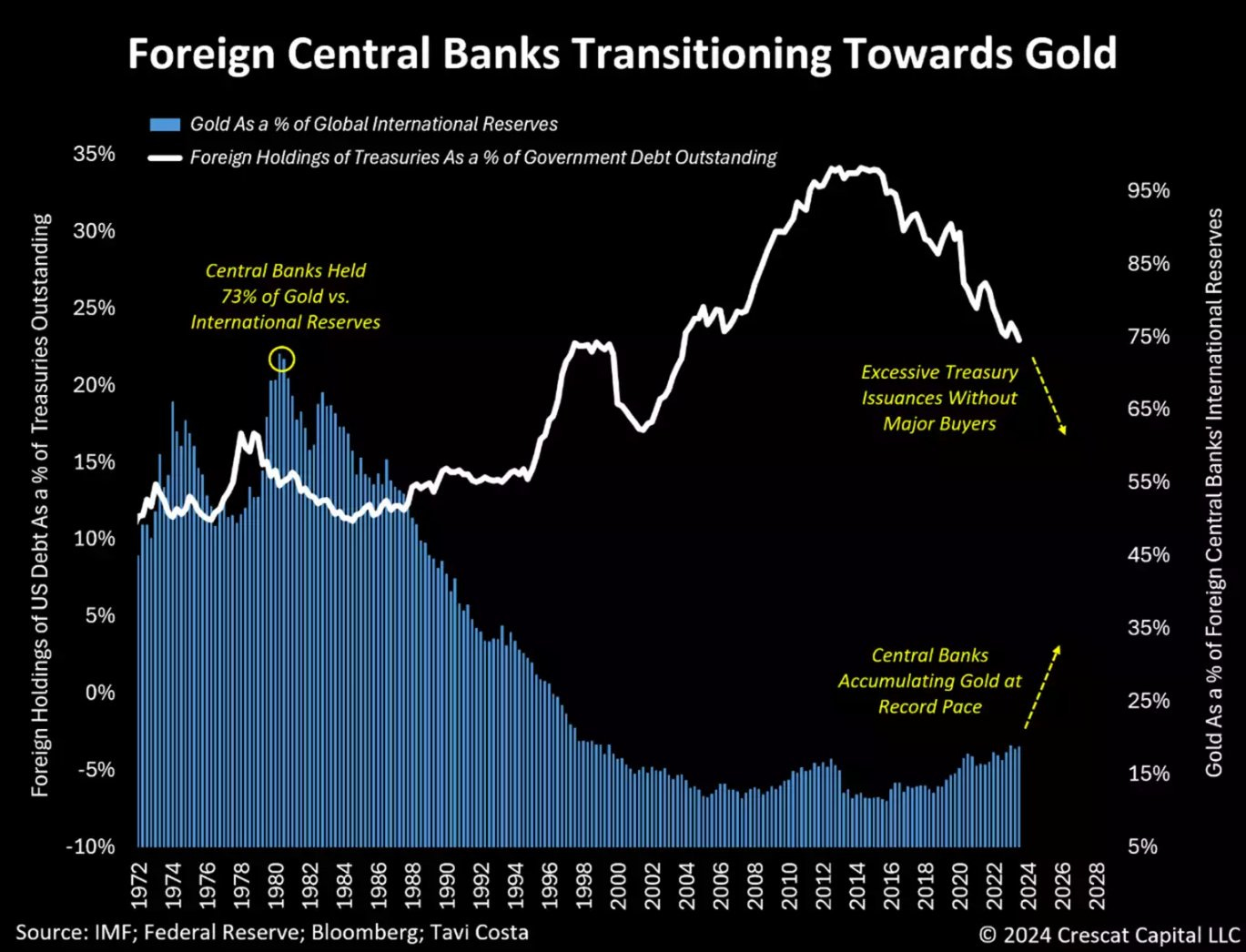

I am devoting a part of my portfolio to gold because gold, oil, and land outperformed the last time we had sustained inflation and sustained inflation is very likely while congress is running a deficit of 7% of GDP. Also, when the US confiscated Russian financial reserves, the entire global south started looking for an alternative for international settlements, and they aren’t so eager to use the Yuan. On top of that, India is growing GDP at 7% a year, and gold is still culturally a preferred way to save for the 1.5 billion people of India who reportedly already own 10% of all the gold ever mined by humanity, and they accumulated that at a GDP per capita of $2,400. Oh, and China recently encouraged their citizens to start saving in gold as well, which is 1.2 billion people with a $12,700 GDP per capita and a much higher savings rate. Once western asset managers start looking for assets which are negatively correlated to stocks now that bonds have flipped to positive correlation, the gold price could surprise us all.

Graphics courtesy of Tavi Costa:

As a generalist investor, I am always walking into industries where I am out of my depth. I try to find the essence of what it takes to make a good decision, and this is not always easy. In mining, there are four tiers of risk / reward tradeoff, and in descending order of riskiness they are exploration, buildout, operation and royalty.

Royalty companies are for the venerable income investor who has already made his fortune, and is only concerned with not losing ground to inflation. To finance the buildout of mines, royalty rights are sold on the future minerals extracted. In exchange for early money, the royalty company receives a percentage of the mine’s production. The royalty company doesn’t take the risk of managing the mine’s costs of production, they just get a stream of gold ounces for the life of the mine. They do get exposure to rising gold prices, but for me, this type of company is too low octane.

Large operators have well established mines, their only job is to operate them well, which is not an easy task. After listening to countless mining earnings calls, I cannot emphasize enough just how many problems can pop up in the mining sector. Floods, fires, shaft collapses, labor disputes, copper wire theft, supply chain disruption, equipment failure, electric grid reliability, regulatory changes, environmental lawsuits, indigenous tribal relationships, etc.; these guys have their work cut out for them. Mining is all about waking up in the morning and solving problems, and after lunch trying to solve the new batch of problems that popped up in the morning while you were solving the last ones. Nature does not yield her minerals to the faint of heart.

On top of that, the large operators suffer from chronic poor capital allocation, they incinerate cash by expanding at the top of the cycle every time, and they incinerate cash by exploring to try and convert their annuity-like business into a perpetuity-like business. I think the operators would be better off not trying to prove as many new reserves, and instead, just accepting the reality that their business is not perpetual, and buy out the successful explorers and buildouts, but not at the top of the cycle. Is this too much to ask? History says yes.

Investing in explorers is like buying lottery tickets. Not even the geologists really know what they are going to find until they spend a few million dollars drilling rock cores and analyzing the mineral content. The key to this space is owning enough different explorers so that some of your lottery tickets will pay out. Even though I call myself a degen, that applies to the leverage I use, and to use leverage it needs to be on a more stable foundation than this. Buying stock in ten companies, knowing that eight will go to zero, is not my style.

For me, the sweet spot is the buildout, it is a mix of pure time arbitrage and a judgement about management’s chance of success. The mineral content of the rock has been proven in the past by the exploration company, now a team comes along to buildout the mine, which takes years, is not always successful, and frequently is over budget leading to future dilution as they need to raise new capital. It is possible to look at the track records of the management team and have a decent prediction about their likelihood of success or dilution. And this is where Equinox Gold (EQX) really shines.

Ross Beaty, the chairman of EQX successfully founded Equinox Resources in the 1980s, where he built out three mines and sold the company to Hecla Mining (HL). Then in the 1990s he founded Pan American Silver (PAAS), which acquired several mines and built out some others. It’s hard to keep track, but it looks like Ross Beaty has successfully built out six mines in his career, relatively on time and on budget. This is an amazing track record, and is as good of an indication of future success from management as can be found.

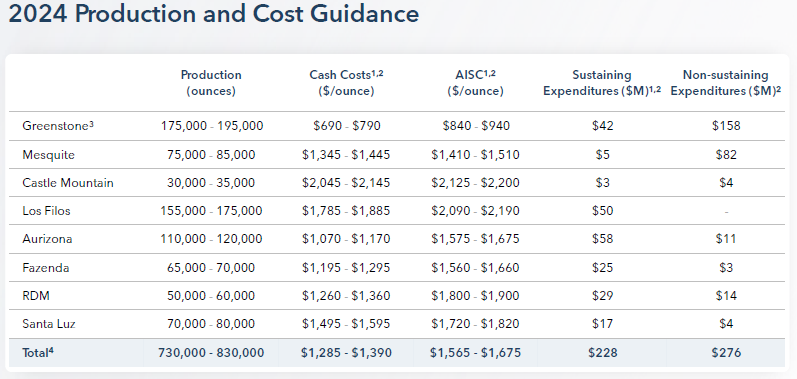

EQX is building out their flagship mine Greenstone in Ontario Canada. It is projected to have a cost per ounce mined of $975 and an annual production of 400,000 ounces per year. At the current gold prices of $2,300 an ounce, that is estimated to generate $530 million of EBITDA per year. The current market cap of EQX is $2 billion.

So how much time arbitrage is left on the Greenstone mine that EQX is building out in Canada? None, they already finished, the first gold was poured on May 22, 2024. Not only has the gold price gone from $2,000 an ounce to $2,300 an ounce this year, but EQX already finished the buildout of their mine and the market hasn’t responded. Is the market so quantitatively driven that it needs four quarters of data to plug into their models before the price responds? Apparently so.

I believe the market was spooked by two things, first, as a way to finance the mine, EQX committed to some long term sales contracts in the $2,000 an ounce range before the price runup. This last quarter disappointed people who did not do their due diligence and were expecting sales to fetch $2,300 an ounce. Second, EQX bought out the remaining 40% of the Greenstone mine from their original financier, Orion for $1 billion in stock and cash. That price was not a discount, it wasn’t overpaying, it was fair. But, I think the market has a knee jerk reaction toward any dilution, even if it does turn out eventually to be accretive. Buying out Orion at a fair price is a bet on gold prices rising further, with which I fundamentally agree. And Ross Beaty, with his 8% ownership stake in EQX has an incentive alignment to only dilute accretively.

So even if gold prices are stuck in a channel for the time being, the next few quarters should show positive improvement for EQX, as the 60%+ of active investors who are quantitatively driven should start bidding up the price when they see the next few quarters of results. The cashflow should dramatically improve as the new ounces coming online from Greenstone were not precommitted at the $2,000 an ounce long term contract.

Now what will EQX do with that cashflow, will they return it to shareholders? Probably not, Ross Beaty has a bigger vision for EQX than just Greenstone. That cashflow is going to get put toward deleveraging and will then get plowed into their other expansion projects, Aurizona in Brazil, Castle Mountain in California, and Los Filos in Mexico. Which is fine by me, as long as they keep delivering reasonably on time and on budget, I like the buildout phase of miners, and I predict higher gold prices. EQX will probably not return capital to shareholders until after Ross Beaty puts the cherry on top of his vision as he did twice before with Equinox Resources and Pan American Silver.

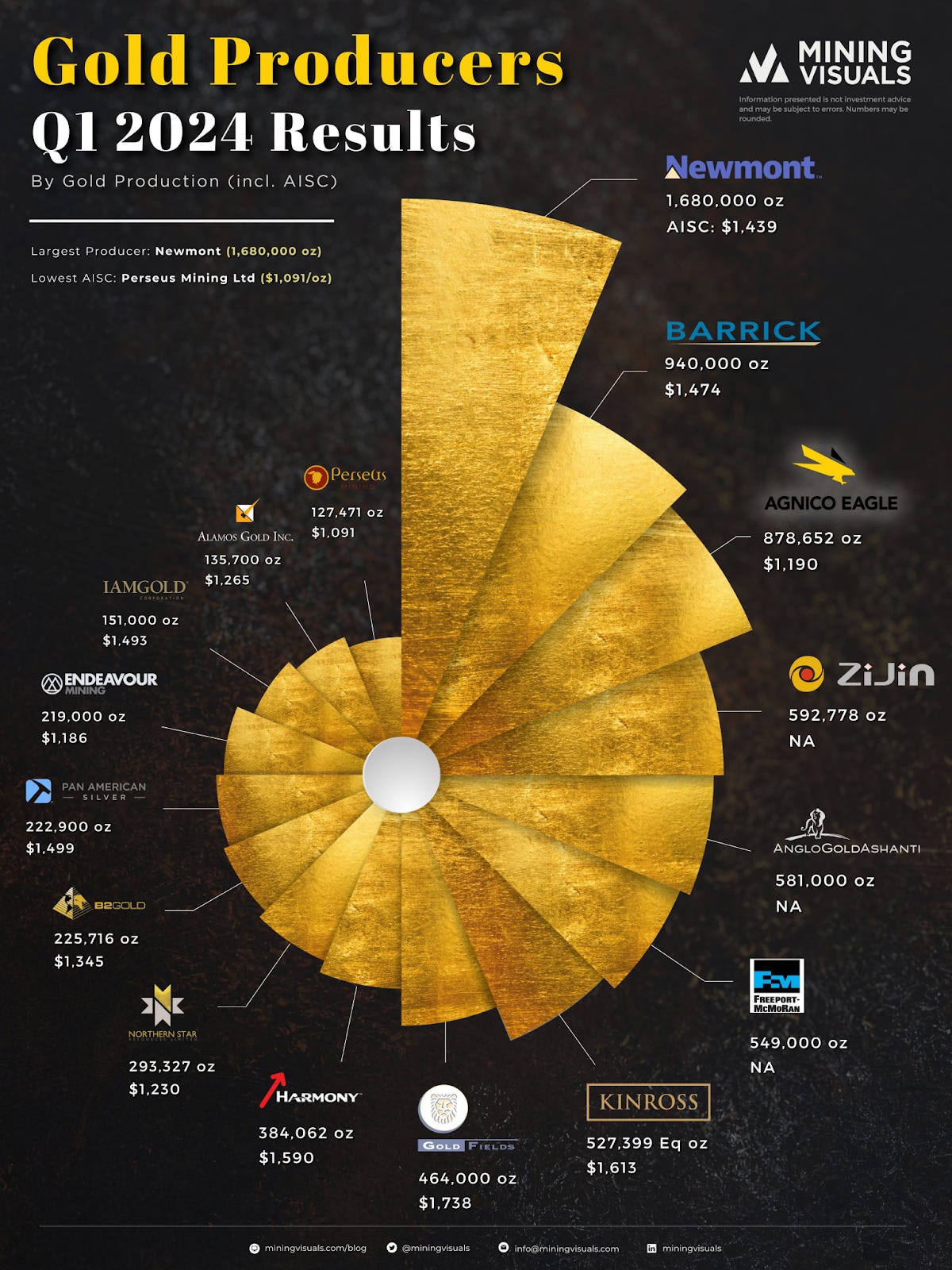

So how to put a price target on EQX, they are on their way to becoming the 10th or 11th largest gold producer? Newmont (NEM) has an enterprise value of $53 billion off of about a 6 million ounce annual production. Barrick (GOLD) has an enterprise value of $29 billion off of about a 4 million ounce annual production. Agnico Eagle (AEM) has an enterprise value of $33 billion of about a little less than a 4 million ounce annual production. Giving EQX a discount compared to larger peers, but a premium once they surpass the psychological 1 million ounce annual production amount would result in about a 3x over the next two years, assuming marginal cashflow goes toward debt paydown given reasonable operational performance, without any increase in the gold price, and not including the three current expansion projects.

If I haven’t lost your attention already, (my wife tells me these write ups are too long), as Rick Rule will tell you, in the last gold bull market, gold miners saw profits fall rather than rise. I believe this was due to a difference between cost push inflation in the gold price vs demand pull inflation in the gold price. In this environment, it is the buying of central banks pulling on the gold price, and the gold price is outpacing the cost of chemicals, labor, diesel, and machinery to do the mining. In this instance I would rather own the miners than the metals, but this was not true in decades prior.