Will Trump Bull-Moose a 5.5% 30-year Mortgage?: Rocket Companies $RKT

The Best Thing to Come Out of Detroit Since The Temptations

I have been predicting higher sustained inflation and higher interest rates as my base case for a while. Now that the Federal Reserve is chasing inflation, they won’t be able to cut rates in the way that they have done since Alan Greenspan pioneered it. Even if the overnight interest rates were to be cut to the current target of 3%, a normal yield curve would imply a 10-year treasury of 4% to 4.5%, about where we are now. But at the same time, it appears that the market believes that the 10-year treasury is on a downward trajectory.

Up until today, I had strong suspicions that Trump would want a lower 10-year treasury rate (he is a real-estate guy after all), but he might not be able to get it. Even if he were to browbeat Jerome Powell, the overnight rate and the bond market are two completely different things. I didn’t anticipate that Trump would try to browbeat the bond market directly. I now believe that Trump has good odds of being successful at achieving a 3% to 3.5% 10-year treasury during the first two years of his administration. And he will accomplish this by bullying other countries into buying our treasuries, while at the same time, the new Treasury Secretary will follow in Janet Yellen’s footsteps in only issuing as much long term debt as the market can handle and funneling the rest into the overnight rate, which the Fed is happy to control.

As you can see from the tweet above, Trump is going to attempt to bully the BRICS into buying treasuries. I think it’s safe to assume, whether covertly or overtly, Trump will use the same tactic on our allies. Australia, Canada, the UK, Germany, Japan, South Korea, etc., all will have some sort of pressure applied to buy more long term US debt. And I think it will work, but only for Trump. Whoever wins in 2028, whether JD Vance, Gavin Newsome, or some other political creature, they won’t have Trump’s ability and willingness to make credible threats to get their way. It really isn’t since Teddy Roosevelt spoke softly, but carried a big stick, that the executive branch could so successfully bully his desired outcomes. And it can also be done without the cooperation of congress or even Jerome Powell.

If we have a 3% to 3.5% 10-year treasury, and the spread between treasuries and 30-year mortgages compresses from 2.5% to 2%, then we could see a 5% to 5.5% 30-year mortgage within Trump’s first two years in office. The spread between the 10-year treasury and the 30-year mortgage can be as low as 1.5% at times, but about 0.5% is due to the regulatory burden created after the 2008 crisis, and another 0.5%, give or take, is from the Federal Reserve rolling off Mortgage Backed Securities as they mature. I believe it is more likely that Trump will roll back banking regulations than that he will convince Jerome Powell to engage in quantitative easing with an emphasis on MBS.

At a 5% to 5.5% 30-year mortgage, the existing housing market would finally thaw out, and all the realtors which I wrote about in comparison to the my paywalled pick, Compass (COMP), Anywhere (HOUS), and Re/Max (RMAX) would all do very well.

Paywalled small cap of the week, old-fashioned Ben Graham net-net, potentially a two to five year 10x.

I would like to thank Benjamin Demase for hosting me on his YouTube channel, The ROI Channel. And special thanks to my two founding subscribers, you guys are total chads for paying more than the minimum.Value Degen’s Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

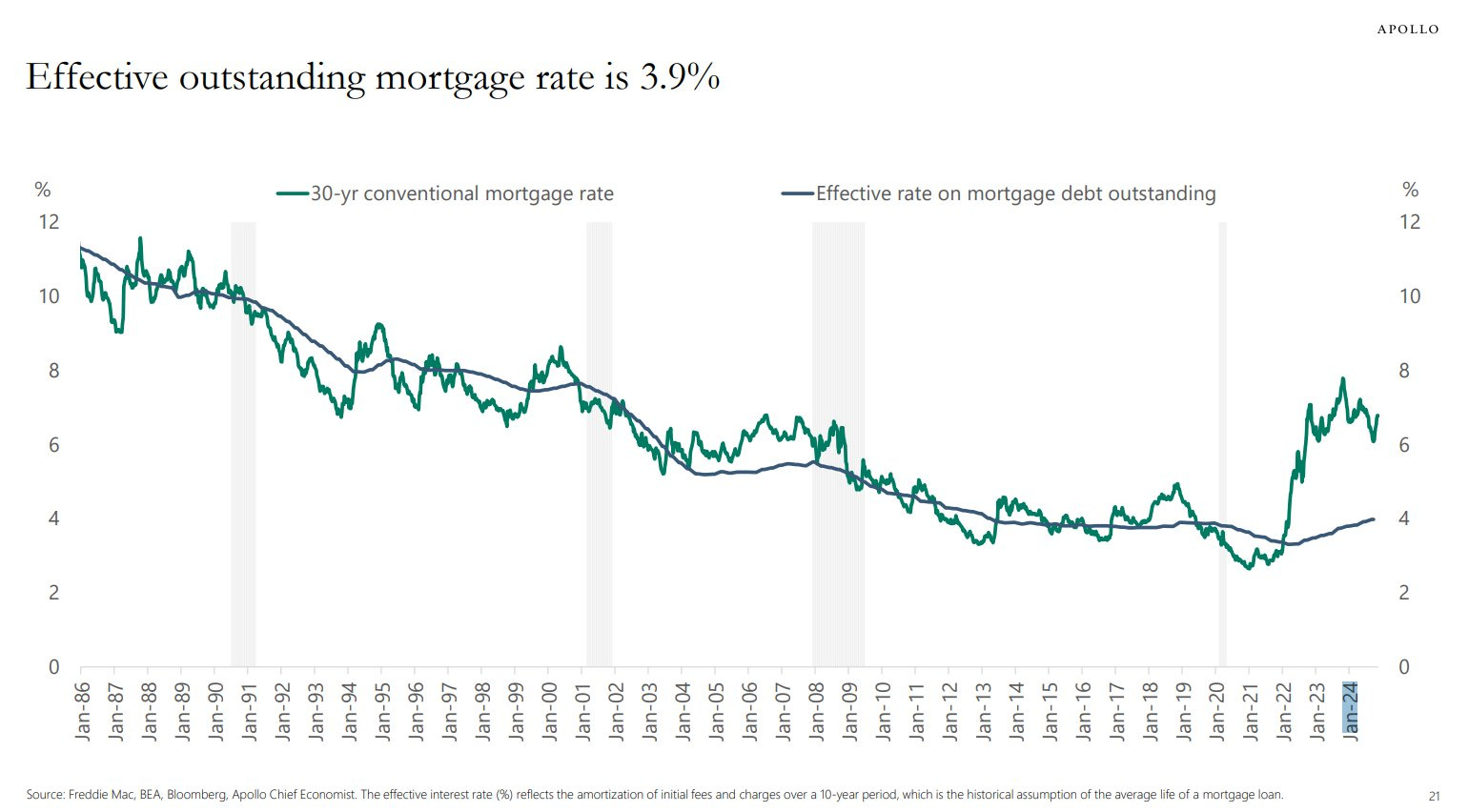

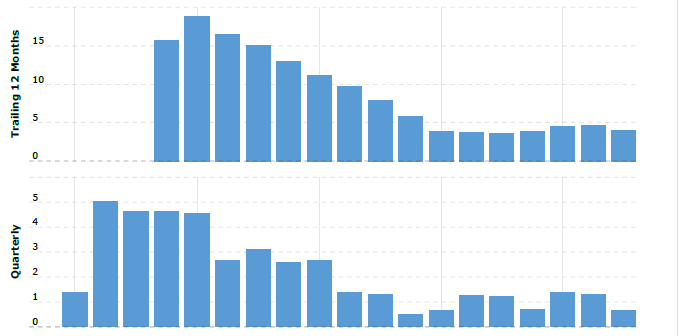

But anyone who got a 7% mortgage in the last two years would immediately refinance it. I am less convinced that we would see a huge wave of cash out refinancing like we saw in 2021 when the average interest rate was 3.62%, and 750,000 households cashed out a median of $37,131 in a single quarter. You can see below, there has been so little volume in housing transactions that the effective outstanding mortgage rate is still 3.9%.

Homeowners have a lot of equity, but anyone with a mortgage pre 2022 would probably do a home equity loan over a refinance. The Fed Funds Rate started 2006 at 4.25% and increasing, but we saw home equity loan volumes of more than 4x the current volume. I think we could break the 2004-2006 record for home equity loans this time around.

US homeowners have about $32 trillion in home equity, so I think we should expect that if Trump is successful in bullying a 5.5% 30-year mortgage, the home equity loan boom will be something to behold. There are a few companies worth discussing, the liquid midcap Rocket Companies (RKT), the degenerate small cap Lending Tree (TREE), and the quality growth Mr. Cooper (COOP). Today I will focus on RKT, and I will leave the other two for another day.

Rocket Companies is formerly known as Quicken Loans, based in Detroit, a mortgage oriented FinTech company that caters mostly to mass market customers. I had owned RKT in the past, the valuation was cheap, and there was heavy insider buying from the CEO Jay Farner, a hand-picked, internally groomed, successor to the founder and still majority owner Dan Gilbert. But Jay Farner retired, and RKT quickly went through two new CEO’s, neither of which had the confidence or the gumption to buy RKT stock at current prices. I was not yet unemployed at that time, and I didn’t have time to re-underwrite the thesis. There is still consistent insider buying from Director Matt Rizik but I don’t place a lot of emphasis on directors’ judgement. Matt Rizik has an accounting background, and is the CEO of Dan Gilbert’s family office, so his judgement might carry a bit of signal through the noise. The new CEO of RKT is Varun Krishna, formerly of Intuit, Paypal, Groupon, Microsoft, etc.

As with many financial companies, their financial statements have a lot of moving parts, a lot of mark-to-market adjustments, and a lot of “adjusted” figures which require a leap of faith on behalf of the investor. Recently the SEC has been clamping down on the overuse of adjusted metrics, and all investor presentations need to have the equivalent GAAP metric as well. This last quarterly earnings, it appears that investors focused on the GAAP figures over the adjusted figures, because the share price sold off heavily.

Times have been tough for Rocket Companies, they focus on mortgage lending, and as one would expect, revenues are down considerably from the 2022 peak. Trailing twelve month revenue peaked at $18 billion, and now stands at $4 billion, quite a shellacking. But because RKT has a mortgage servicing business, and incredible control over fixed vs variable costs, despite revenue falling by 77%, EBITDA has remained mostly positive, and if you trust management’s “adjusted” EBITDA, things are just swell at RKT.

The SEC mandated GAAP endnotes for the presentation showcase that the $286 million adjusted EBITDA for the quarter could also be described as a $481 million net loss. Gotta watch those mark-to-market adjustments.

In an attempt to get past all the adjustments, I’ll look at gross profit which has fallen from $4 billion a quarter to $600 million a quarter, versus shareholder equity, which has fallen from $9.7 billion to $8.8 billion. Cash on hand has fallen from $2.4 billion to $1.2 billion. Trying to pierce the fog, this interest rate environment did cause some pain, but the business is hardly distressed, and they have plenty of runway to last several years. And best of all, they are taking market share in both mortgage origination and refinancing origination.

Gross profit:

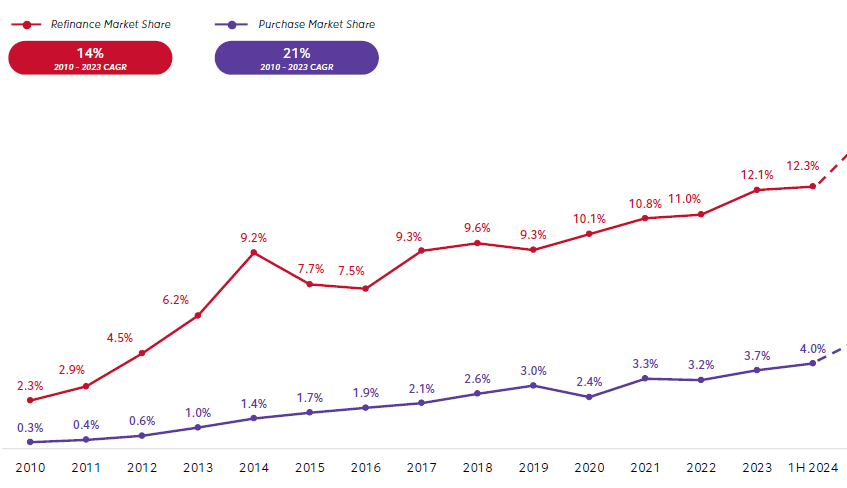

With 12% of the refinance market share, I don’t think any business will capture more of the boom if Trump does achieve a 5.5% 30-year mortgage than Rocket Companies. But there might be some small caps with more torque than RKT.

Don’t expect any of that adjusted EBITDA to be returned to shareholders, every nickel gets plowed into FinTech development. I am not a tech expert, so it’s hard for me to know if they are getting a good return on all that software development. But I do know that before Ozempic and Artificial Intelligence, trying to figure out which FinTech company would build the biggest network was such a serious theme that Goldman Sachs tried and failed miserably to break into it. Is the $500 million that RKT spent on software better than paying a dividend? Time will tell.

One of the larger points of confusion and risk about RKT is the strange corporate structure which they used in order to go public. The public float is only about 5% to 8% of shares outstanding, with most shares still held by founder Dan Gilbert. Going public adds exit liquidity, allows the market to set the price on the margin for valuing shares given to charity, allows better access to capital markets to raise debt or complete acquisitions, etc. There are a lot of benefits to being public, but as a shareholder, it’s not always optimal to be in a completely controlled company. But on the other hand, at least Larry Fink’s opinion doesn’t carry any weight here either. Due to the incredibly small float compared to size of the business, the stock price on the marginal share could whipsaw around with huge volatility. If you are nimble when you enter and exit, there is a lot of opportunity; so much opportunity that RKT is a well known meme stock on Reddit.

The prize at the end of the rainbow for all of these mortgage based FinTech companies is to get the people on their platform to originate their mortgage on the app, and spare the company from paying a fat commission to a mortgage broker. The mortgages originating on the app have zero acquisition cost in a world where broker commissions are typically half of the pizza. RKT does a pretty decent job of breaking down the value chain:

That $1,600 of Title and Closing fees (on a $300,000 mortgage) is also a target for the new Douglas Elliman (DOUG) CEO.

I am not a typical tech investor, but I do appreciate that RKT can grow their tech platform with retained earnings instead of the Silicon Valley method of rounds of equity fundraising. I also am impressed by how RKT can make enough on their mortgage servicing portfolio, about 2.7 million mortgages, to pay most of their fixed costs in this down market. Tomorrow I will be writing about Mr. Cooper (COOP), who has a 6+ million mortgage servicing portfolio, and is a solid quality growth name.

Rocket Companies is probably the company best situated to benefit in an environment where 30-year mortgage rates fall to the 5% to 5.5% range, low enough for home equity loans, probably low enough to thaw out the housing market, but probably not low enough for cash-out refinancing as the pre-existing mortgages average 3.9%. This also makes mortgage service revenue more sticky, as the chance of early mortgage repayment is at an all time low. Another benefit for RKT, but also for COOP. With the recent price action, I think this is a reasonable entry point for RKT, but due to the size of the business, the upside potential in the near term is limited. If RKT can become 20% of mortgage refinancing market by 2027 as they desire, then it would be an incredible quality growth stock, but until I see if market share grows as the market heats up and not just as it cools off, for me it is a potential rebound for a quick pop to $20 as interest rates fall. I’m ready to date Rocket, but I’m not convinced I want to marry her.

$GHLD Guild Holdings Comp. would be interessting to look, cause it does reverse Mortages like FOA. Maybe they profited from the inverted yield curve as well.

$LDI is another one to look at.