Will I get Kohl in my Stocking for Christmas? Kohl’s Corp $KSS

Muddling Midcaps

Welcome back to another Muddling Midcap. These fallen angels end up at a small market capitalization, despite being sizeable businesses that deserve respect. Kohl’s (KSS) is at just about a $16.5 billion revenue run rate ($20.5 billion at the peak), but sits at a $1.64 billion market capitalization. At a price to sales ratio of 0.1x, it gets my attention.

I do believe that consumer discretionary, one of the worst performing sectors of 2024, could be due for a meaningful outperformance in 2025. However, Kohl’s targets the middle class, and the theme of the last four years has been the K-shaped economy. Wealthy individuals have had an almost 5% money market rate to generate an enormous income on their cash for the first time in decades, and this money has been circulating in their favorite shops. But the middle class has been trading down to bargain shops, leaving brands like Kohl’s under extreme distress.

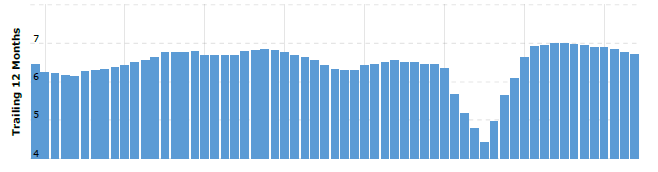

You can see the story in their trailing twelve month revenue, first with the Covid lockdowns, but then with the Biden economy, which the media told us was wonderful, but the middle-class facing brands have told us was not.

I believe the narrative surrounding Kohl’s is incorrect. People seem to think that online shopping is going to devour all retail. I think that if there is a middle-class recovery, when people have money in their pockets, they like to shop. They like to try things on, hold them in their hand, feel the texture and the weight, and fill their bags.

I also believe that the overall economic conditions are only half of Kohl’s problems, the other half are of their own making. Just compare Kohl’s revenue over this time period with Dillard’s:

So where did Kohl’s go wrong? Lots of places. In 2023 CEO Michelle Gass left Kohl’s to become the CEO of Levi Strauss. Kohl’s filled the gap with interim CEO Tom Kingsbury while they performed the search for Gass’ replacement, which has just been named, Ashley Buchanan, current CEO of Michael’s. Year over year, Kohl’s was underperforming Dillard’s even before Michelle Gass’ departure, however, Dillard’s really knocked it out of the park with Facebook event advertising after the Covid lockdowns were lifted. It was like a block party in there.

Levi Strauss has been doing just fine, so I would take a guess that the changes Michelle Gass implemented for Kohl’s were probably pretty decent. Interim CEO Tom Kingsbury, bless his heart, seems to have been in completely over his head, and drove Kohl’s into the ground. Michelle Gass had focused on omnichannel growth, and the development of private label brands so that Kohl’s would not have the same branded merchandise as their competitors. Tom Kingsbury re-embraced the branded merchandise, and on the last earnings call, admitted that this was a mistake, and that Kohl’s had just made a large purchase of their proprietary brands to fill the shelves before the Christmas season.

Michelle Gass also created a partnership with Sephora, putting Sephora stores within the Kohl’s department store. This is bringing in millions of new and younger customers to Kohl’s, but in order to make space, the jewelry counter and the petite clothing line were scrapped. Traditional Kohl’s customers really liked their jewelry counter. My grandmother was a petite woman, and I can tell you by experience, they are fiercely loyal to whichever department store has their sizes on the shelf. Just in time for this Christmas season, the jewelry counter is being redeployed in over 200 Kohl’s locations, and the petite clothing is being redeployed as well. This might even be a stealth Ozempic beneficiary. Petite women talk to each other about which stores cater to their needs.

On top of that, Kohl’s has started a partnership with Babies R Us. I think this is smart for a couple of reasons, first, with the Bed Bath and Beyond bankruptcy, their Buy Buy Baby store was profitable, and could have been sold or spun off, but was allowed to go down with the ship. There is room in the marketplace for a baby themed store, and this gets younger people into Kohl’s to join their rewards program. Also, being the go to place for gift registries is a nice business, which is starting to get traction at Kohl’s. Baby stuff is one of those areas where shoppers like to feel and hold the items, and should be resistant to online competition. You should see the expression on my wife’s face every time she touches a baby blanket when we are buying a baby-shower gift.

Tom Kingsbury, interim CEO, is an interesting character, not only did he make a $2 million insider purchase, but he also made a lot of mistakes. However, as the data came in, he acknowledged those mistakes and has started implementing changes to fix them. So Tom has my respect for being a decent guy who was in way over his head while Kohl’s searched for Michelle Gass’ replacement. I think Tom Kingsbury was a loyal soldier, given a job too big for him, and he did his best.

Regarding this new replacement, I have no idea how Ashley Buchanan was as the CEO of Michael’s for these last four years. Michael’s is owned by Apollo, and that data isn’t readily available. Here’s hoping he performs at a high level. But without knowing which changes the new CEO is going to make at Kohl’s, buying the stock today would just be a prediction on a middle class recovery generally and not the Kohl’s turnaround specifically. Management tried to assure investors on the last earnings call that in the hiring process, they ascertained that Ashely Buchanan was on board with the overall strategy, which hopefully after correcting for Tom’s mistakes, is the right strategy. But of course, the new CEO will need to put his fingerprints on things too.

I will be listening to the CEO on his first earnings call, because the opportunity in Kohl’s is enormous. As recently as 2021, the market capitalization was $9 billion. In 2015, it was $15 billion. If Kohl’s can successfully turn themselves around, it could be a near term four bagger, or a longer term ten bagger. Again, I do not believe Kohl’s is fundamentally suffering from an existential threat from Amazon competition, I think they are suffering from cyclicality and their own mismanagement.

Just given the macro environment, I think odds are very good that we went through a shallow recession recently that the government data agencies were too daft, or too partisan to declare it. A decline in full time employment has, over the last fifty years, always occurred mid-recession. Until now, of course. This is just one of many data points I have seen over the last 18 months of mixed signals, but looking forward, is incredibly bullish for consumer discretionary stocks. Even without a CEO doing the right things, Kohl’s has very good odds of having a real hum-dinger of a 2025.

As a highly seasonal business, Kohl’s is very dependent on the Christmas period. Due to higher volume and inventory destocking, they could generate upwards of $700 million in cash flow next quarter. Half of this is probably dedicated toward retiring $353 million of notes due July 2025, but after that, Kohl’s has no imminent maturities on their $1.2 billion of long term debt. They have a long runway to figure things out, as long as they can stay net income positive in the meanwhile, which they have done, even during this “not a recession” recession.

Kohl’s is so far maintaining a dividend of $0.50 per quarter, or $2.00 per year. This is important, because 2024 earnings are estimated to be around $1.50. I think bolder leadership would have cut the dividend in order to save $200 million annually to retire more debt, and a dividend cut is a distinct possibility going forward. But the dividend is probably the only thing anchoring Kohl’s stock price, so a dividend cut would probably see the stock price fall, potentially even getting cut in half again. Is it the smart thing to sit back and wait for the stock price to fall? Maybe.

There are very good chances that Q4 might outperform, on a relative basis, that is revenues should be down less compared to 2023 than Q3. But there is also a slim chance that Q4 could provide the first, and much needed, year over year quarterly improvement. First of all, Kohl’s Christmas season shopping is heavily influenced by the weather, the colder it gets, the more blankets, jackets, sweaters, and other fuzzy things that people buy. We have had a decent cold snap to start the holiday season so far this year compared to 2022 and 2023.

Also, the influx of the proprietary brands, the redeployment of the jewelry counters, petite sizes, and even the Trump election victory enthusiasm might provide some benefits to Kohl’s Q4 results. While my base case is that they underperform 2023’s $5.95 billion in revenue, there is a small chance they could beat it, possibly being the catalyst to a short squeeze, as Kohl’s stock is heavily shorted. Management guided last to a comp sales decline of around 6%, and that is a slight enough margin of error that a strong Christmas could surprise everyone. Not a prediction, just a possibility.

Kohl’s stock is heavily shorted, and while there are short reports and retail involvement, most professional shorting is purely quantitative. And quantitatively, Kohl’s has been in decline. I expect the shorting to stay brutal up until they have positive year over year improvement for several quarters in a row. There are very good odds that starting in Q1 2025, we could start to see year over year improvement. Especially since Q1 2024 was exceptionally weak, and the Sephora partnership will be deployed to all Kohl’s locations by then.

Another reason why I think the Kohl’s recovery could be explosive is because they have a corporate culture of doing share buybacks. Maybe 1,100 Kohl’s locations or so is all the country can really handle, so instead of burning cash on growth, management retires shares. It would only take a small recovery for management to have more than $200 million annual cashflow to support the dividend, and start pumping money into share buybacks again, especially at these currently depressed prices. The recent price weakness since Covid had even made their legacy repurchase programs that much more effective.

While I tend to focus on small caps, these muddling midcaps have been an important batch of earnings calls to listen to. National businesses have a lot of insight to share on the state of the overall economy. And it makes a great contrast, as above a certain market capitalization, the quality of the executives changes rapidly. There is still some risk at Kohl’s, but I believe the negative sentiment is overdone, and on a risk-adjusted basis, this is a great opportunity. Every near term four bagger is going to be at least a little risky. I could change my mind depending on Ashley Buchanan’s first earnings call, and as more quarterly results keep coming.

you son-of-a-bitch I'm in

Thanks for the write-up. The muddling mid cap series is really interesting as an exercise in estimating probabilities of the different outcomes, since the businesses often start getting more complicated with more moving parts compared to smaller companies. I appreciate you doing to work, it personally helps me learn more about analysis.

On a completely unrelated note, you should check out Perma-Fix Environmental Services (PESI). A near to medium term 3-5 bagger.

Initial write up on VIC here https://valueinvestorsclub.com/idea/PERMA-FIX_ENVIRONMENTAL_SVCS/9479507240

and covered by a fellow Substack author https://ideahive.substack.com/p/new-portfolio-position-ea1