What’s the Deal with Braskem? $BAK

FinTwit Favorite Series

Welcome to the FinTwit Favorite Series where I try to make sense of what everybody is so excited about.

“Oh my God, Becky, look at her volatility, it is so big, ugh

She looks like one of those Latam cyclicals, but, ugh, you know

Who understands those Latam cyclicals? Ugh, they only talk to her

Because she’s going to get acquired by the Kuwaitis, okay?

I mean, her volatility, it's just so big”

- Sir Invest-a-Lot probably

BAK Price:

Braskem S.A. (BAK) is the American Depository Receipt of a massive Brazilian petrochemical company. It has volatility, it has cyclicality, it has deep value, it has a struggle for control, it has BRICS issues, it has communism issues, it has environmental issues, it has tribal issues, it has legal issues, if you can think of it, Braskem probably has a problem with it. But just look at that chart, it’s perfectly degenerate. You can date Braskem, but for pity’s sake, don’t marry her.

I might call myself a degen, but my hat is off to

for having a 27.4% position in Braskem (BAK) as of July 1st. That is more concentrated than I like to allocate things, but if a position is deep value and is low risk enough, and if you aren’t using leverage, then game on. Is Braskem low risk? Let’s dive in.

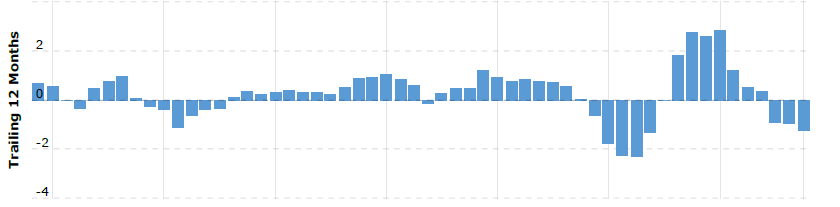

Starting with the business, Braskem is not a small cap, in the last 12 months, just the depreciation on their plant and equipment is larger than a lot of the small caps I analyze; over five billion reals, which is about one billion dollars. They make plastic resins, olefins, ethylene, propylene, butadiene, cumene, paraxylene, ortho-xylene, toluene, polyisobutene, isoprene, piperylene, nonene, and probably everything else that ends in “ene.” This is the stuff that comes out of the oil refinery that doesn’t get burned as fuel. Instead it gets turned into plastics, and a lot of other things, but mostly plastics. Braskem makes a lot of money when there is a boom in plastics, and they lose money when there isn’t. This means packaging, construction, and consumer goods. The next time those things are hot, Braskem is going to switch from losing $1 billion a year, to making $2 billion a year, and the market cap is currently $2.8 billion. With the end of the destocking cycle I discussed in the writeup for Forward Air (FWRD) as well as the construction boom from reshoring, we might be nearing the next good year for Braskem relatively soon.

BAK Net Income:

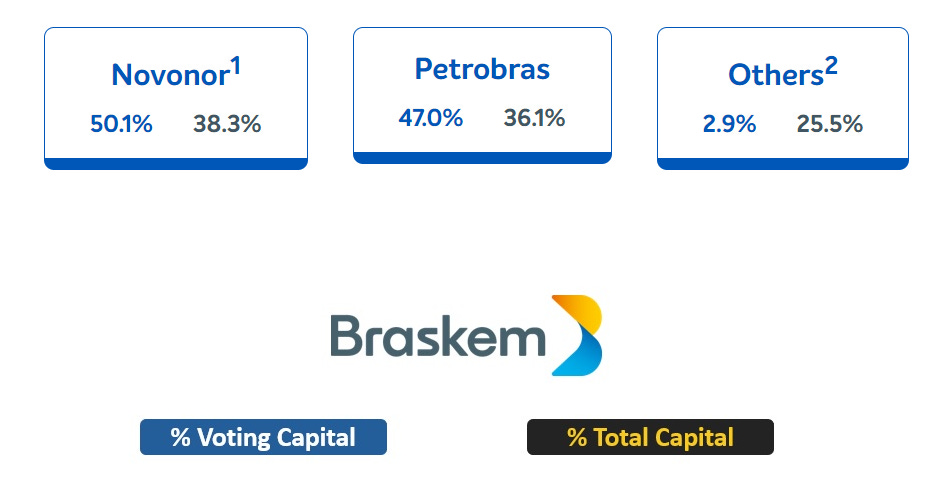

The cyclical income is not the reason why Braskem is blowing up on FinTwit, although it is the reason why I am starting to like it. The big attraction right now is that there have been outside offers to acquire Braskem. But so far those offers have failed. First a peek at their ownership structure, BAK has dual share classes, and the controlling shareholder with 50.1% of the votes and 38.3% of the ownership is Novonor, a private Brazilian company, who’s founder passed away in 2014, and is currently Brazil’s largest construction company. Since they need pvc piping and since BAK pays a semi-regular special dividend, it is not clear why they would want to give up control. Petrobras has a right of first refusal on Novonor’s shares, so while they don’t have a veto power, they can scuttle the deal in their own way as an outside investor would probably not want to spend billions just to be subordinate to the Brazilian government. Petrobras is the Brazilian state-controlled oil company who provides Braskem with their naphtha feedstock. And, Brazil is currently controlled by communists who aren’t particularly keen on decreasing their power.

Last year, the Abu Dhabi National Oil Company (ADNOC) explored acquiring Novonor’s stake in Braskem. The deal fell through. In 2018 LyondellBassell, the Dutch chemical company, attempted to buy Novonor’s stake in Braskem. The deal fell through. In 2016, the Chinese National Offshore Oil Corp (CNOOC) tried to buy Petrobras’ stake in Braskem. The deal fell through. Currently, Kuwait’s Petrochemical Industries Companies (PIC) is exploring trying to buy Novonor’s stake in Braskem. Now I’m no expert in pattern recognition, but… either Brazil is too dramatic of a place to do business, or Novonor is not an eager seller of Braskem. And why would they be, they don’t need anyone gouging them on their pvc piping. It isn’t entirely clear why retail investors would be so excited, it isn’t obvious someone buying out Novonor’s stake would imply that they would receive a tender offer as well. Maybe the market would react to the price paid, but maybe not. There is some scuttlebutt about retail investors finding some document that makes them think they have a ride-along provision to the transaction. I am not basing my portfolio decisions on what a Brazilian judge might rule on contract interpretation, they took away Bolsonaro’s social media accounts on a whim.

So is Lasse being foolhardy, is Braskem a risky investment? If you have an MBA and have been brainwashed into thinking that risk is the same thing as volatility, then sure. But are petrochemicals going obsolete in the next ten years? No. Is anyone lining up to spend $10 billion to build what Braskem has to compete with them? No. How is their liquidity? Braskem has 69 months worth of cash to wait for the next uptick in their commodity cycles. You might be concerned about the negative carry between having so much cash and so much long term debt, but that is just the cost of having a balance sheet that will bring you through to the next boom time, no matter what. It’s a reasonable strategy for the third world where you need an umbrella in case it rains.

What about their solvency? Braskem’s debt is about 70% denominated in US dollars. It has an average maturity of 12 years. In the past, this would have been a huge red flag for me, but seeing as how the US has probably chosen to go down the path of inflationary currency devaluation, having about $10 billion in long term debt to evaporate over time is a huge asset. Interest rates are mostly between 4.5% and 8.5%, with a particularly juicy 5.88% 3.7 billion BRL due 2050. How much purchasing power will the dollar have in 2050? Small caps typically don’t have access to long term debt this good.

The risk of dilution? The Brazilian corporate culture focuses on dividends and doesn’t focus on dilution or share buybacks much at all. While Vale is doing share buybacks, both Petrobras and Braskem have flat share counts for many years. The older generation of well-to-do Brazilians are all invested in their Brazilian majors, and rely on the dividend income, as the average take home pay of their version of social security is around 1,500 BRL or $300 USD monthly. Lula probably doesn’t want to suffer the political consequences of cutting off the elderly’s retirement income.

The risk of the communist government? During Lula’s first term from 2003 to 2011, Braskem paid out $3.44 USD in dividends for those 8 years, of course Braskem was a bit smaller at that time, and there was a global financial crisis. In those years, the state owned enterprises failed to spend enough on maintenance capex so that Lula could direct that money how he pleased. The consequences of that started popping up around 2012 or so. So far under this Lula administration, Braskem’s capex is unchanged, so perhaps that trick won’t be repeated this time around. I think the BRICS countries, even when they vote for communism, have the counterbalancing force of China keeping an eye on them, somewhat preventing extreme behavior.

Is Braskem deep value purely as a cyclical and not relying on some sort of strategic acquisition? It is trading at a price to peak sales of 0.15. From 2011 to 2024, BAK paid out $8.31 in sporadic special dividends over the time period, an average of $0.59 per year. At the current price of $7.21, that would equate to an 8% dividend yield. That’s pretty standard for a cyclical in a dangerous jurisdiction, so relying on dividends alone would not make BAK suitable for a value degen. The stock price passed $20 a share on a share count adjusted basis in 2000, 2004, 2005, 2011, 2017, 2018, 2019, and 2021, or 8 out of the last 24 years, and only went at most 6 years between peaks. Being three years already from the last peak, the probability of tripling your money within the next three years is pretty solid. If it takes until 2027 to sell Braskem at $20 a share, including a special dividend or two, that would be an internal rate of return of 46%. Of course if the price passes $20 in 2025 or 2026, the rate of return is much higher. But it is important to sell, because plastics are a garbage cyclical business that goes through years at a time of losing money.

So to Lasse, who I assume is Scandinavian, may you find glory in Braskem and may your courage take you to Valhalla. I won’t be 27% long BAK, but on the next portfolio reshuffle, if the price is still down I might be 1%-2%. The risk that Jerome Powell causes an international dollar shortage with high interest rates is a real threat to Braskem’s dollar denominated bonds, and Lula could come up with a new way to destroy Brazil’s business climate. I put both of those risks as very small, but not negligible.

You know you're an honorary Latino when you: cover BAK, warn of dating volatile 'assets' and refer to combustible as 'Nafta.

Solid write-up ! You are able to turn such a boring company into an engaging and learning exercise. Bravo !