The Structure of a Commodity Supercycle…Maybe. Taseko Mines $TGB

There seems to be a consensus going around regarding the commodity supercycle that gold leads, and oil follows. Well, I dug into the data, and it isn’t necessarily true.

In the 1890’s copper was the first mover, followed by oil and then gold.

In the 1930’s gold was the first mover, followed by copper and then oil.

In the 1970’s gold was the first mover, followed by oil and then copper.

In the 1980’s oil was the first mover, followed by copper and then gold.

In the 2000’s copper was the first mover, followed by oil and then gold.

It appears that copper leads in industrial booms as it is needed in construction and manufacturing expansion. Gold leads in monetary shocks when inflation fears dominate. And oil leads in geopolitical shocks as OPEC flexes its muscles.

What we have seen so far is gold leading this commodity cycle. But will oil follow? It is true that we do have geopolitical shocks, but unlike past geopolitical shocks, now the US is producing shale oil.

Even though we are in an unstable time with wars in Ukraine and in the Middle East, for the moment the artificial intelligence revolution is the dominant theme. For this current cycle, I find it a lot more likely that copper will follow next, and even though copper miners have started to rally off their lows, I have this nagging feeling that I don’t own enough copper miners.

We are in an industrial boom, after all, although it doesn’t feel like it at the moment with Trump’s tariff uncertainty weighing on industry generally. But that tariff uncertainty will start to slowly fade, and with interest rates coming, the reshoring industrial demand will add to the data center buildout. I think now is the time for copper, and oil will join the party eventually.

In June of last year I wrote about three copper miners, Hudbay Minerals (HBM), Ero Copper (ERO), and Taseko Mines (TGB). At that time I preferred Hudbay Minerals, as their management team was able to drive incredible efficiency, and the TGB buildout was too far away to drive prices. In December I reprised that writeup, and I included TGB as a good choice to buy at current prices.

But now that the TGB buildout is just around the corner, I don’t believe it's anywhere near priced in. In a world where not a lot feels cheap, I am willing to start adding to Taseko Mines every week.

Taseko Mines is a Canadian domiciled, US listed junior copper miner with one producing mine, one under construction nearing completion, and three large greenfield deposits. Management owns about 3.2% of the company, and despite new production coming online in Q4 2025, analyst price targets are almost all within 10% of the current price. You have to love those analysts and the way they chase the price as it runs away from them.

The producing mine is a traditional open pit called Gibraltar, it produces a blend of copper and molybdenum, and it’s in British Columbia. Taseko management acquired the shuttered mine for $1 in 1999, and then spent $800 million modernizing it. Now it has 32 year life, and in 2024 it produced 106 million pounds of copper with a cash cost of $2.30 per pound. Management prefers to use cash cost instead of all-in-sustaining cost, so it’s on us to look at the capex on our own. Production for 2025 is projected to be around 120 million pounds, and US dollar cash costs are stable, but Canadian dollar cash costs are exploding due to exchange rate differences.

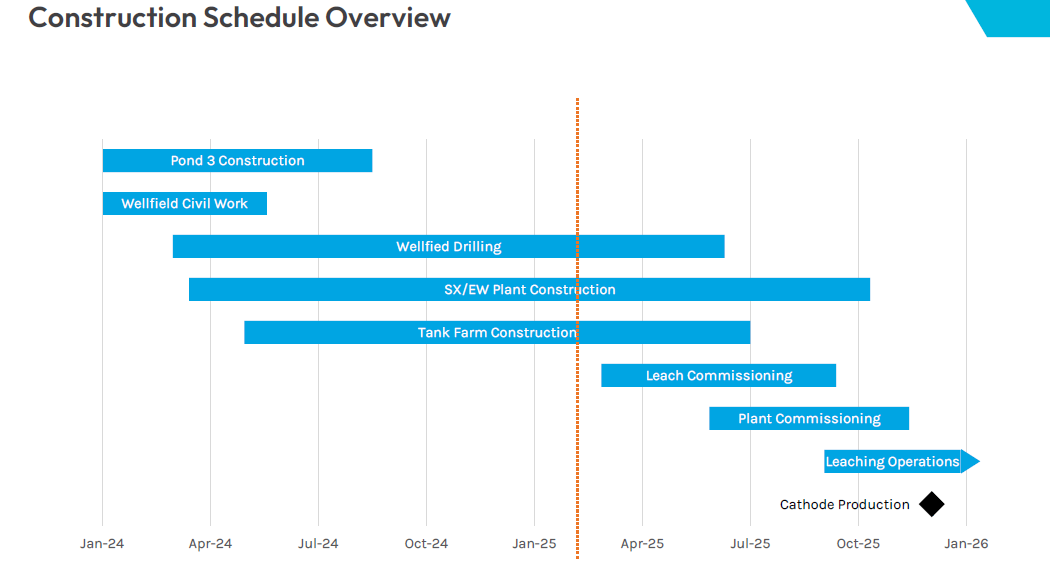

The mine under construction is very interesting, it’s an in situ copper mine in Arizona. In situ copper mining has a long history, the Greeks were doing it in 200 BC, and the Chinese were doing it around 900 AD. But the geology that is appropriate for in-situ mining is not extremely common. The Florence copper project has a geology with a highly permeable, naturally fractured ore body that is under the water table, and it contains soluble copper minerals. Since the copper comes out of the ground already dissolved, it bypasses the need for an ore mill.

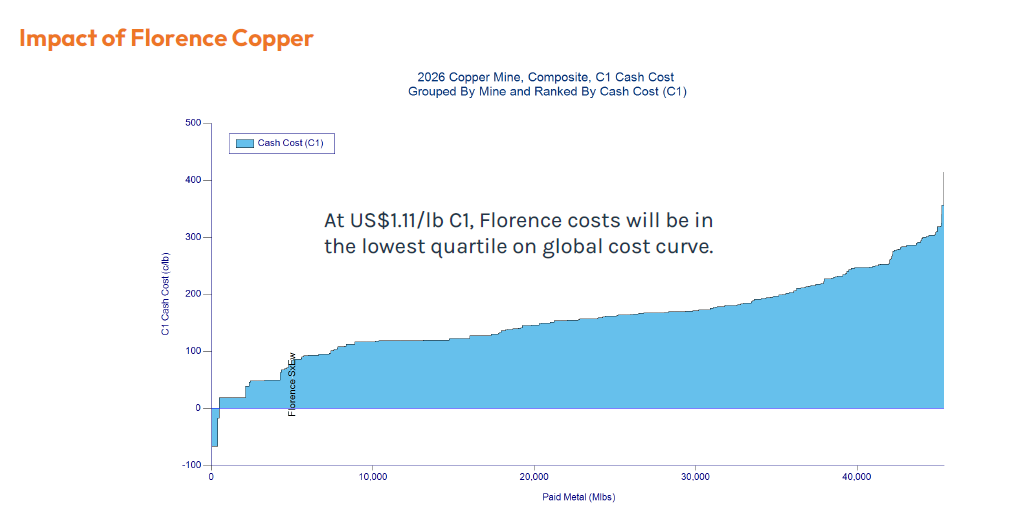

What makes in situ mining so attractive is the extremely low up front cost, and the extremely low cash costs of production. Florence is only projected to cost about $235 million to build out, although it was acquired from someone who had spent $150 million building the infrastructure. The asset was acquired in an all stock deal, for a cost of around 75 million CAD and is projected to have cash costs of production of around $1.11 per pound of copper produced, placing it squarely in the first quartile of the copper cost curve.

Taseko funded Florence three ways, they sold a royalty for $50 million, Mitsui contributed $50 million, and the rest is from Gibraltar’s cash flow. The royalty is from Taurus Mining Royalty Fund, and they get 2.05% of gross revenue for the life of the mine. Mitsui gets a 2.67% copper stream, plus an offtake agreement to buy 81% of copper cathode produced for the first few years. Mitsui has the option to buy a 10% stake in Florence for another $50 million, but for now it is 100% owned by Taseko.

The Florence mine is projected to produce around 85 million pounds of copper per year, ramping up slowly in Q4 2025 (which is 15 days away as I write this), and reaching the full run rate sometime around 2027. With such a low cash cost, Florence is projected to add about $325 million of EBITDA to Gibraltar’s current $250 million of EBITDA.

There are three other greenfield deposits, two for copper and one for rare earths, all located in British Columbia, and all much more than five years away from production if started today.

New Prosperity is a copper / gold porphyry. If constructed, it would have a 33 year mine life. In order to get approval from the indigenous tribes, however, Taseko is contributing a 22.5% ownership stake to a trust for the benefit of the Tsilhqot’in Nation.

The Yellowhead project has a projected upfront cost of $2 billion for a 25 year mine life. It’s a traditional open pit copper mine with a projected 206 million pounds of copper annual production for the first five years, and 178 million pounds average for the life of the mine.

And then there is the Aley Niobium Project, with a projected mine life of 24 years, and 84 million tons of 0.5% Niobium Oxide content.

At current prices, feasibility studies put the payback periods of New Prosperity around 4 years, Yellowhead around 3.3 years, and Aley at over 5 years. Management has guided that the Yellowhead mine would be the next in line to develop, which is comforting because at current prices it has the best economics.

But now on to trying to value Taseko. With the market almost completely ignoring the Florence project coming online sometime within the next few months and ramping up into 2027, Taseko is by far the cheapest copper miner based on 2027 production.

At the expensive end of the list, Southern Copper has an $80 billion market capitalization for projected 1,000,000 tons of 2027 copper production. You would be buying 2027 production for $80,000 per ton of capacity. Freeport McMoRan is considerably cheaper, $60 billion gets you 1.95 million tons of production for $30,000 per ton. Antafagasta is similar at around $33,000 per ton.

But small caps trade more cheaply, Hudbay Minerals which was my preference in past writeups is on track to produce 180,000 tons in 2027 for a $55 billion market capitalization. That comes out to about $29,000 per ton of capacity. Ero Copper is considerably cheaper at around $17,200 per ton of capacity.

But then you have Taseko, who is so incredibly overlooked that their projected 88,000 tons of 2027 production is being valued at $12,841 per ton. TGB is less than half the price of HBM, and this doesn’t take into account the enormous cash flow from the low cost of in-situ mining.

From a projected EBITDA perpsective, HBM is trading at 4.74x projected 2027 EBITDA at $4.50 copper. ERO is trading at 4.46x projected 2027 EBITDA at $4.50 copper. And TGB is trading at a humble 3.07x projected EBITDA at $4.50 copper.

Once the production from the Florence mine starts rolling in, Taseko mines room to rise over 50% on a relative basis to catch up with peers. Beyond that, the copper price can drive further gains. At $5.50 copper, TGB is trading at 2.1x 2027 EBITDA. The historical average for junior copper miners is between 4.5x and 6.0x EV / EBITDA.

Taseko Mines (TGB) $3.66: $5.50 by the end of 2027 at $4.50 copper

Taseko Mines (TGB) $3.66: $7.84 by the end of 2027 at $5.50 copper

Thanks for this article. I opened a long position the day after I read it and have added since