The Burning Question: Staffing, Kelly Services $KELYA vs. ZipRecruiter $ZIP

Team VD Collaboration

Introducing a collaboration between

(VDL) and (UVD).With VDL and UVD, please clap for Team VD!

You’re gonna really love this collaboration, opportunity is contagious when VD is going around.

Today’s Burning Question is which staffing company is better, Kelly Services (KELYA) or ZipRecruiter (ZIP)?

Colin has recently written about Kelly Services:

And Steve has recently written about ZipRecruiter:

An Overlooked Trump Trade, Staffing Companies: Manpower $MAN, GEE Group $JOB, ZipRecruiter $ZIP

“Socialism never took root in America because the poor see themselves not as an exploited proletariat but as temporarily embarrassed millionaires.” - Ronald Wright interpreting John Steinbeck

Kelly Services is a more traditional, brick and mortar, staffing and temp agency, possibly the market leading temp agency. Jobseekers who start out as a temporary worker have their payroll processed by Kelly who is paid by the employer. This causes huge revenues and thin margins. Some temporary positions do turn into full time job offers after a period, many do not. Kelly also is expanding to other aspects of the staffing industry, but they are still known primarily for their temp agency business which did $4.3 billion of revenue in 2024.

ZipRecruiter manages an online, artificial intelligence powered, job posting board. They are paid a subscription fee by employers who post on their site, which in 2024 had revenues of $474 million.

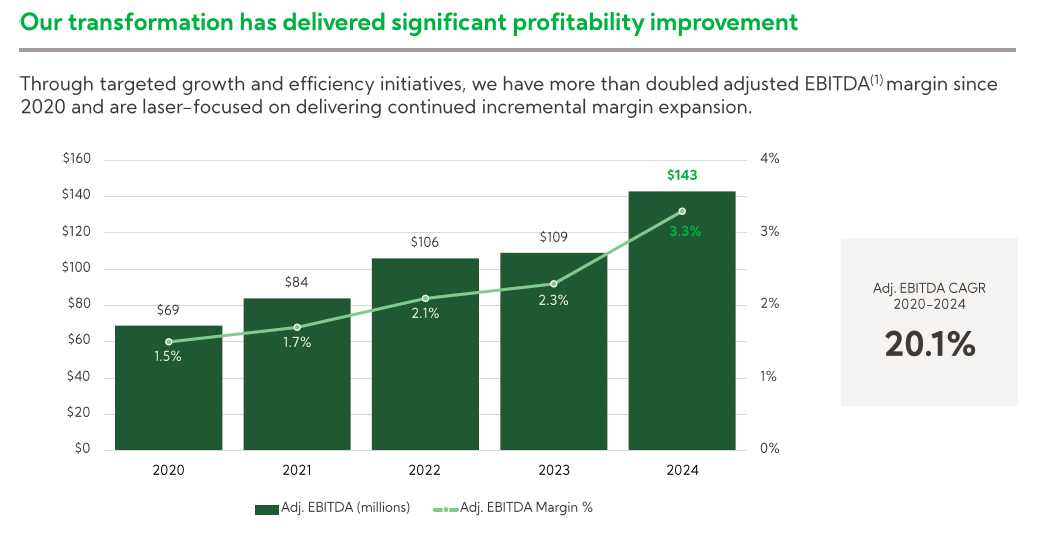

One of the biggest differences between the two is their adjusted EBITDA margins, with KELYA up to 3.3% in 2024 from 2.3% in 2023. Meanwhile ZIP is down to 16% EBITDA margin in 2024 from 2023’s 27%.

Both firms have suffered a decline in revenues from their peak in 2022, but KELYA is down to $4.3 billion from a peak of $5.0 billion, a 14% drop. But ZIP is down to $474 million from $905 million, a 48% decline. The reason for the large collapse in ZIP’s revenues is possibly the effect of AI and tech’s year of efficiency on white collar employment.

Given the vastly different margins, each company trades at wildly different multiples. In the last 15 years, KELYA traded at a peak of 0.19x price to sales ratio. But ZIP traded at over 3.0x price to sales just a couple of years ago. The multiple compression both have experienced is comparable, with KELYA down to 0.11x price to sales, and ZIP down to 1.22x price to sales. A return to peak multiples would be approximately a double for either company, but a return to peak multiples and peak revenues would make KELYA a 2x return, but it would make ZIP a 4.7x return.

I think Colin might be on to something with KELYA, over the last five years, they have more than doubled their EBITDA margins from divesting of unprofitable divisions and focusing more on contract employment over temp employment. This means that on the next rally higher, past peak multiples might even be exceeded.

In other words, for KELYA, the business has already transformed, and it’s just a waiting game for multiples to catch up to the fundamentals. In the case of ZIP, the opportunity is much greater, but the fundamental problem hasn’t been solved yet. The white collar market is still frozen, and it isn’t entirely clear at what point the AI revolution will result in more white collar hiring. In one believes in doomsday scenarios, there could be tens of millions of white collar workers who need to learn to weld, plumb, or groom dogs. I think the doomers are overly pessimistic, but it does remain as a threat to ZIP’s rebound.

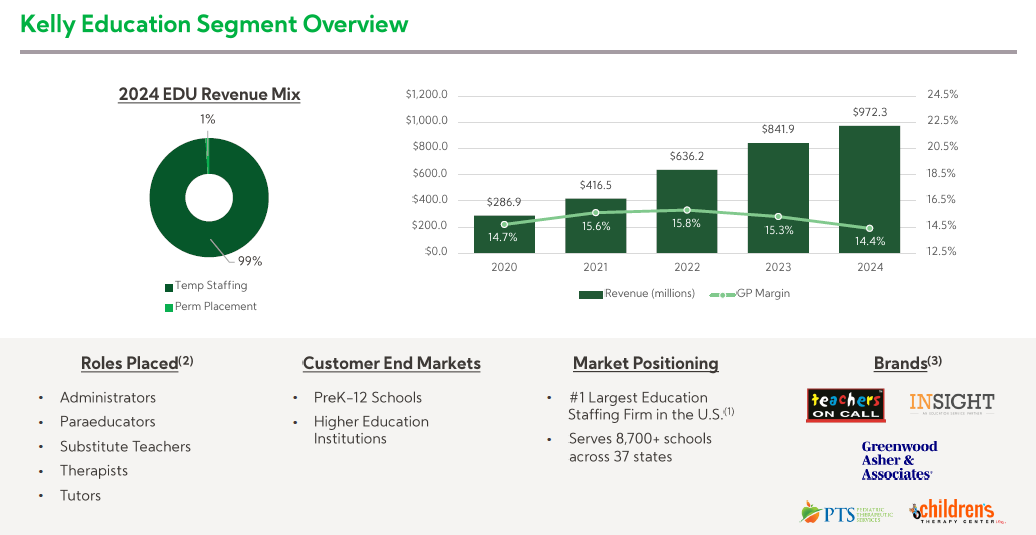

Different aspects of the labor market are thriving while professional hiring struggles. For KELYA, science, engineering, and technology revenues have grown from 23% to 33% of in the last five years. And education as a category has grown from 5% of revenues to 16% over the same time period. The job market isn’t terrible for lab technicians and substitute teachers, it’s just terrible for “professionals.” KELYA with several business segments in an aggressive growth trajectory make it even more likely that past peak multiples will be exceeded.

With expanding profitability, and an aggressive recent selloff, KELYA strikes me as a relatively conservative way to double your money in probably two years as the market rerates. After this small cap selloff since November, I’m not against a “base hit” strategy. I don’t have to swing for the fences every time.

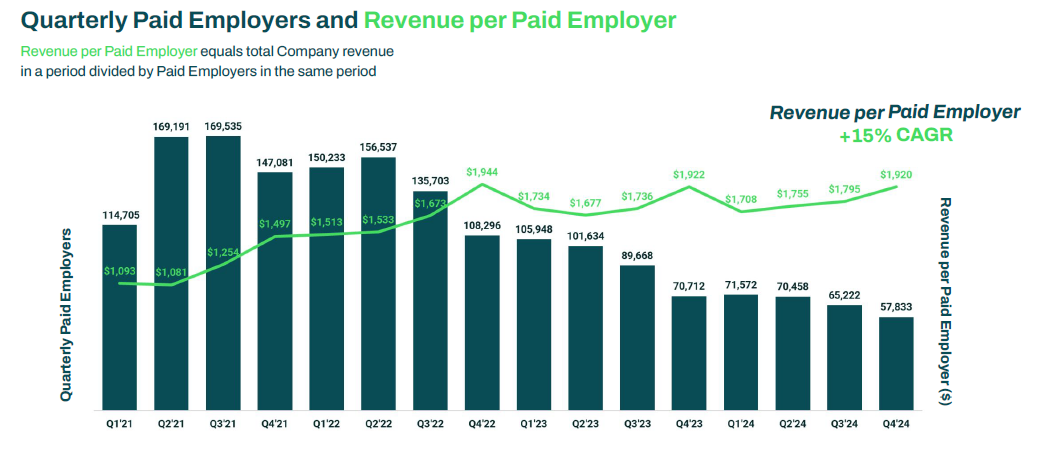

But for those of you who do want to swing for the fences, ZIP has been improving under the surface as well. While the number of employers who are hiring is down, ZIP has been focusing on increasing revenues by adding more value to the people who are hiring. The employers who started using ZIP in 2017 went from paying $250 a month to $1,060 a month over eight years. But the employers who started with ZIP in 2023 went from paying $482 a month to $956 a month in one year as ZIP has become better at demonstrating their value proposition to customers, deepening relationships faster over time.

So the next time that white collar hiring is in a frenzy, whether that be in two years or in five, if ZIP is able to maintain or grow market share, revenues could easily be double on the same volume of job seekers.

While ZIP is a 4.3x on a return to past peak multiples and revenues, on a return to past peak customers, that number is more like an 11x return. The 48% decline in revenues is understating the 66% decline in employers using the ZIP platform. However, it’s not entirely clear whether or not ZIP has permanently lost market share. Some very rough estimates would put ZIP’s market share of the online recruitment marketplace up from 5% in 2020 to 10% in 2022, and back down to 5% in 2024. The ultimate question for ZIP is whether their decline in market share is due to the type of jobs that tend to get posted on their site, or due to increased competition from Indeed and LinkedIn. The answer to that question is beyond me, but I am encouraged that ZIP’s sticky employers are paying up for a deeper relationship. While low risk 2x opportunities like KELYA are abundant, an 11x opportunity will almost always come with a dash of uncertainty for extra flavor.

Kelly Services (KELYA) $13.24: Price Target $26 by the end of 2026

ZipRecruiter (ZIP) $6.19: Price Target between $25 and $64 at some point between 2026 and 2028

| A guest post by

|