An Overlooked Trump Trade, Staffing Companies: Manpower $MAN, GEE Group $JOB, ZipRecruiter $ZIP

“Socialism never took root in America because the poor see themselves not as an exploited proletariat but as temporarily embarrassed millionaires.” - Ronald Wright interpreting John Steinbeck

One little piece of news that slipped past a lot of people’s radars was the sudden spike in small business sentiment after the Trump victory. I know the talking heads on the financial news spend most of their time talking about big business, and I know that big business employs most Americans. But, big business does not create most jobs. Typically, small businesses create jobs, are eventually acquired by bigger businesses, and big businesses look for efficiencies and downsize the acquired employees.

On a recent family trip to St. Augustine, Florida, I was surprised at how many little tourist shops had Trump stickers in their windows. Decades ago, it would have been easy to find left-wing small business owners alongside right-wing small business owners. It might have been hard even then to find right-wing government employees. But it seems that the United States has polarized, and the political parties are increasingly less about ideologies and are more about class, the class of government employee versus the class of small businessman. The Trump victory just invigorated the small business community, and the small business community is who creates most jobs.

Just look at those two vertical spikes on the graph, both in November of a year that Trump won the election. 2016 and 2024. Small business owners think of Trump as their guy. They really do think of themselves as “temporarily disgraced millionaires” and they see themselves in Trump. How else do you explain a small business optimism index where even though earnings trends are a bit less than in 2023, more businesses think it’s a good time to expand, plan on making capital outlays, and plan on increasing employment? Especially when they don’t expect higher real sales, and don’t expect better credit conditions.

I had previously written about staffing companies as a special for Labor Day. The timing wasn’t great then, and most of the companies are trading below their price on Labor Day. I have a filthy habit of being early, but I have a sinking suspicion that all the staffing companies are going to report an increase in volumes on the very next earnings call due to this increase in small business hiring starting in January after the Christmas season. Small businesses tend not to hire much during December.

Happy Labor Day! Manpower $MAN, HireQuest $HQI, and ZipRecruiter $ZIP

I remember when I was young and Labor Day was about having a day off from school and possibly even a barbeque. It was long before I learned about the Marxist paradigm of the bourgeoisie versus the proletariat. Even in today’s world where the typical employee with a 5% 401k match with compound interest will earn more as a capitalist than through their …

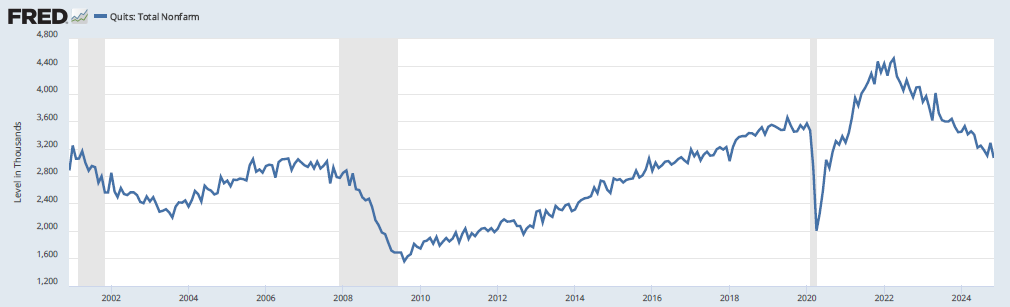

But small business hiring isn’t the only aspect of staffing companies’ volumes, another major component is the quits rate. The rate of employees quitting their jobs for better opportunities has been in a 26 month decline, matching tech’s year of efficiency, now going over two years. Staffing agencies are calling it, “The Great Stay” as employees stay at jobs out of fear of not being able to find another. The drawdown of about 1.5 million in the Total Nonfarm Quits is of equal magnitude to the 2008 Global Financial Crisis.

“If something cannot go on forever, it will stop.” - Herb Stein

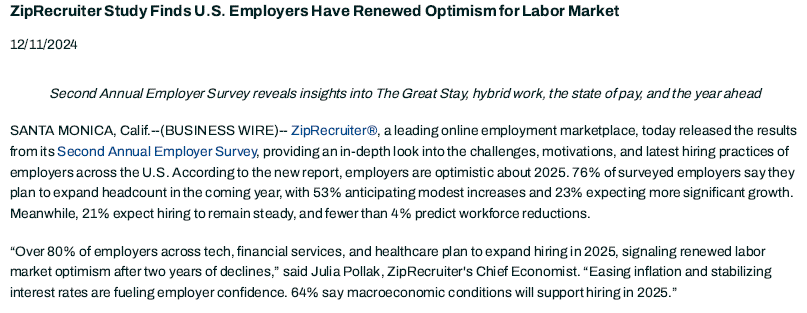

Zip Recruiter did a survey of employers on December 11th, 2024, what they found was that over 80% of employers in tech and finance are planning on increasing hiring in 2025. The year of efficiency seems to finally be coming to an end. With an increase in hiring, the frozen labor market might start to thaw out, with results potentially coming as soon as this upcoming quarter’s earnings calls.

There are a lot of potential staffing companies, and the largest, Robert Half (RHI) is only a $7 billion market capitalization, so they are all mostly small caps. A few names stand out as very interesting. First, even though RHI has the largest market capitalization, Manpower (MAN) has 3x their revenue volume, and less than half of their market capitalization. A company that still has positive GAAP net income, however small, shouldn’t be trading at a price to sales ratio of 0.14x. The CFO agrees, he just spent $500,000 on an insider purchase. MAN isn’t my favorite name in the space, but an inside purchase from the CFO, extremely cheap valuation, and a secular inflection to tailwinds make a compelling case. It’s worth noting that this CFO has previously sold all of his stock on two separate occasions, and this is his first purchase. Not all insider behavior is signal through the noise, but a day-trading CFO is almost as good as a purchase by Nancy Pelosi.

There are microcaps if you prefer, GEE Group (JOB) has a $25 million market capitalization, no debt, they have been buying back a tiny bit of shares here and there, and management believes the market is turning around soon. With $116 million trailing twelve month revenue, $162 million at the peak in 2022, JOB trades at a price to sales ratio of 0.22x. Earnings look terrible due to an asset impairment charge, but that is a non-cash event. There is insider buying from the CEO, CFO, and several directors, all at prices higher than where the stock trades today. Three days ago JOB announced an acquisition of an Atlanta based staffing company, Hornet, for cash and seller financing. The details of the transaction were not disclosed. I don’t usually write about microcaps, they are illiquid and often operated by scoundrels who are happy to abuse retail gamblers who are happy to be abused for the chance to win the multibagger lottery. But the insider behavior is very strong here.

My favorite name in the space is still ZipRecruiter (ZIP). They aren’t the cheapest, and there isn’t insider buying, but they are a tech platform and they fit in with my theory of the Revenge of Cathie Wood when small cap tech rallies back to traditional multiples. Over the last two years, ZIP has been focusing on their technology platform, and if 2025 really is the year of agentic artificial intelligence, ZIP has their AI agent, Phil. Phil will help to generate an applicant’s resume and flesh out their work history. Phil will also generate an employer’s job posting. So yes, Phil will mostly be talking to himself. Meanwhile, ZIP’s fifteen years of proprietary data and machine learning will be helping to successfully match employers with employees based on what little information they give Phil. A recent rollout of the “Invite to Apply” program has dramatically increased matching success rates, and during this down time in the market, ZIP has taken market share from their larger competitors, Indeed and LinkedIn.

ZIP doesn’t have insider buying, but the co-founder is still the CEO, and the company does engage in share buybacks. Quarterly revenue is down to $114 million from the 2022 peak of $240 million, but EBITDA margins are up, market share is up, and revenue per employer has grown at a 14% annual rate since 2021. Also, ZIP believes that they have reached the final stage of brand awareness, and while targeted marketing might increase as the market recovers, general marketing should decrease as a percentage of revenue, potentially leading to margin expansion from 20% to a long term run rate of 30%.

Listening to earnings calls, I find that management is sharp, has a credible plan, and is executing on that plan. I wish I could say the same about Opendoor (OPEN), Cardlytics (CDLX), and Teladoc (TDOC), but I own those companies for the size of the opportunity, and I foolishly tolerate a floundering management to my own detriment. But ZIP has much more promising leadership that has led the company to successful 15% ish annualized growth against their competitors with much deeper pocket books.

A return to peak sales of around $1 billion, and a return to a price to sales ratio of approximately 4.0x, which is conservative for a 15% annual revenue growth tech business, in addition to the share buyback program, would put a share price target on ZIP of $47 up from the current price of $6.81. I think it’s a reasonable prediction to think that the labor market should thaw out in about two or three years. That’s a seven bagger, give or take, and without the potential growth from ZIP’s recent international expansion.

ZipRecruier (ZIP) $6.81: $47 by end of year 2027

gee groups' q4 report was pretty depressing to read.

Good write up and price targets. Just seen ZIP has recent insider buying and selling (Dec 2024), including the CEO more recently on 6th Jan 2025 (direct buy & additional sell through family trust). Could be a time to take a long position but will have to do a bit more digging. Cheers.