South American Oil Junior Thunderdome: Petrotal $TAL.TO vs Geopark $GPRK

Thank you to Fabio at Capital Mindset for hosting me on his podcast recently. I am grateful for any opportunity to reach a new audience.

We started talking about the three Silver Tsunami stocks, Jackson Financial (JXN), Abacus Life (ABL), and Finance of America Companies (FOA), and then moved on to commodities. Fabio told me to take a quick look at one of his favorites, PetroTal (TAL.TO). Petrotal is Canadian domiciled, Houston headquartered, and Peru’s largest public oil company with production of a whopping 23,225 barrels of oil per day. I think it’s useful to do a side by side comparison with a similar company, GeoPark (GPRK), the US domiciled, Bogota headquartered, junior Colombian oil company with 33,000 barrels of oil per day production.

I have also previously written about Parex Resources as well, they are a bit bigger than PetroTal or GeoPark, and their margins are a bit thinner. Parex produces mostly natural gas for the local Colombian market. Natural gas is considerably less liquid than oil, and it needs less refining. Separating the propane and butane out of the mix is much less expensive and less capital intensive than cracking crude oil. Also, natural gas is harder to ship, allowing for regional prices instead of global prices. This has benefitted Parex, however, either through overproduction or an expansion in US export terminals, those prices could eventually come down. Think tanks and forecasters are predicting natural gas prices to rise considerably in Colombia in the near future, however, as domestic natural gas is $3.70 per mmBtu and imported is over $13 per mmBtu. Colombia is facing a domestic shortfall going in to 2026, so Parex could have some near term tailwinds instead of headwinds.

Two dry holes, wasn’t that a punch line from the Golden Girls?: Parex Resources $PXT.TO

Welcome back to the “Probably Not a Value Trap” series where I discuss businesses with a 10%+ dividend yield which I believe probably won’t get cut and why, but don’t come after me on Twitter if they do.

But first, why am I still hung up on the energy sector? The market capitalization of energy companies is around 3% to 4% of the S&P 500, but the earnings of energy make up closer to 10% of the S&P 500’s earnings. Energy was as high as 12% of the S&P 500 market cap within relatively recent history. So either the marketplace is prudently pricing declining earnings from the obsolescence of oil, or energy companies are undervalued. I, personally, do not believe that oil is going away anytime within the next 30 years, so I am bold enough to want to stuff my portfolio with energy stocks. Either they will catch a multiple rerating over the coming years as the market shakes off its ESG fever dream, or they will remain the new tobacco, and will be able to buy back their own stock aggressively at the cheap valuations.

Why invest in oil companies in South America? In the US, we have been drilling for oil since the days when Rockefeller first standardized a replacement for whale oil lamps. But in plenty of other places in the world, there hasn’t been a hundred years of property rights and wildcatting to discover all the easily accessible oil. Colombia especially has been a failed state for so long, nobody in their right minds would have explored aggressively for oil until recently. This means that oil discoveries with low lifting costs can be made with less capex, but good governance and rule of law is still a work in progress.

Peru ranks third in South America for rule of law, if the World Bank’s data is accurate. But Chile and Uruguay stand alone with scores that one would consider investment grade. It would be fair enough to call third place a three-way tie between Peru, Colombia, and Brazil. Of the three, Colombia seems the most likely to be more market friendly after the next election. The current president, a literal guerilla fighter from the mountains, is wildly unpopular and ineffective. In Colombia it is assumed that the right-wing party will win, but in the past that hasn’t always guaranteed a market-friendly administration. In Brazil, Lula is probably too old to run for office again, but it is much less clear who will replace him. I believe that the recent drama surrounding the Petrobras dividend indicates that modern South American socialists are reluctant to disrupt their economies, and they are exhibiting self-restraint. If only the socialists of developed economies were so self-aware.

But in Peru, things are really a mess. The prior left-wing president was arrested for corruption, and his vice-president, formerly left-wing, but now in coalition with the right-wing, is market friendly, prohibited from running for the presidency again in 2026, and even if she weren’t, has a 2% approval rating in the polls. Out of the 54 registered political parties, nobody has a clue who Peru’s next president will be. But, whoever it turns out to be will likely be confronted with a market-friendly congress who will try to hold the line in favor of economic growth, as they have done since the 1990’s. Peru’s GDP has grown from $28 billion to $303 billion, compounding at over 7% for the last 35 years, now a stone’s throw away from overtaking Portugal and rivaling South Africa. So their congress must be doing something right.

PetroTal’s all-in cost, including royalties to the government, is about $35 per barrel. With Brent averaging around $75, they have been generating about $40 of EBITDA per barrel of oil sold. I know oil prices are bit low at the moment, and I can’t predict when the cycle will turn, but PetroTal is unlikely to be the marginal producer that goes bankrupt. For 2025, PetroTal is guiding toward $30 a barrel EBITDA margins, reflecting $65 Brent.

I was saying previously, that South America hasn’t had one hundred years of wildcatting, so their reserves mostly still have yet to be found. PetroTal has been able to prove new reserves for $8 a barrel, which is a fraction of the exploration costs for many of their peers in other countries. At $75 Brent, for every barrel of oil that PetroTal sells, they get enough EBITDA to prove five more barrels of reserves. They don’t spend 100% of EBITDA on exploration, but it’s an interesting way to think about it.

PetroTal is guiding toward $240 million of EBITDA for 2025. Out of that, $40 million goes to the tax man, and $140 is earmarked for drilling. That leaves $60 million for dividends and buybacks. Sadly, most of that will go toward dividends, the buybacks are only implemented heavily when Brent is high. But in the meanwhile, a 13% dividend yield isn’t a bad consolation prize while one waits for the oil cycle to turn.

The strong emphasis on growth capex, $140 million out of $240 million, has generated a production growth rate of 56% annually, growing from 958 barrels per day in 2018 to 22,000 barrels per day in 2025. Of course those growth rates are unsustainable, but for the last two years have been steady around 24%. Over those seven years, proven reserves have grown at 19% annually. The reserve growth has been somewhat affected by the fact that PetroTal’s flagship field, Bretana block 95, is on a lease from the Peruvian government until 2041. And PetroTal has already proven enough reserves to maintain production until the end of the lease. At this time it is uncertain whether or not the Peruvian government will allow PetroTal to keep operating Bretana after 2041, although management indicated they have good odds to be able to obtain a lease extension.

PetroTal’s current goal is to become a multi asset producer, engaging in exploration at four additional locations within Peru; Zapote, Iberia, Tapiche South, and Lead E. Until they are able to produce significant volumes outside of Bretana, PetroTal’s entire business is tied to Block 95.

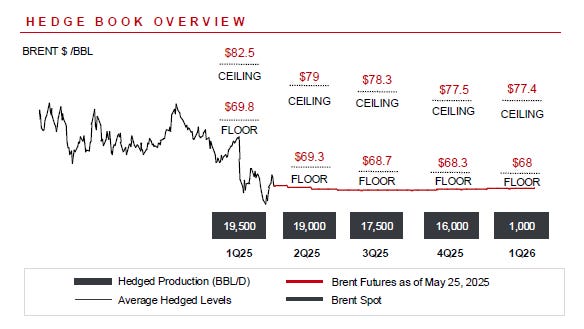

Comparing PetroTal with GeoPark, GeoPark is already producing 33,000 barrels per day as of last quarter, comapred to PetroTal’s 22,000. Both have extremely similar margins, GeoPark has a 61.8% EBITDA margin in 2024, and for PTAL that was 60.0%. Which makes sense, both companies are selling Brent, and drilling in places that haven’t been picked over too much. PetroTal was clever enough to place some hedges when Brent was at $80, but some of those hedges are already starting to roll off. Still, about 40% of 2025 production has a floor of $65 Brent. GeoPark has a similar hedging book.

GeoPark:

GeoPark has an even more ambitious growth trajectory than PetroTal, aiming for 70,000 boe/day by 2028 from their current 33,000, but of course this comes at the cost of returning capital to shareholders today. GeoPark’s forward dividend yield is 8.75% compared to PetroTal’s 13%, and GeoPark is allocating just $30 million annually to the dividend compared to PetroTal’s $60 million.

Both companies have similar reserve life proven, about 8 to 10 years. But PetroTal has a pristine balance sheet, whereas GeoPark has over $500 million in long term debt mostly maturing in 2030. I’m not against leverage, I’ve even been accused of focusing on over-levered shitco’s. But sometimes it’s better not to double down on risk. South America already has jurisdictional risk, they don’t need leverage on top of that. However, GeoPark’s $500 million of long term debt is only about 1.25x 2024’s EBITDA, and 2025’s production is considerably hedged. If there were some sort of interest rate crisis, it seems unlikely that GeoPark wouldn’t be able to meet their 2030 obligations, and maybe PetroTal could use a little more torque.

GeoPark is already regionally diversified, with 5,000 barrels per day coming from the Vaca Muerta in Argentina. If you absolutely must own South American shale, GeoPark is one way to do that. I am more focused on traditional oil drilling in South American jurisdictions that haven’t been fully explored, so the Vaca Muerta isn’t a huge attraction for me. And while diversification is nice, my portfolio is diversified by having more than one energy company. If Colombia were to surprise everyone and have an incredibly hostile regime after the next election, GeoPark would suffer enormously, even with the exposure to Vaca Muerta. PetroTal is still trying to diversify away from a single asset with a lease that expires in 15 years, but still within Peru.

Both companies are undervalued even compared to their own price history, although the organic growth is so rapid that the decline in market capitalization per barrel of oil of daily production is a bit masked. PetroTal was at CAD 0.87 per share in 2022, when production was 12,000 barrels per day. Today their share price sits at CAD 0.58, and the buybacks have shrunk the float by 10%. GeoPark was at $17 per share in 2022 compared to $6.75 today, but production has actually declined over those years from 37,000 barrels per day to 33,000. It is only recently in 2023 that GeoPark has embarked on this ambitious drilling program to hit 70,000 barrels per day in 2028 and 100,000 in 2030. GeoPark suffers from rapidly declining production at their core asset, the Llanos 34 block in Colombia, and the last two years of growth in other areas have only kept overall production close to breakeven. GeoPark started their journey 22 years ago, and Llanos 34 has paid a lot of dividends to shareholders over that time, but it isn’t doing many favors for shareholders who want to invest in GeoPark today. Although GeoPark has shrunk their float by 20% in the last two years. PetroTal only started production at Betana in 2018, and the keystone asset still has a growth runway ahead of it potentially reaching 40,000 barrels per day alone.

The enterprise value of the two companies are a lot more similar than their market capitalization. GeoPark has more debt, but in the fashion of South American companies, also has much more cash on hand. PetroTal is trading at a market capitalization that is about 2.4x 2024 EBITDA. GeoPark is trading at a market capitalization that is about 0.84x 2024 EBITDA. But when you include the debt and cash calculation and switch to enterprise value, you get much closer with PetroTal at 2.2x 2024 EBITDA and GeoPark at 1.7x 2024 EBITDA.

Choosing between the two, Colombia probably has the more predictable and more favorable 2026 election, however, I am very impressed by Peru’s congress which has restrained their presidents for the last 35 years. GeoPark has a new commitment to growth, but PetroTal has an impressive six year history of proven growth. GeoPark has a better allocation to share buybacks, but a worse allocation of returning capital to shareholders overall. The valuations aren’t too far apart when you account for debt and cash, and PetroTal will likely go to the debt markets within the next few years to get closer to their optimal capital structure, at least that’s what an MBA degree from an American university would tell them to do.

What is the upside potential for TAL.TO and GPRK? Over the next few years, the odds that we get a stretch with over $100 oil are pretty good. The odds that emerging markets rerate closer to historical multiples are decent as well, and the odds that energy returns to historical multiples as the world slowly shakes off ESG are also nonzero. For PetroTal especially, a 13% dividend yield, with production growing at 24% and share count falling by a few percentage points a year, the stock could easily trade down to an 8.5% dividend yield on a much larger dividend in a few years. TAL.TO could double in a couple of years, or do better over a longer time period. If GeoPark really does produce 100,000 barrels per day in 2030, that’s more than triple the current production in five years, all while paying an 8.75% dividend.

I don’t have any complaints about either company, but as I already have a position in EcoPetrol (EC), I will take Fabio’s advice and add a bit of PetroTal to the portfolio. Not a large amount, as I am already full up on RIG, ACDC, VET, FET, EC, and tiny 0.5% allocations to a handful of other names. But thanks again to Fabio at Capital Mindset for having me on his podcast, and thank you for turning me on to PetroTal.

Can we get a link to the podcast, please?

Link to podcast?