Revisiting Small Cap Tech Part II: ZipRecruiter $ZIP and Transact Technologies $TACT

One possible theme for 2026 is the revaluing of small software companies. Instead of just assuming that AI will displace all software, after three years, maybe the market will start to examine the ledger and see who is using AI to take market share, and who is fading away.

ZipRecruiter (ZIP):

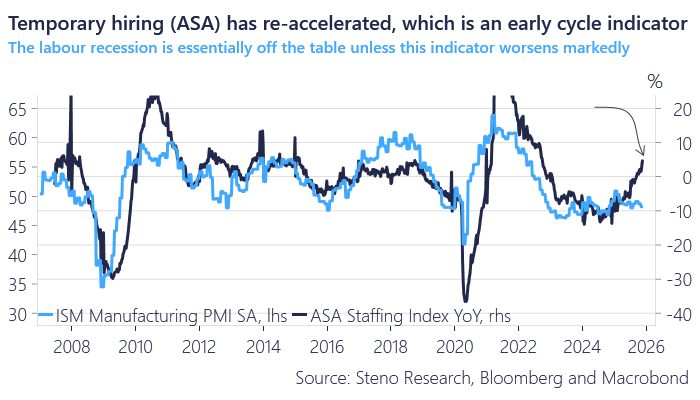

Before Trump’s Liberation Day, small business optimism and plans to hire were reaching new highs. But then uncertainty paralyzed growth plans. Their longer term capex plans still remain, however, even if they were on hold for 2025. The combination of interest rate cuts, tariff certainty, and 100% accelerated depreciation on qualifying equipment is quite an incentive to bring growth initiatives back to the front burner. There is already a pickup in temporary hiring, which typically precedes permanent hiring. Businesses need more manpower, but they want to see if business conditions really are stable.

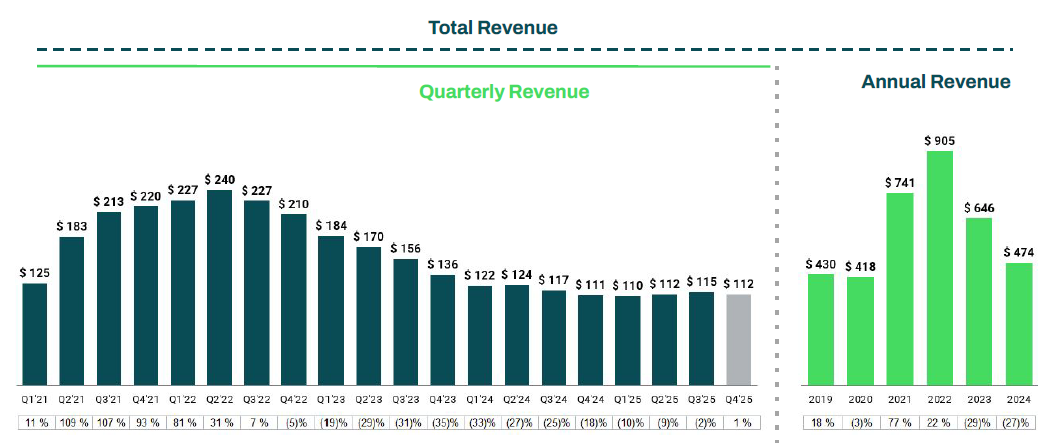

ZipRecruiter just had their first year over year volume increase since tech began their year of efficiency three years ago. You might have to squint to see it, but Q4 2025 revenue was $112 million compared to Q4 2024 revenue of $111 million. This is the first positive revenue comp in twelve quarters. This might be early, and maybe you can afford to keep ZIP on your watchlist for a while, but the market is forward looking.

ZipRecruiter is implementing AI, reasonably aggressively, this has allowed them to hold revenue steady while their competitor, the merged Monster and Career Builder entity, went through bankruptcy in July. Indeed and LinkedIn are still the 800 pound gorillas in the room, but ZipRecruiter seems to be carving out a niche for itself.

ZIP is a two-sided marketplace, they serve both the employer and employee. The employer uses AI to sort through resumes, and the employee uses AI to make their resume stand out to the employer. It might seem like a bit of an AI Rube Goldberg machine, but ZIP management maintains that this AI intermediation facilitates better employee matching. Those employers who stuck with ZipRecruiter during this downturn must like it, because what they are willing to pay for it has been growing over time.

ZipRecruiter just spoke at UBS’ Global Technology and AI conference, and while I would not be so bold as to claim that tech was within my circle of competence, there were a lot of positive developments. There are a number of new AI tools being rolled out for free with the priority of finding product market fit first, and only afterward does ZIP intend to use them to drive revenue. Given that the recruitment market is a $300 billion marketplace, and only 5% online, it makes sense to attempt to aggressively take market share first, and to figure out how to monetize it later.

Job Seeker traffic from large language model sources are up 140% quarter over quarter, which is up from 60% last quarter. The interface between LLMs and the job market is only just starting to accelerate. ZIP’s latest product is a kind of speed dating model, where an employer can post a job, and conduct a first round of introductory interviews of AI selected matches on the same day. Management claims that employers and employees are very happy with the rollout.

I am often early, and this could easily be one of those instances, but I am very bullish on ZipRecruiter. My original writeup can be found here:

Happy Labor Day! Manpower $MAN, HireQuest $HQI, and ZipRecruiter $ZIP

I remember when I was young and Labor Day was about having a day off from school and possibly even a barbeque. It was long before I learned about the Marxist paradigm of the bourgeoisie versus the proletariat. Even in today’s world where the typical employee with a 5% 401k match with compound interest will earn more as a capitalist than through their …

The Burning Question: Staffing, Kelly Services $KELYA vs. ZipRecruiter $ZIP

Introducing a collaboration between Value Don't Lie (VDL) and Unemployed Value Degen (UVD).

Transact Technologies (TACT):

I am less enthusiastic about Transact, half of their business is food labeling for convenience stores, but the other half is for casinos. With the rise of online betting markets, casinos are under enormous pressure. Occasionally an industry under pressure tries to spend their way out of the problem, and it is possible that TACT could be a beneficiary of casino pressure, but that is not an easy thesis.

But their quarterly results are impressive, casino and gaming sales are up 58% year over year, and total revenues were up 21% year over year. Last quarter GAAP net income was even positive, even if it was only $15,000. A stock price that was flat on a flip to GAAP net income breakeven, and a guidance raise on full year 2025 revenue, just goes to show how little the market thinks of small technology under the looming threat of AI. Management is guiding toward lower casino sales this upcoming quarter, again due to the headwinds of in-person gambling.

I like the interim CEO, but as an interim CEO, his tenure is temporary by definition. But since my original writeup, TACT has acquired two new non-casino clients, a convenience store chain and a national sushi franchise. With tech’s land and expand strategy, we won’t know how those accounts will grow over time. With the recent 2.5 million deportations and self deportations, businesses will be looking for labor saving technologies, and TACT promises labor saving.

I like quirky little companies, but I am out of my element in tech. I had started a small position in TACT, and I am reluctant to add more. I am also reluctant to sell a little business with 21% year over year growth and a major growth initiative coming from the scrappy CEO personally revamping the sales team’s sales process workflow. I’m not enthusiastic about their market position, but I am enthusiastic about their recent results. Every week that I deploy capital, TACT just doesn’t make the cut, but I also haven’t liquidated it either.

The original writeup can be found here:

Microcap growing revenue 19% year over year, growing gaming revenue 42% year over year, trading at 0.9x price to sales and with 40% net cash. (Paywalled)

The reason why I am digging into this particular microcap is that it is a part of the B. Riley Financial (RILY) constellation of companies, and I want to assess whether their shares in this company will likely be sold for a significant gain or not, and whether or not RILY’s investment decisions are sound. Two RILY investments I found to be incredible opportunities and are a part of my model portfolio, ALTG and BW. Some were outside of my circle of competence to judge, BEBE and SNCR. And DDI was another gambling stock, which while significantly undervalued, I avoided for my own portfolio.