New Fortress Energy (Reprise) $NFE

Someone asked me yesterday if there was a good writeup on New Fortress Energy (NFE), and so much had changed with the company since I had first written about them that I had to send them four different links with updates to my original article. NFE is sorely in need of a reprise.

From a bird’s eye view, natural gas is cheap in the US due to the gas that comes as a byproduct from fracking for shale oil. But natural gas is expensive, or even unavailable in many other places. Most of the Caribbean burns the most expensive hydrocarbon, diesel, for electricity. But natural gas needs a lot of infrastructure spending for liquefaction terminals, regasification terminals, storage tanks, and sometimes even the power plants. New Fortress Energy is trying to capture almost the whole damn value chain all by themselves; ambitious, and highly profitable, but watch out for that upfront capex.

The best example of how this business model would work is their oldest market, Jamaica. Today Jamaica has transitioned from 95% diesel electricity to 65% natural gas electricity. New Fortress Energy has about 15 years remaining on a contract to deliver 30 trillion British thermal units of natural gas annually, providing about 330 MW of power and natural gas to more than twenty industrial customers. It took five years from the start of construction at the Montego Bay terminal in 2015 until the completion of the Clarendon combined heat and power plant in 2020. Using some very rough estimates, because NFE is parsimonious with the details, the Jamaica market generates about $135 million of EBITDA annually, and that is contractually fixed for the next 15 years, with some room for volume growth as well.

The founder, CEO, and largest shareholder, Wes Edens, has a background in fixed income at Fortress Investment Group, and manages risk by fixing natural gas purchase orders and long term electricity power purchase agreements. By pairing the natural gas purchase contracts with the electricity delivery contracts, NFE typically has zero net exposure to natural gas prices. This means that the cash flows for NFE are known years in advance. This should be a highly desirable business that fetches huge multiples, but it has had its stumbles along the way. Also, since Fortress Investments is a private equity firm, New Fortress Energy does not have a culture of keeping shareholders well informed. One of the best presentations were for the bondholder’s viewing only, until they were released in an 8-K last October.

The Good:

New Fortress Energy has been growing aggressively, expanding from their original market in Jamaica to Puerto Rico, Nicaragua, and Brazil. The Nicaragua terminal was scheduled to come online last quarter, it is a 25 year contract, and should contribute an additional $175 million of EBITDA per year, and with room for volume growth as well. The Celba power plant in Brazil is coming online this summer, and that should generate an additional $225 million EBITDA annually as well. There is also a capacity auction in Southern Brazil this July, which should be an important catalyst, it could generate around $450 million annual EBITDA alone.

All combined, management is guiding toward $1 billion of EBITDA for full year 2025. I believe that this is a conservative estimate, and it does not include EBITDA from Jamaica which NFE plans to sell. EBITDA should grow to $1.3 billion for 2026, and $1.5 billion for 2027. By the time we get to 2028, management guided for over $1 billion EBITDA from Brazil alone.

Another huge catalyst is the recent election in Puerto Rico, where a Republican won for the first time in Puerto Rico’s history. The new Governor mentioned natural gas electricity in her victory speech on election night, and has since awarded NFE with a new contract to supply a power plant that Puerto Rico is building, but will generate an additional $100 million of EBITDA for 20 years, from 2028 to 2048. Most importantly is that this additional $100 million of EBITDA comes with no capex, as NFE already built a natural gas import terminal in San Juan.

But this is just the start of potential good news from Puerto Rico. There are four power plants capable of being converted from diesel to natural gas, two with negligible capex, and two with somewhat modest capex, but both conversion types could be done quickly. Also, Puerto Rico is interested in renegotiating their other supply contracts, as they have less than two years remaining, and both Puerto Rico and NFE prefer to have many years of certainty. It isn’t clear if the new contracts will be for ten years or fifteen, and what kind of margins NFE can capture, but we should be prepared for good news from Puerto Rico.

And the last recent positive catalyst, EBITDA was more than expected last quarter because NFE’s flagship liquefaction facility is running above nameplate capacity, and the excess production was sold in Europe for fat Dutch TTF natural gas prices. Since TTF is so high, and NFE likes to have zero exposure to natural gas prices, derivative hedges were used to lock in those prices for the excess capacity for 2025.

Again, piecing together disparate information from obscure investor presentations and press releases from New Fortress Energy, this extra capacity should be about 13 Tbtu, or 13 million mmbtu. That should correspond to around $100 million in EBITDA for 2025 just from the FLNG1 facility operating at above nameplate capacity.

The Bad:

So how did such an amazing business end up with a stock price can’t seem to catch a bid? Well, no good deed goes unpunished.

After two hurricanes destabilized the power grid of Puerto Rico, FEMA and the Army Corps of Engineers requested bids for a company to build two natural gas power plants in Puerto Rico. NFE rose to the occasion, and won the contract. But government contracts are very different from what NFE is accustomed to, and things have not worked out as well as they could have. Instead of a fifteen or twenty year gas supply agreement, the FEMA contract only came with a two or three year gas supply agreement. And while the payment from FEMA was scheduled to be paid to NFE over the entire period, the contract contained a clause that the Puerto Rican Power Authority, PREPA, could buy those power plants before the full contract term finished. PREPA exercised that clause, and bought the power plants from NFE.

The amount PREPA paid for the power plants was an amount pre-determined by the FEMA contract, but it did not include compensation for NFE for the work undertaken in order to build the power plants quickly and to stabilize Puerto Rico’s electric grid. One of the plants was built in 28 days! There is an ongoing reconciliation process for New Fortress Energy to be compensated for the rest of the FEMA contract, which NFE has estimated to be in the range of $500 million to $625 million. This is a an amount based on what NFE spent in order to fulfill the remaining years of the contract which was terminated early, as well as a standard profit.

New Fortress Energy has come under attack from short sellers, and if you have been following my write ups for Medical Properties Trust (MPW), I argue that one of the tactics of short sellers is to sow confusion and uncertainty. If you do a quick Twitter search, you will find posts arguing that NFE will not be paid the money owed to them by FEMA, but I don’t find these arguments to be credible. NFE management claims that FEMA is motivated to reconcile the contract, because the full liability if NFE sued FEMA for nonpayment would be over $1 billion, as FEMA would be obligated to pay for gas deliveries for the full contract length.

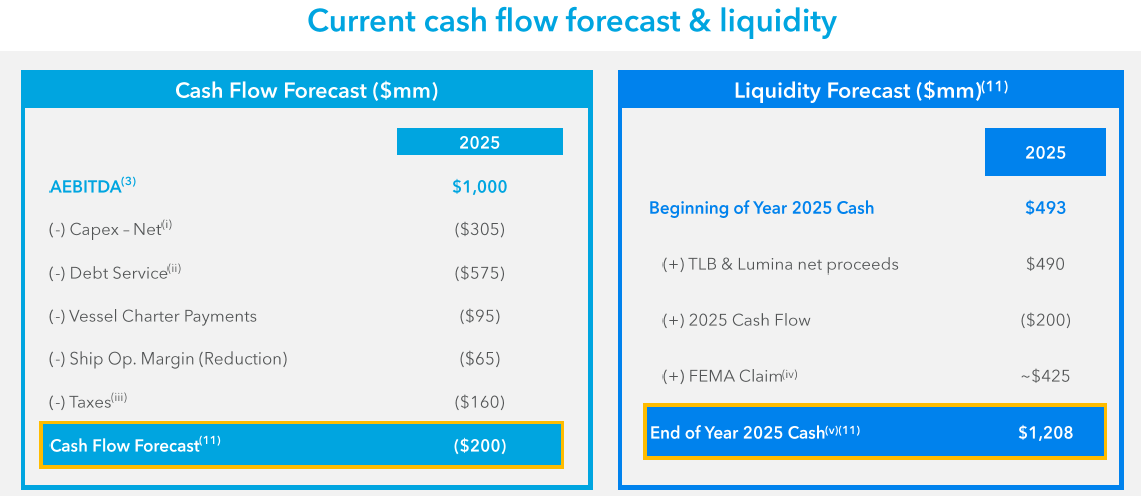

This FEMA contract reconciliation is important in the near term, because with interest expense and capex for 2025, NFE would only be free cash flow positive for the year if they received the FEMA settlement. In their most recent presentation, NFE management is guiding toward receiving those funds in 2025. Deutsche Bank just lowered their price target on NFE citing near term liquidity and cash flows. NFE just upsized a term loan, raising an additional $400 million, and they had $493 million at the end of last quarter. While it is true that management is guiding toward negative cash flow of $200 million, there is no imminent crisis. The real danger comes when the debt matures, and that is still a few years away.

The Puerto Rico FEMA contract caused another complication. GAAP accounting rules don’t have a way to log that $500 million expected FEMA settlement on the balance sheet, it isn’t a true receivable. This caused NFE to violate debt covenants relating to debt to assets ratios. It is a black mark on management that the CFO didn’t catch this beforehand, but with debt covenants violated, NFE had to refinance under duress. The bond holders extracted a pound of flesh, and a couple billion dollars of debt was extended and refinanced at 12%.

NFE management is guiding for some asset sales to de-lever. Jamaica is listed as a top priority for sale, as it is a mature market with limited growth potential. So how much is $135 million EBITDA a year for 15 years worth? At an 8% discount rate, that would be over $1 billion. Management is guiding toward $2 billion of asset sales, it isn’t clear which other assets would be sold in whole or in part. But with $2 billion less debt on the balance sheet, as well as the potential to refinance at least another $1 billion with an asset secured lease at low interest rates, NFE could enjoy a large multiple expansion. And, based on prior projections for 2025 EBITDA of $1.3 billion, it looks like the current projection of $1 billion of 2025 EBITDA is after the asset sales.

Conclusion:

With falling interest rates, NFE should be able to fetch some very respectable prices for their asset sales. Cutting $2 billion of debt, and lowering interest payments on another $1 billion, would dramatically change the market’s perception of NFE. We are likely to hear about new power plant conversions and corresponding gas supply contracts from Puerto Rico, as well as a renegotiation of the existing 80 Tbtu contract which expires in 2026. The FEMA money could come in at any time. And the power auction in Brazil this July should be very interesting. Once some positive catalysts start to roll in, the stock price should start responding.

New Fortress Energy has properly incentivized and competent leadership. Wes Edens has created value for shareholders before, and he owns about 20% of NFE, with inside purchases yesterday of 100,000 shares and the day before of 200,000 shares. And he has added value to shareholders before with FTAI Aviation (FTAI), which since January of 2022 has been a 5x return. That was a 7x until the recent value selloff these last three months.

I hate to put short term price targets, that is a method almost guaranteed to be wrong, but by the end of 2025, the market should be pricing in 2026 EBITDA with new Puerto Rico plant conversion income, and NFE could easily be trading north of $30 a share. By the end of 2026, when pricing in 2027 EBITDA and with more organic debt repayment, I would be surprised if the share price wasn’t closer to $50 a share. And by the end of 2028, EBITDA could easily be over $2 billion. I don’t consider a 5x over two years to be unreasonable given the fundamentals, and because Wes Edens just did the same thing for FTAI Aviation.

New Fortress Energy (NFE) $8.80: $30 by end of year 2025

New Fortress Energy (NFE) $8.80: $50 by end of year 2026

NFE needs better financing, I just hope the CFO and Wes will not commit any further unforced errors and that PREPA/FEMA pays soon. NFE wants to be financed like a utility, but currently pays 12+% for debt 🤯

Looks like everything depends on the likelihood and speed they can sell assets.