“Manure! I hate manure!” - Biff Tannon Part 2: LSB Industries $LXU

I forgot to update everyone on the January fitness challenge yesterday. Things are starting to heat up as I now owe you 14 pushups and 72 sit ups. Thank you all for taking the restacking more seriously. I am not as out of shape as I had thought I would be, but there is an unexpected challenge. My two-and-a-half year old thinks that pushups and sit ups are a great opportunity for an impromptu wrestling match, and proceeds to climb on me while I am fulfilling my end of the New Year’s resolution.

As a quick reminder, for the month of January, I will do 1 pushup for every restack and 1 sit up for every like that each writeup receives. If the combined number of likes and restacks reaches certain milestones, it will create a narrowing window of intermittent fasting.

I have been on the lookout for the right agricultural exposure, and it hasn’t been easy. Agriculture as a sector provides the possibility of an independent cycle, an opportunity for one investment to do well when others aren’t, instead of everything doing well or poorly together. The agricultural cycle is based on the weather, every few years there is a weather event that causes a crop failure in a staple crop, and when that occurs, average prices rise and farmers are rolling in cash. Outside of those years, bumper harvests are a famine for the farmers’ cashflows. It has been two years since the last staple crop price spike from the Ukraine war, and farmers are hurting, which means that agricultural stocks are cheap, but nature provides no visibility for when the next crop failure will drive up prices again.

Fertilizer in North America is especially interesting because the shale fracking revolution has made the primary input for fertilizer, natural gas, very cheap. Meanwhile, the primary competitor, Germany’s chemical industry, is in secular decline due to government mismanagement, banning fracking, and relying on intermittent power sources. A recent purchase of a fertilizer plant by the Koch family turned a lot of heads due to the high price paid.

I had previously written about CVR Partners (UAN), but there are problems with UAN. Carl Icahn is slowly buying the company, and as soon as his control hits 80%, he can buy out the rest at his convenience when regular volatility drives the price down. That and the limited partnership structure’s tax consequences have left me unhappy with UAN. I do own a few shares, but will probably be liquidating them shortly. The price is mostly flat since the writeup.

“Manure! I hate manure!” - Biff Tannon: CVR Partners $UAN, CVR Energy $CVI

Welcome back to the “Probably Not a Value Trap” series where I discuss businesses with a 10%+ dividend yield which I believe probably won’t get cut and why, but don’t come after me on Twitter if they do.

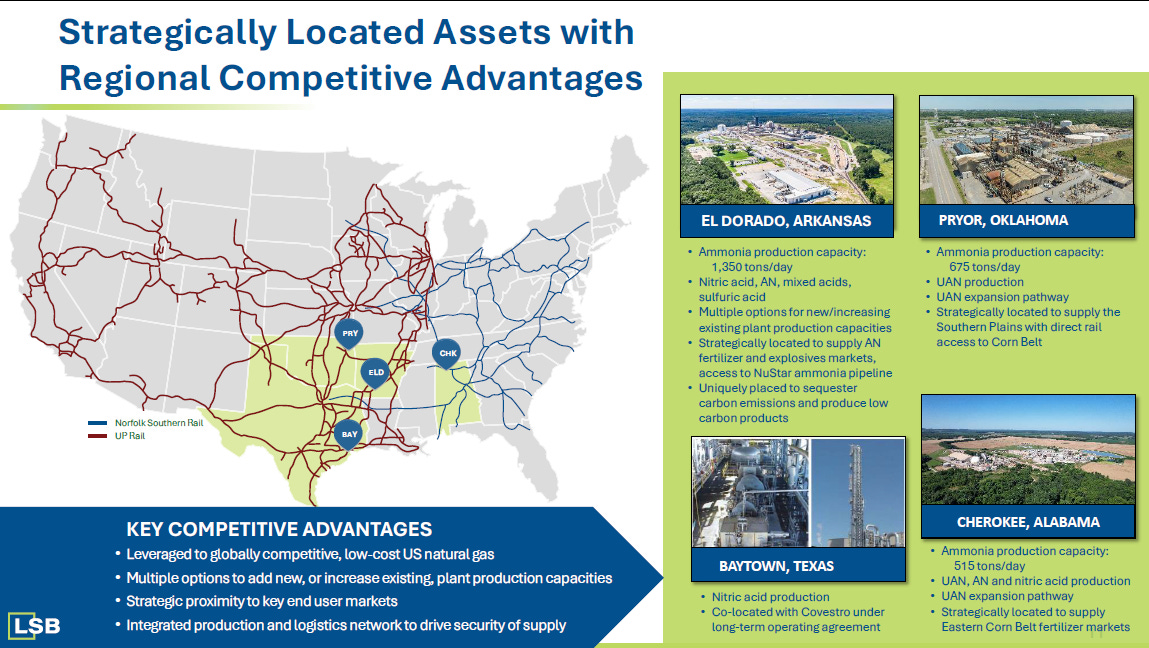

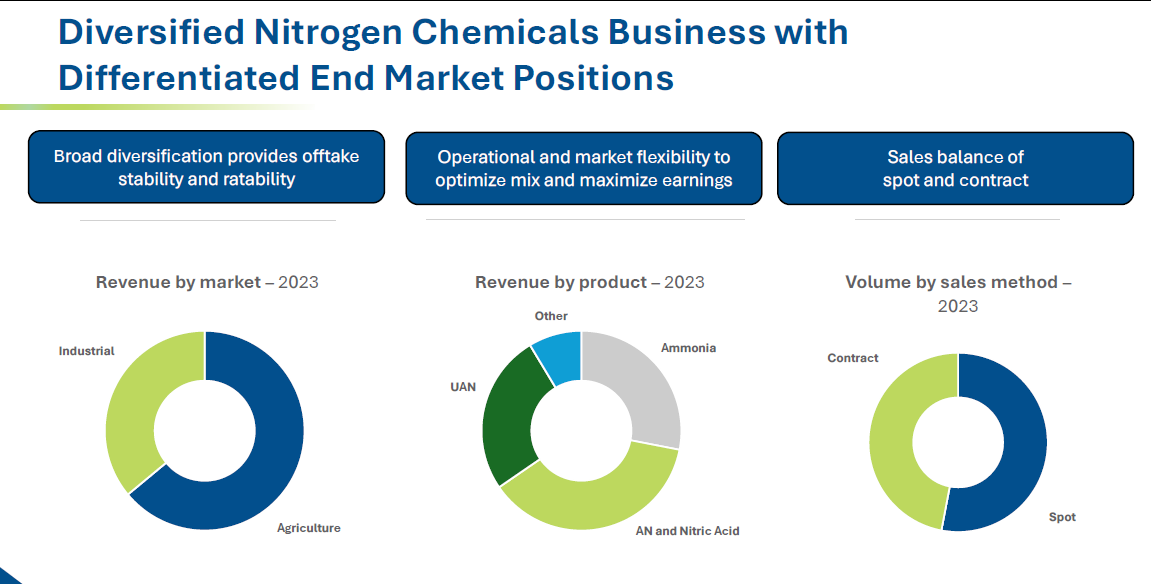

LSB Industries (LXU) is a small, North American nitrogen fertilizer manufacturer with three facilities. They produce ammonia, nitric acid, and ammonium nitrate. Their product mix is approximately 40% for industrial and mining applications, and 60% for agricultural applications. The agricultural products are sold almost entirely on the spot market, but the nitric acid for industrial and mining production are sold on fixed, gas-plus contracts with a three to seven year duration. Management is currently trying to upgrade facilities to try and pivot more toward the industrial products with their fixed contracts over the agricultural products that are sold on the spot market. Cruel irony, even when I find an agricultural company I like, they are in the process of pivoting away from agriculture.

Fertilizer is a cyclical commodity, and the last two years have been tough. Despite this tough time, LXU is generating about $100 million of operating cashflow, and their sustaining capex is approximately $60 to $80 million annually. However, due to the growth capex for their industrial pivot, trailing twelve month capex is closer to $100 million, so the company is mostly at breakeven for the moment. If you want to own LXU for the cyclicality, in 2022, peak EBITDA was $378 million, and this drove the market capitalization briefly over $2 billion. Today the market capitalization has fallen to $548 million.

Despite being at breakeven, from the bumper year in 2022, LXU still has $200 million of cash on the balance sheet, and has been retiring debt and buying back stock. Management is guiding toward another $100 million capex year in 2025, after which their pivot should be finished, and capex should fall again to the sustaining level. The pivot is being called “Pathway to $200 million” as it is management’s goal to get annual EBITDA up to $200 million at normal commodity prices, $500/ ton Tampa ammonia and $260/ton UAN.

Note that in the share count graph below, after the current CEO was hired in 2019 to revitalize the company, he negotiated the conversion of outstanding preferred stock into common. This caused an enormous dilution, but it is probably better in the long run to not have those dividend payments. Once LXU was able to return capital to shareholders, they bought back shares aggressively. Management might still buy some shares going forward, but they are currently focusing on the capex to realize their pathway to $200 million EBITDA.

The management team is about what you would expect from a fertilizer company. I wasn’t overwhelmed or underwhelmed, I was just whelmed. They were doing a decent enough job because they are supposed to, but not particularly enthusiastic about it. When the new CEO and CFO were brought in to turn the company around, they did their duty and bought a tiny bit of stock as a good faith gesture, but there isn’t enough insider buying to make me confident that incentives are really aligned.

The company is still 21% owned by the private equity firm which had originally held the preferred shares, Eldridge Industries. In the last two years, Eldridge has sold down their position from 60% ownership down to 21%. I don’t know whether or not Eldridge has plans to maintain control of LXU, or to continue selling down their position. This selling is almost certainly responsible for the stock’s downward momentum, and when Eldridge is finally finished selling, the stock would probably behave differently.

LXU starts their investor presentation with their poison pill, that is the first time I have ever seen a poison pill bragged about on page 1. This is to protect the value of their Net Operating Losses from being lost if they were to be acquired. LXU had negative net income from 2017 to 2021, and there are still $250 million in NOL’s left, which at a 25% tax rate would have a value of a little over $60 million. Once the NOL’s are completely worked through in a couple of years, management would no longer be justified in their poison pill, and at that time, LXU would become a likely acquisition target if they haven’t fixed their share price by then.

The pathway to $200 million EBITDA strategy has three components, the first is increasing maximum capacity from 800,000 tons of production to 875,000 tons. This capacity increase is due to efficiency gains and debottlenecking. The second component is upgrading facilities to produce higher value added products, less ammonia and more nitric acid and UAN. Two facilities have been upgraded in 2024, with the remaining to be finished in 2025, and this should result in about $55 million additional EBITDA. And the third component is a joint venture for carbon capture where the joint venture partner is spending all the capex, but then will pay LXU for their C02 offtake for about $15-$20 million annually. And of course, once LXU is back on sustaining capex only, that’s another $20 million saved. These should all be online for the 2026 year.

There are five ways to win with LSB Industries. First, at any time a crop failure could cause a spike in agricultural commodities, and LXU could suddenly earn $387 million in EBITDA instead of $100 million. Second, the pathway to $200 million EBITDA strategy should be finished in 2026, and at that time, absent multiple compression, doubling EBITDA should double the stock price. Third is share buybacks, at these low prices, LXU already bought back 20% of the float in two years. Fourth is a potential multiple rerating from the transformation away from a company that is reliant 60% on spot prices to one that is 70% based on multi-year gas-plus contracts for nitric acid. And fifth is the potential for falling interest rates to heat up the automobile and housing markets, as LXU’s products are used in polyurethane for automobiles, insulation, and aggregate for road construction. I know the sentiment now is all fear about rising interest rates, but I don’t suspect that will last for long. Trump has already announced he will bully other countries into buying our treasuries again, and he will be inaugurated in about a week and a half.

Trying to put a price target on LXU absent a commodity price spike, considering a 2027 with $200 million in EBITDA, only $70 million of sustaining capex, and 10% fewer shares from buybacks, would give a share price target of around $17. That could change if management engaged in an acquisition, which management has said is not off the table. It could also change if LXU is acquired after their NOL’s are used up and they drop their poison pill. If the stock price really is suppressed by Eldridge Industries’ selling, then $17 could be a low estimate.

LSB Industries (LXU) $7.66: $17 by end of year 2026

Bob Robotti has an ownership of 6% as well. Low US Nat Gas prices isthe huge competitive advantage this investment thesis is based on. Could also be a potential risk in the medium future imo.

I have a small piece left. Made some money, lost some money. In cyclicals I usually overstay and regretfully pay for it.

Management made some blunders with natural gas purcases, their ideas of M&A,...

Would prefer UAN, which is much more profitable, but as MLP is a no go for me (foreigner).