In July of 2024 I wrote about LifeMD (LFMD), the telehealth competitor to Hims & Hers (HIMS). Since I wrote about LFMD, the price went from $6 to $15 and back to $6. I was not tracking it closely, and I was not nimble. But it looks like LFMD is a better value at $6 today than it was at $6 fourteen months ago.

LFMD had very strong insider buying under $5, and very strong insider selling over $7. At this current price around $6, no insiders have stepped up yet to buy again. This could indicate that management doubts the growth trajectory, or they are waiting for a cheaper entry price. There might be time to wait and keep LFMD on a watchlist, or not, the market is moving pretty fast these days.

My original writeup can be found here:

My stock has fallen, and it can’t get up: LifeMD $LFMD, Medifast $MED

I have to sometimes remind myself that inside jokes and memes from thirty years ago might fall flat to a different generation or an international audience. Allow me to introduce you to Mrs. Fletcher, the star of an iconic television commercial from the 1980s.

Is it smart to invest in a HIMS competitor, after all, isn’t technology winner take all? Companies like Uber have a network effect, drivers want to drive for the app with the most customers, and customers want to use the app with the most drivers. It creates a self-reinforcing feedback loop pushing out most competition. If it isn’t winner-take-all, then it’s usually winner-take-most.

But not every technology is a network. Is there any benefit to using the same bank as your friends? I don’t think so. Companies like SoFi are growing aggressively because Millennials don’t want to go into a physical bank branch, and legacy banks have been terrible about updating their technology. But banking isn’t a network.

Is there any benefit to using the same app as your friends to buy your viagra, finasteride, and semaglutide? It isn’t like a taxi, it doesn’t matter if the prescribing doctor is five miles away or five hundred miles away. The only advantage that HIMS has over LFMD would be traditional things like economies of scale for advertising and to fund more research and development. But it doesn’t seem to necessarily be a winner-take-all kind of market.

LifeMD has been struggling for the last six to nine months with their growth trajectory suddenly flat lining. In their rollout of semaglutide, they went with the branded Wegovy, meanwhile, over a hundred competitors went with a generic compound version. Why use LFMD for $500 a month, when their competitors are $150 a month?

For one thing, Novo Nordisk has filed 132 lawsuits against those generic compound versions. The law isn’t entirely clear, it is allowable to prescribe a generic version of a patented drug if the patient needs that drug to be blended with another. But it seems obvious that what the patients really wanted was a $150 drug instead of a $500 drug. So far courts have issued 44 permanent injunctions against these generic compounders, but it’s a bit of a game of whack-a-mole, and LFMD management says that the legal actions have not had an effect in removing the cheaper alternative from the marketplace yet.

So LifeMD isn’t taking market share, but at least they aren’t getting sued. HIMS is large enough to play it both ways, offering branded Wegovy and compounded generics, and Novo Nordisk isn’t suing them, so there appears to be some benefits to size.

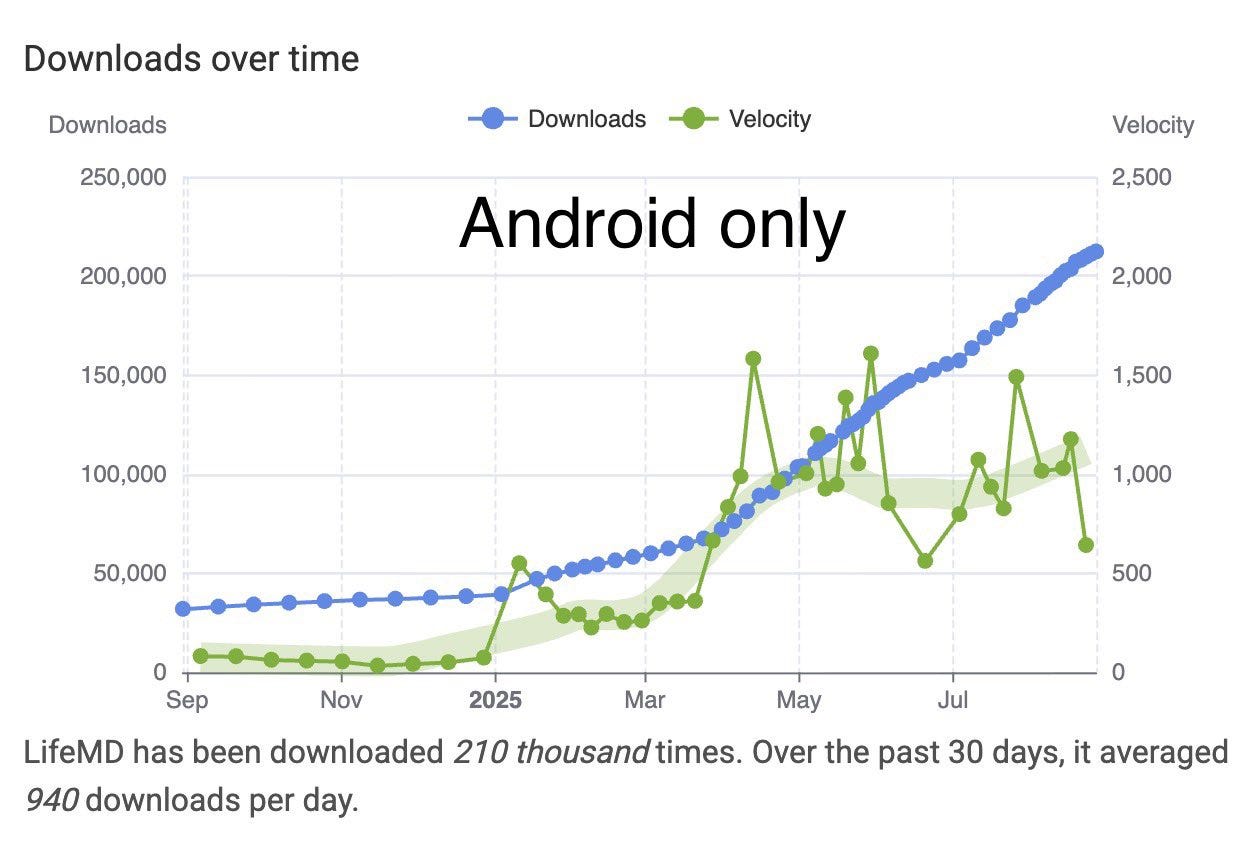

But this is just the beginning of the Semaglutide story, in April LifeMD announced that they can now accept Medicare for certain treatments which covers 21 million Americans in 26 states. And after Medicare adoption, insurance coverage typically follows quickly. I don’t have all the details regarding whether or not this will lead to more market penetration immediately, but I do have the data on recent LFMD app downloads.

To me it looks like the LifeMD app has gone from being downloaded 400 times a day to 900 times a day since the April announcement of Medicare compatibility. This hasn’t shown up in revenue yet, however, and it isn’t obvious why. Are people downloading and not buying?

The last earnings call for the quarter ending June 30th 2025, which is a full 60 days after the spike in app downloads, showed flat revenue quarter over quarter. And management guided for things to be flat for the remainder of 2025. Allegedly Medicare pays over 80% of claims within 14 - 30 calendar days, which is not what I have heard from hospital operators, but they likely have more complicated scenarios. Also, LFMD didn't have a large increase in accounts receivable last quarter, so it doesn’t appear that these downloads are for Medicare users for which LFMD hasn’t been reimbursed yet. There might be a timing issue of which I am unaware, but management is still guiding for next quarter to be flat.

With 21 million Americans having access to $0 out of pocket expense for obesity behavioral therapy if their BMI is over 30, will this start to show up in LifeMD’s revenues next quarter, even though management didn’t guide for any improvements on their last earnings call on August 5th? The app download rate has more than doubled, I have a hard time believing that means nothing. Since the end of June, Android downloads have gone from 140,000 to 210,000.

Management did discuss the urgency of providing users with instant insurance verification so that customers can immediately know which treatments will be covered. This should be rolled out before the end of 2025, and it could be responsible for the lack of revenue growth despite the download growth.

In the last 12 months since I wrote about LifeMD, revenue per share has gone from $4.79 to $5.67. That’s an 18% growth rate for a company that only had the $500 branded Wegovy option. Management is guiding toward the end of 2025 having all of their weightloss customers covered by Medicare, insurance, or be on a cheaper version of semaglutide, perhaps copying HIMS with both branded and compound version, but still not getting sued because at least Novo Nordisk is making some money.

I think LifeMD might be a gem that’s been thrown out in the trash with the overall selloff in Healthcare stocks. The only thing that the market hates as much as Healthcare right now is Energy.

My original thesis was that the Medifast partnership would stuff LifeMD full of volume. Even if Medifast eventually did go out of business, at least in the meantime there would be tens of thousands of multi-level marketers signing people up for LifeMD. Management has noticed an increase in their weightloss customers using the LFMD app for other medical needs. Some of the Medifast customers, once accustomed to the app, are using it for their recurring cardiovascular prescriptions, hormone therapy, sexual health, etc.

This is still a company that is growing telehealth revenue at over a 20% rate, despite the fact that they were strategically poorly positioned for the semaglutide market for the last six months.

I believe that once the wrinkles are ironed out regarding insurance coverage, Medicare customers, and the cheaper oral option of compound semaglutide, there is a very good chance that LifeMD returns to growth. As a growth company, they could fetch a growth multiple. The stock reached $15 just a few months ago, a price to sales ratio of 5.0x. Today it sits at 1.2x.

A return to 20% growth and a 5.0x price to sales multiple would send LFMD’s stock price from $6.19 to $40 by the end of 2027. A more moderate price target would be half of that. They just became debt free, and with control over advertising spending, they are in a great financial position. As the market gets certainty on semaglutide, LFMD has a very good chance of returning to their growth trajectory. And as an added bonus, they just added mental health capabilities to compete directly with Talkspace (TALK) as well as menopause treatment capabilities.

LifeMD (LFMD) $6.19: $20 to $40 by the end of 2027