Guerrillas for President and Cocaine Hippopotamuses: Ecopetrol $EC

Pablo Escobar’s Legacy - Probably Not a Value Trap

My dominant thesis still remains sustained inflation, commodity supercycle, revenge of the old economy, etc. ; there are many names for the same theme. For twenty years we have underinvested in resource extraction and commodity prices will catch up at some point. I have my doubts whether or not that will happen in 2025, but already Gold is leading the pack due to demand from central banks for a reserve asset in a world without trust. According to JP Morgan, Gold now accounts for 15% of global central bank reserve assets.

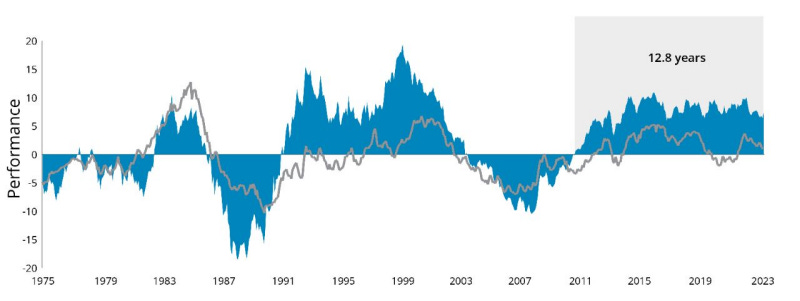

Also, you may be aware of my consistent home country bias, the vast majority of write ups are US domiciled public companies. One possible theme for the medium term future is a reversal of the last 12 years of US stock market outperformance against International stock markets. Is now the moment for the trend below to reverse? It could be.

S&P 500 Minus MSCI World

The US stock market has been the beneficiary of foreign capital inflows. Investors from around the world are taking their hard earned savings and buying NVIDIA, Apple, Microsoft, etc. A big threat to US stock market outperformance would be if those foreign buyers of US stocks took their money back to invest elsewhere. And this would typically happen if benchmark rates were lower in the US relative to other countries. High interest rates in the US are connected to capital inflows which are connected to a strong dollar.

Net foreign acquisitions of US securities.

So how cheap do foreign investments have to get before investors take their money and go home? The S&P 500 at a price to earnings ratio of 26.32 is 4.62 standard deviations above its 20 year average. Spain, Austria, Poland, Japan, Chile, and Mexico are all more than one standard deviation below their 20 year average price to earnings ratio. The cheapest country on a relative basis currently is Colombia with a price to earnings ratio 2.48 standard deviations below the 20 year average, and Ecopetrol (EC) is trading at an eight year low. At its current dividend yield, as long as it isn’t nationalized beforehand, shareholders would break even from dividends within four years.

Ecopetrol is the state controlled oil company of Colombia and produces about 750,000 barrels of oil equivalent per day. As I write this, futures markets for oil are down 5%, and there are good odds that Ecopetrol’s stock price will be down at the open tomorrow. I’m not smart enough to call the bottom in oil, but I think I am smart enough to call that oil is cheap when the marginal barrel of shale oil is almost at breakeven prices.

Colombia has jurisdictional risk, it has been a somewhat failed narco state for as long as anyone can remember. But crime rates have fallen and gdp per capita, especially in purchasing power parity terms, have been improving since the 1990s. Their current president, Gustavo Petro Urrego, a former guerrilla fighter, is the first progressive president in Colombia’s history, but he seems to be having a difficult time in enacting his platform. Now with less than two years remaining in his term, if he hasn’t tried to loot the national oil company, it seems increasingly likely that he is either unable to execute it, or unwilling to kill the golden goose after watching the economic destruction of Venezuela. With the electorate disappointed in his accomplishments in office, many talking heads are predicting a return to a more centrist politician in 2026, but this is far outside of my expertise.

Ecopetrol reached its peak stock price of $64.70 in April of 2012, and since that time has paid out $20.50 in dividends, and now sits at a price of $8.10. Share count is unchanged over that time, revenue is 5x larger, and net income is about 3x larger. There are capital allocation problems, EC has been on an acquisition spree, diversifying into electricity transmission, toll roads, telecom, etc., all industries which typically fetch a high multiple, but not in Colombia, and not with a conglomerate discount. Ecopetrol also has relatively few proven reserves, but for the last three years, has been proving more reserves than it depletes, but at a large capex expense. So the dividends paid out by Ecopetrol are the scraps from the table, but the price is so cheap, that those scraps are probably a $1 to $1.20 dividend payment for 2025, which puts it well over the 10% threshold for the “Probably Not a Value Trap” series.

The good part of Ecopetrol is that they are still drilling cheap surface oil with a low lifting costs; I’ve seen estimates of costs between $8 and $10 per barrel. This gives them a 40% to 45% EBITDA margin, but of course most of that money is spent on capex and acquisitions which leaves a 14% net margin, down from a peak of 30%. Another good aspect of Ecopetrol is the corporate culture in South America doesn’t have much dilution from executive compensation, there are no share buybacks, but a flat share count is better than a diluting one. Maybe the best aspect of South American corporate culture is to keep enough cash to weather some volatility, EC has over $4 billion in the warchest to cover near term debt maturities and for a rainy day.

Even though the capital allocation is poor, many of those acquisitions will come to bear fruit and drive future growth. Ecopetrol has four jackup rigs in the Gulf of Mexico near Texas, and a joint venture with Occidental Petroleum in the Permian basin near Midland. Ecopetrol USA is already up to about 80,000 barrels of oil equivalent per day.

Ecopetrol also has about $27 billion of debt, most of it USD denominated. But 2023 EBITDA was over 6x interest expense, which is a reasonably comfortable amount of leverage. Debt maturities within the next two years are at about $2.4 billion, and EC has a credit rating of BB+, so they can access US debt markets with relative ease.

Ecopetrol has jurisdictional risk, but Ecopetrol is 88% owned by the Colombian government. And the government relies on that dividend income as much as any shareholder, those dividends are between 1.5% and 2% of Colombian government receipts. I believe the jurisdictional risk is wildly overstated, and the government wouldn’t kill their golden goose, or even jeopardize its access to US debt markets. If it is true that the marginal cost of shale oil is going to provide a price floor on the commodity due to supply destruction, then Ecopetrol could be one of the more safe high yield income stocks.

With a reasonable likelihood for regime change in 2026, Ecopetrol could enjoy a sizable multiple rerating. EC typically finds itself trading at a price to earnings ratio of between four and eight. A return to an eight price to earnings, combined with the oil prices of 2022, would put the share price of Ecopetrol at around $28. Or, if EC runs out of handy acquisition targets and pays out a larger dividend, in the last twelve years the annual dividend was over $3 twice, and over $2 three other times.

If a centrist or conservative government after 2026 reallocated capital away from green projects and toward growth or return of capital to shareholders, the pass through from EBITDA to Net Income could easily double, or a higher growth rate could get priced into the stock. Either of those paths could bring the stock back to the 2012 peak of $64.70. On a price to sales metric, Ecopetrol would need to 10x to return to past multiples.

In my pursuit of businesses outside of my home country bias, it is not my intention to focus on emerging markets or commodities. I will be searching for undervalued businesses in developed markets and in other sectors. But I think the odds are strong that Ecopetrol is mispriced, and especially if the price drops below $8 a share on Monday’s trading, I am tempted to start a position.

Great minds think alike, I already own EC at 9.15 share but I'm buying more as it drops.

very interesting professor!

vaguely related to the commodities supercycle, how able a mining, logistics, and ports business in australia with no jurisdiction risk and is expanding production 3x: https://twitter.com/Fenix_Resources