Buying $1 of Land for $0.70, Hopefully Selling it for $1.40: Forestar Group $FOR

Maybe I’m feeling a bit brutalized by the market recently, but sometimes I have to reach out for some comfort and go back to the basics. One of my short term investing ideas is falling interest rates, and one of my long term investing ideas is sustained inflation. Cheap real estate developers with large land banks should benefit from both.

Forestar Group (FOR) is a real estate developer, but with an extra step forward in the division of labor and specialization. Forestar only does the lot development, they don’t build the houses. A different developer will identify the land to buy, but then Forestar will buy the land, take the risk of getting it re-permitted, create a master plan in conjunction with that other large developer (mostly DR Horton (DHI)), and Forestar will subdivide the property and perform the site development. The other real estate developers get to be more capital light, meanwhile Forestar, gets to be a boring and predictable land bank, with an inventory that gets more valuable over time. The developed lot represents around 20% to 30% of the final home cost, and last quarter Forestar sold their lots at an average price of $105,500.

I am not as interested in this modern trend of companies trying to be capital light. As a value investor, I am happy to buy capital-intensive businesses if the capital is underpriced. And especially if the assets appreciate rather than depreciate. Forestar is currently selling at $0.70 to book value, and their book value is all land, no goodwill or intangibles. Just through regular cyclicality, every few years or so, Forestar trades up to about 1.4x price to book value. And their book value per share has compounded at 16.2% annually for the last five years since management made growth their policy.

From start to finish, from the time Forestar acquires a parcel of land until the time that the last lot is sold in a large development, it can take twelve years, but Forestar usually has a return of initial risk capital within three years. With land prices appreciating at an average rate of 3% to 5%, and with the potential for sustained inflation to increase the rate of land price appreciation, Forestar’s $2.7 billion of investment properties are a compounding snowball. Their modest long term debt carries an average rate of 4.6%, which is much lower than the rates that banks would charge for a typical land development loan.

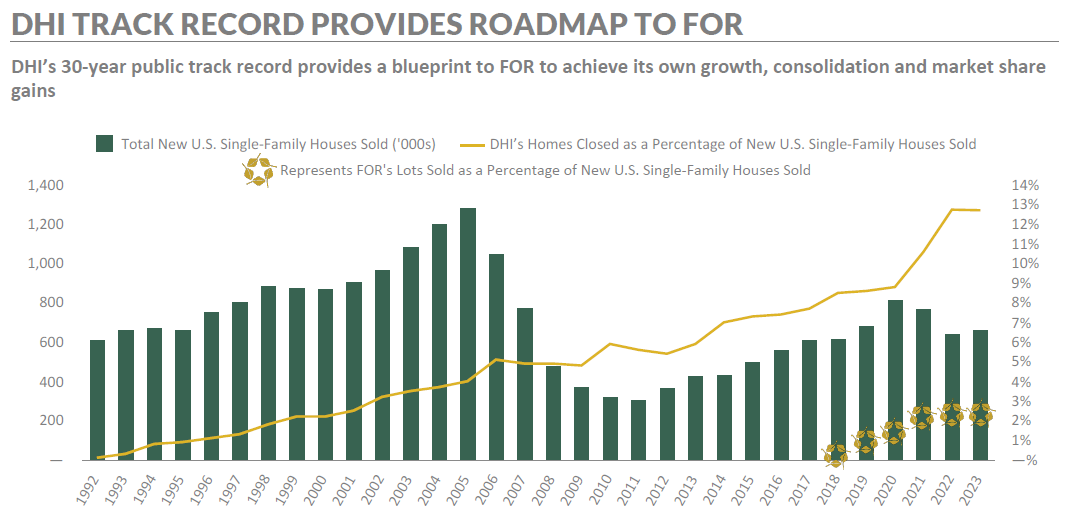

The biggest risk is that Forestar has the majority of their sales with one large client, DR Horton. However, DR Horton has a master supply and shared services agreement with Forestar, as well as owns 62% of Forestar stock. DR Horton has a right of first offer for any lots on land that is sourced by DHI, but not for land that is sourced by another developer. Forestar isn’t captive to DR Horton, Forestar is constantly trying to develop relationships with new clients, and to expand the business model of third party lot development. But with approximately 2/3rds of sales to a single customer, the risk remains that if DR Horton struggles, it could impact Forestar’s business. Within DHI, there is still plenty of room for Forestar to grow. Today 15% of DHI homes are built on Forestar lots, with the goal of reaching 33%.

DR Horton has grown to be over 12% of all single family homes sold in the US last year. Meanwhile 2.3% of all single family homes sold in the US are built on Forestar’s lots. Forestar has the goal of reaching a 5% national market share, or double from where they are today, not including the potential for some sort of a rebound in single family home construction back to the levels seen in the 1990s. Until Forestar reaches their market share goal, profits are plowed back into the land bank, they don’t pay a dividend or do share buybacks. And it is not certain how DR Horton will monetize their 62% ownership stake, however it is very likely that they will monetize it eventually.

Based on current growth trajectories, Forestar will reach their market share goal by about 2030, in about five years. At that time, book value per share will likely be around $65 from $31 today. While the stock price could be depressed by DHI selling, it could also trade back up to a historical 1.4x price to book. Once market share goals are reached, it isn’t clear how Forestar would return capital to shareholders, or if capital allocation policy could cause multiple expansion beyond prior peaks. But it is very possible that Forestar’s stock will trade up to around $91 a share by the end of this decade.

There are too many unknowns to consider Forestar to be a buy and hold forever stock. A lot would depend on how DHI chooses to monetize their shares, and what sort of capital allocation policy Forestar chooses after they reach their market share goal. In the meanwhile, I would sell any time that the price to book ratio reaches past cyclical highs of 1.4x, and look to re-enter any time the price to book ratio falls below 0.7x.

Forestar Group (FOR) $22.21: $91 by the end of 2030

If their average lot life is 12 years, then how do they earn back their cash equity (or stepped-up land basis contribution) after only 3 years?

Sounds similar to $MRP no?