2024 Q4 Earnings Update Part I: $COUR, $BZH, $HTLD, $NWL, Paywalled $LEU

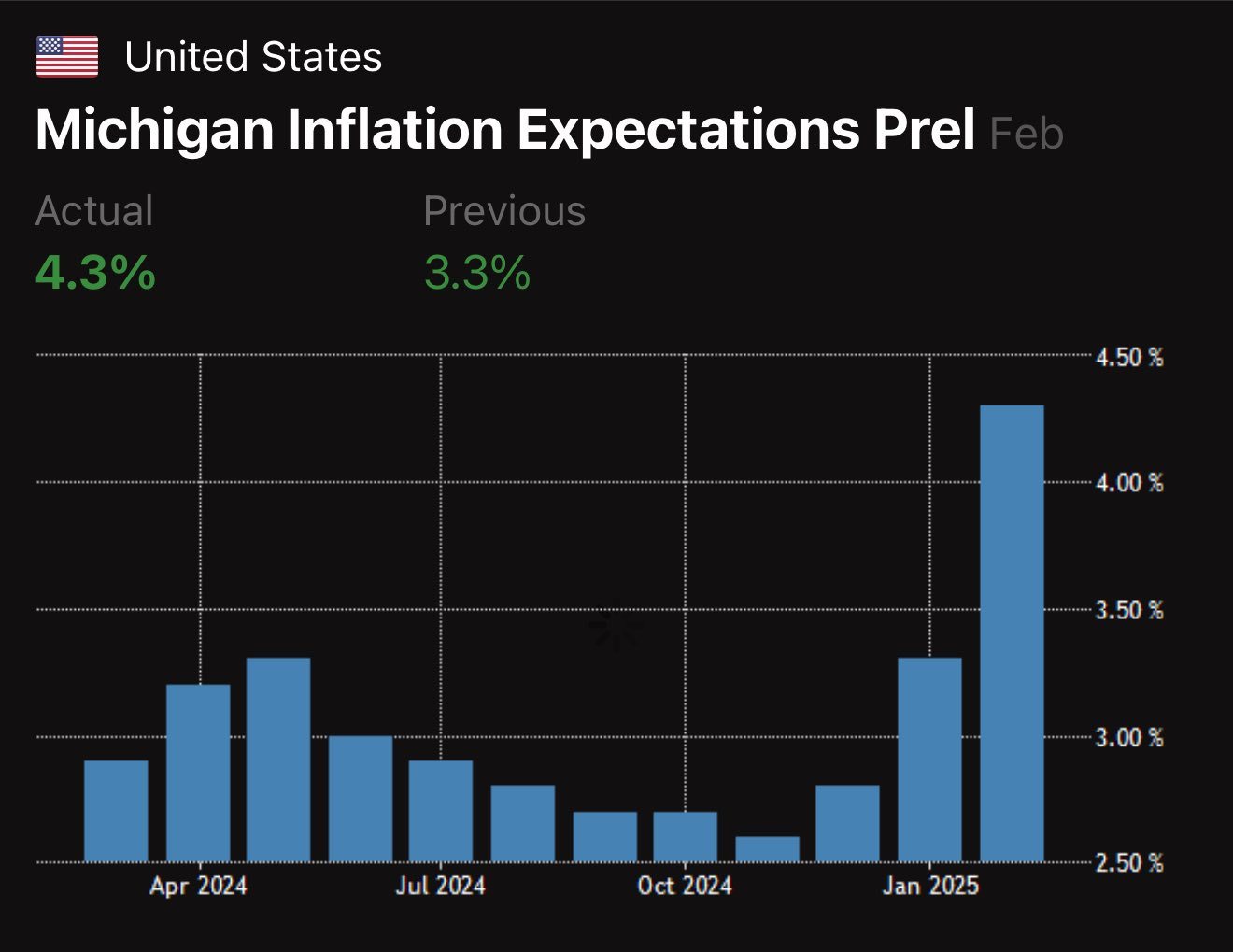

For the last two weeks, we have had a Monday surprise, first DeepSeek, and then friendly neighborhood tariffs. This week we even had a Friday surprise, survey results showed that inflation expectations had risen to 4.3%!

Within this data was the surprise result that Republicans expected 0% inflation, Democrats expected 7.2% inflation, and the survey oversampled Democrats. Why do Democrats expect 7.2% inflation? Because that’s what their news sources told them would be the result of Trump’s tariffs, because Orange Man Bad. This is despite the fact that he implemented tariffs in his first term, and they did not lead to a huge inflation spike.

But, the narrative that inflation expectations had become unanchored, and thus the Federal Reserve might have to raise interest rates, spooked the market. Futures have about a 25% chance of a rate hike in 2025 priced in. As CPI data is released, there is enormous potential for this fear to be unwound, and for the market to climb higher. Truflation is even showing some relative inflation relief for the moment.

I am predicting higher sustained inflation, and I believe that it will come in waves, but I believe the next wave will be due to looser banking regulations and lower interest rates allowing people to tap into their home equity. I do not predict that the next inflation wave is imminently upon us in 2025 due to tariff policy. But I have been wrong before.

Coursera (COUR):

Coursera’s earnings call was nothing special, modest growth among their three segments, 5% to 14%, and a small positive adjusted EBITDA, but a negative GAAP net income. The 14% year over year growth was from a segment with 100% margins, tuition share from universities who are desperate to implement an online strategy, and simply plug into Coursera because that is the easiest solution. With a bit more growth, Coursera could outpace the scourge of tech stocks, stock based compensation. Not only is AI not killing Coursera, but AI micro-credentials are being rolled out for entry-level job certifications. I don’t know how many quarters it will take, but on the inflection to GAAP net income, Coursera could enjoy a huge rerating.

Coursera has a new CEO, Greg Hart, who started in February of 2025. Greg comes from 23 years at Amazon, so I would predict that the odds of Coursera increasing their growth and innovation trajectory just went up. There is no reason given why the former CEO of seven years, Jeff Maggioncalda, retired suddenly, but the co-founder and chairman of the board, Andrew Ng remains. Executive search takes a long time, usually two years for a CEO, this leads me to believe that the process of replacing Jeff started a while ago, and the reason for the replacement was not due to some egregious scandal or a falling out, just that Jeff underperformed, and Greg was handpicked to increase performance. Compare this to the situation at Kohl’s when the previous CEO was lured away, and an interim CEO mishandled the company for two years during the search process. Exceptional people are few and far between, and I am cautiously optimistic about Coursera’s future under Greg Hart.

I have a small position as one of many small cap tech stocks, but at the moment, both Teladoc and Nerdy are outperforming Coursera. Tech is one of those areas where I don’t have confidence in which company will outperform, so I diversify. I did not put a price target on Coursera when I first wrote about it, but an efficient tech CEO should be able to get the company into the “Rule of 40” club where growth and margins add up to over 40, and the price to sales multiple is greater than 4.0x.

Coursera (COUR) $8.04: $17.68 by end of year 2026

Disrupting Higher Ed: Coursera $COUR

A quick note before I dive in. I am starting to believe that the theme of the weakening dollar and the reversal of fund flows back into emerging markets and commodities might be more than a year away. I am still holding my starter positions in Ecopterol (EC) and PagSeguro (PAGS), and I will even add to them, but I do not expect them to rally significa…

Beazer Homes (BZH):

Beazer Homes reminds me of a Little Ceasar’s Pizza meme:

Beazer Homes: It’s cheap and it’s ready.

Me: Is it good?

Beazer Homes: It’s CHEAP. And it’s READY.

This $684 million market capitalization home builder has $2.1 billion of inventory, much of which is land purchased at lower prices and understates the current value. They also have $1 billion of long term debt, which to me is not a problem as I am counting on inflation to whittle the real value of that debt down. Management isn’t great, their focus has been on growing tangible book by 19% a year on average, but the market wants growth not value. BZH has pivoted toward growth, but the sudden shift to aggressive capex in the short term is hurting earnings. When BZH hits their 200 community target by the end of 2026, growth capex could slow dramatically and earnings would improve, but growth will collapse. A seasoned management team would have been targeting sustainable growth all along to avoid this start stop whiplash. I’m not trying to criticize management too harshly, there’s nothing wrong with Little Caesar’s Pizza, but this would not go into a quality portfolio.

BZH stock sold off hard on the last earnings call, down from $27.50 to $21.00 a share, but it has since bounced back to around $22 a share. For that $22, you get $39.50 per share of tangible book value, and land is one of the key categories I want exposure to for the sustained inflation thesis. Last quarter BZH earned $0.10 a share, and next quarter they are guiding toward $0.30 a share. But earnings aren’t the reason that I am interested. Christmas is a weak season for home sales, and management claims that BZH did not chase discounts as aggressively as their competitors, choosing instead to preserve asset values. Management also says that January has been an improvement, despite the higher rate environment. Plus, interest rates seem to be on the decline, making this likely a good entry point. Where else can you get land at a half off sale?

On a relatively medium term rerating, BZH could double and get back to 1.00x price to tangible book. That could be achieved by falling rates, or it could be achieved by hitting their 2026 goal of 200 active developments, slowing down on growth, and having a bit better profitability due to lower growth capex.

Beazer Homes (BZH) $21.95: $43.51 by end of year 2026

Why Homebuilders like Beazer Homes $BZH and Landsea Homes $LSEA are a part of my Oil, Gold, and Land inflation protection strategy.

During the last period of sustained inflation, gold, oil, and land outperformed almost every asset class. Congress is running a deficit of 7% of GDP and we are reshoring industries with the rise of tariff retaliation and rivalry with China. So I believe sustained inflation is a safe prediction, but it’s always important to ask what could make things g…

Heartland Express (HTLD):

Heartland Express had positive operating income for the last quarter, a sequential improvement, but still not GAAP net income. Management attributes this to two things, better integration of the recent acquisitions, and an improving market, which corresponds to my thesis that the end of the great destocking cycle is finally upon us. HTLD engaged in two acquisitions during this two year bear market, and has already paid down $295 million of debt in the last two years, $100 million in the last 12 months. I don’t hate debt, if it has a low interest rate, I prefer some leverage to benefit from sustained inflation. But the management of HTLD hates debt, and is on a journey to be debt free again. In a cyclical business, this positions HTLD to be the company that survives and makes acquisitions in the downturn, as they have done. I don’t know how many quarters of sequential improvement it will take for the market to notice HTLD, but the process has begun. I might be early, but it looks like HTLD is an eventual three to four bagger from here, as logistics companies routinely trade at 2.5x to 3.0x price to sales. At the current pace of debt paydown, they will be debt free and returning to share buybacks within two years.

Heartland Express (HTLD) $12.17: $38.24 by end of year 2026

Picking my spots for the End of Destocking: Heartland Express $HTLD

Hello and Welcome to another small cap value idea. For those of you who have been following for a while, my largest logistics holding, Forward Air (FWRD), has been pressured by activist investors to go private and I will not be able to enjoy the stock returning to full value. While still a double from the price when I first wrote about it, it easily c…

Newell Brands (NWL):

Wow did the market hate this earnings report! The stock price crashed from around $10 to a bit over $7. Newell brands is on quarter 6 of sequential improvement from a well thought out turnaround strategy. But, they guided toward worse results next quarter, which is in line with their typical seasonality. Some brands are strong for back to school, some are strong for Christmas, but next quarter is always seasonally the weakest. It looks like the algorithms this week were programmed to sell off anything that guided lower, shoot first, ask questions never. Newell Brands is still well on its way back to being a $25 stock, but now you can buy it around $7 instead of around $10.

I do think the market is waiting to see revenue growth, not just cost cutting and margin expansion. Management is guiding for a return to revenue growth in 2025, this year! Until then, the company is still GAAP net income profitable and paying a tiny dividend while you wait. I was shocked by the market response on a quarter with an earnings beat, sometimes earnings reports on the wrong day, and having that 4.3% inflation expectations report really spooked the market.

Management updated investors on their supply chain reshoring efforts, and NWL has very little exposure to China, except for within the baby segments. There is somewhat more exposure to Mexico, but NWL has excess capacity in their US factories, and can continue to reshore production without large capex spending.

When Newell Brands was priced for growth, it enjoyed a 1.40x price to sales multiple. But even in more moderate times, still traded at a 1.0x price to sales multiple. Today it sits at 0.39x. New management came into a bad situation, proposed a highly credible turnaround strategy, has executed that turnaround strategy as advertised and to successful effect. I have no reason to doubt them when they say that 2025 is the year when they return to growth.

Newell Brands (NWL) $7.16: $25.96 by end of year 2026

Why Newell Brands' $NWL turnaround strategy is fundamentally sound.

Capital markets are a second career for me, and after ten years of paying my dues in my first career, I knew that I didn’t have it in me to do things the hard way again. I have become obsessed with trying to find those pieces of information which are the signal through the noise and can dominate a large number of other concerns.

Centrus Energy (LEU):

Keep reading with a 7-day free trial

Subscribe to Value Degen’s Substack to keep reading this post and get 7 days of free access to the full post archives.