Disrupting Higher Ed: Coursera $COUR

A stealth AI company

A quick note before I dive in. I am starting to believe that the theme of the weakening dollar and the reversal of fund flows back into emerging markets and commodities might be more than a year away. I am still holding my starter positions in Ecopterol (EC) and PagSeguro (PAGS), and I will even add to them, but I do not expect them to rally significantly in 2025. The idea that the new administration will try to raise blue-collar wages by competitive devaluation is either incorrect, or the politician below is a liar. At this point, it’s not clear which. It will be interesting to see if blue-collar wages will rise under Trump, or if he fails to bring home the bacon to his core demographic, but time will tell.

The theme that I believe is much more imminent is the Revenge of Cathie Wood. Small cap tech stocks are starting to rally, and many of them are still beaten down since their 2021 highs. In addition to that overall theme, Trump is allegedly going to target education for a major disruption. I might be jaded and cynical to suspect that nothing will happen, but on the off chance that there are major educational reforms, in addition to the former article on Nerdy (NRDY), I want to dive into Coursera (COUR) today, and Chegg (CHGG) tomorrow.

“Times are changing, Betty. These nerds are a threat to our way of life.” - Stan Gable: Nerdy, Inc $NRDY

“You can't always get what you want

Before I jump into the details of the business specifically, the charts for Coursera are exactly what I’m looking for in the Revenge of Cathie Wood.

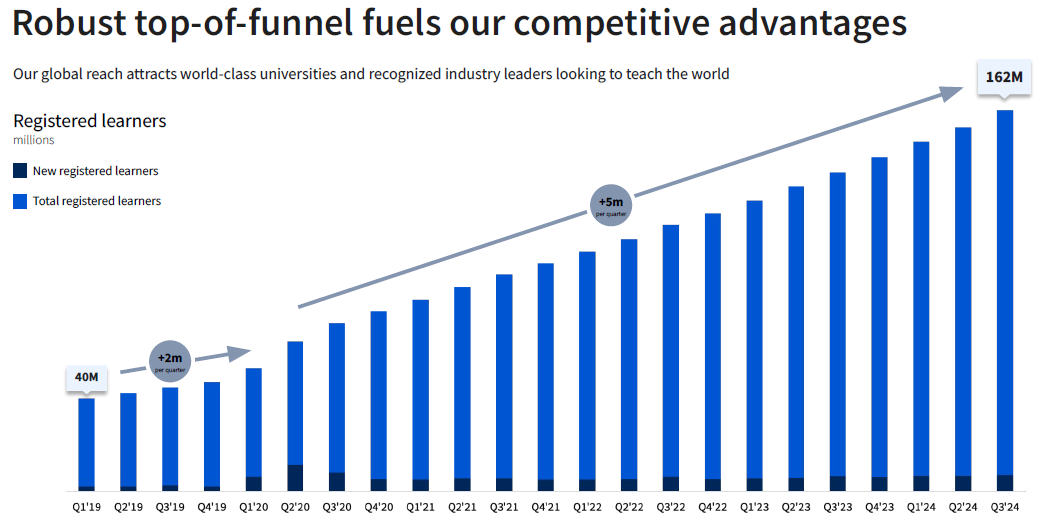

Revenue Still Growing:

Shares Outstanding Not Diluting worse than most tech companies:

Stock Price Completely Bombed Out:

Coursera still isn’t generating heaps of cash, nor does it have positive net income, but it is a high margin, zero marginal cost, network good. Last quarter Coursera added 7 million new registered users to their platform, bringing the total up to 162 million. And that is a very sexy combination of attributes that could fetch a multiple much higher than 1.62x price to sales, or 0.6x price to sales net of net cash. On top of that, Coursera has been generating positive operating cash flow for the last five quarters, which despite net income losses, has kept their cash position stable.

Coursera’s business is broken into three parts, consumer discretionary, vocational training, and higher education.

The consumer discretionary aspect is currently slow, we are in a consumer discretionary slump, people are feeling the pinch of higher rents, higher groceries, and stagnant wages. Self improvement through an online course is a bit high on Maslow’s hierarchy of needs, and can easily be cut from a struggling budget. But consumer discretionary is a sector that I believe will bounce back soon, and if Trump really does get 1% to 2% increase in GDP growth through deregulation, then the consumer will feel a lot better about spending. This is the largest segment of Coursera’s business, but only grew at 3% year over year.

The vocational training segment of the business is based on microcredentials and professional certificates. Coursera has classes on everything from Microsoft Excel certification to Google Cybersecurity and to IBM Data Analytics. These microcredentials are used by customers to help them find a job, or change jobs, or climb the corporate ladder. We are in year two of Silicon Valley’s “year of efficiency” with no sign of the white-collar labor market turning around yet. But this cycle will turn eventually as well, and when it does, you can add Artificial Intelligence microcredentials to the list. The AI microcredentials are only just starting to be created, and have not had a large impact on revenue yet, but management claims that these new broad categories of credentials create structural tailwinds for years as all employees need to acquire them, not just those in the job market currently. This segment grew at 10% year over year.

The higher education segment of the business is a bit of an odd duck. One would think that the universities would view Coursera as competition, and seek to not integrate with them, but one would be wrong. Having recently been employed in academia, I can tell you that incentive alignment is terrible, and if a dean has to have an online strategy, and Coursera offers a complete solution, the eventual death of the university doesn't really come into the calculation. This is the smallest segment of the business, but is growing at 15% year over year.

The big threat to Coursera is perceived to be Artificial Intelligence. It seems at the moment that all small cap tech is assumed to be on a terminal path to zero just because large language models created an interface between human language and statistics. On the one hand, Coursera is integrating their own AI tools through in-house product innovation, and on the other hand, they have an $800 million warchest to make focused acquisitions just in case an AI startup comes up with a Coursera killer, they can buy them out first. Being integrated with 350 universities and 1,560 enterprise customers gives Coursera a certain amount of inertia to resist hungry startups long enough to come up with their own answer to AI. I believe the stock is priced for an inevitable loss while the company is positioned for a probable win on the AI front.

But any serious digging into Coursera would reveal that the founder, chairman, and 5% shareholder Angrew Ng is one of Silicon Valley’s godfathers of artificial intelligence. Andrew Ng’s Machine Learning course is the most popular class at Stanford, and AI for Everyone and Neural Networks and Deep Learning rank at numbers five and six for popularity. To think that Coursera doesn’t have an AI strategy is laughable, Coursera is ground zero for AI strategy. The job disruption that AI brings about will cause tens of millions of workers to retool, get new microcredentials and certificates, and find a new job. I think Coursera will compete for space in my portfolio along with ZipRecruiter (ZIP) and other employment agencies as a major AI beneficiary.

Happy Labor Day! Manpower $MAN, HireQuest $HQI, and ZipRecruiter $ZIP

I remember when I was young and Labor Day was about having a day off from school and possibly even a barbeque. It was long before I learned about the Marxist paradigm of the bourgeoisie versus the proletariat. Even in today’s world where the typical employee with a 5% 401k match with compound interest will earn more as a capitalist than through their …

The major tailwinds for Coursera are the rebound of consumer discretionary spending, Trump’s disruption of higher education pushing for more cost-effective online content, the end of tech’s year of efficiency, and a new layer of AI microcredentials. On top of that, management froze their stock options at $10 per share, so until the share price rebounds, dilution from stock based compensation should slow down a bit. And, Coursera’s management has a new focus on profitability, they are looking to cut costs and let about 10% of their employees go. While most tech companies did this last year, better late than never. Not bad for a company that is operationally cash flow positive and growing revenues.

One last bit of bookkeeping, about $150 million of Coursera’s liabilities aren’t firm, they are deferred revenue. Those of you who read my Douglas Elliman (DOUG) writeup remember that when a company sells gift cards, the value of those sold gift cards show up as a liability on the balance sheet until the final goods are delivered. But in the case of a tech platform, marginal cost is trending slowly toward zero. The $150 million of deferred revenue is a prepayment for either a service with a 56% margin, a 70% margin, or a 100% margin. So that liability is overstated by $60 million, $100 million, or $150 million somewhere about.

Some relief from the overall negative sentiment toward small cap tech and education platforms could return Coursera back to prior multilpes. Price to tangible book is down to 1.9x at the moment, but was routinely over 4.5x in the company’s history. If it takes two years for Coursera to return to those multiples, and it grows revenue at a 10% rate during those years, the stock price would have to triple to catch up. In the meantime, an AI acquisition could change the narrative and bring multiples back to the range of a growth stock as well.

I will be starting a small position on Monday, but I would not be surprised if the stock price were to fall on continued fears of AI disruption, and on uncertainty surrounding the details of Trump education reforms.

their ceo leaving suddenly. i'd be careful here because it's hard to see any traditional content seller as an ai winner.

Andrew Ng's CV makes me feel like a pathetic loser :D