Will a 3D Printing Mania Materialise?: Materialise $MTLS

Crosspost Community

I am back from Pensacola where my wife received a teaching award from the Academy of Economics and Finance, and I got to hear war stories from a small cap value investor who retired at the age of 25 after going all in on an 11-bagger micro cap thirty years ago.

Over the next few weeks it is my goal to try and expand my horizons as much as possible by cross posting with other substack writers, highlighting their top picks. Today’s idea comes from

.The market is in a funny spot, most things have caught a bid, and not much is bouncing along the bottom anymore. It can be emotionally difficult to buy things after they’ve run up 30% to 40% in a short time period. But, buying things on the way up typically works better than buying them on the way down as momentum is such a powerful force in the markets.

One stock that has nearly doubled since November is Materialise (MTLS), an additive manufacturing (3D printing) company with exposure to the industrial and healthcare markets. I haven’t written about a 3D printing stock before, but before I dive into the fundamentals, just as we recently saw with quantum computing, in an aggressive bull market, frothiness can move from theme to theme very quickly. 3D printing is the sort of thing that, just like with quantum computing, could suddenly triple or more as the artificial intelligence narrative rolls across the marketplace in unpredictable ways. For those of us who are not so nimble to jump into themes at the first sign of narrative shifts, it doesn’t hurt to have a few companies that are in a position to get lucky.

The Additive Manufacturing (3D printing) marketplace has three similarly sized public companies in the space, 3D Systems Corp (DDD), Stratasys (SSYS), and Materialise (MTLS). But of the three, MTLS is positioned in the center of the ecosystem as the software leader, even if their competitors have a bit more manufacturing revenue. The leading uses for Additive Manufacturing are rapid prototype iteration, and custom medical devices, but, as 3D printing technology has advanced to be able to work with more useful materials, we are now entering a stage where 3D printed components are being used to manufacture end products, and not just flimsy plastic prototypes. For example, the titanium hinges on the new foldable smart phones are manufactured using Powder Bed Fusion technology. As 3D printing becomes more integrated into manufacturing end products, the market for Additive Manufacturing is projected to double every four years for the foreseeable future.

As the 3D printing software leader, even though software is less than 20% of their revenues, MTLS has the potential to trade at higher multiples than their peers. If it is true that additive manufacturing will be an aggressively growing sector of the economy, 19% CAGR, then MTLS has the potential to benefit disproportionately as they sit like a toll booth in the center of that ecosystem with their software and patents.

MTLS is a European company, domiciled in Belgium. They are aggressively expanding in the US, which is still a huge short term growth opportunity going forward. Despite my expectation for a fast and loose management style due to the meme nature of the sector, MTLS has conservative management which has been focusing on steady growth and profitability all along, as opposed to US tech companies which only started focusing on profitability when the rising interest rates forced them to. Also, the conservative management has very little debt, and $120 million of cash on hand.

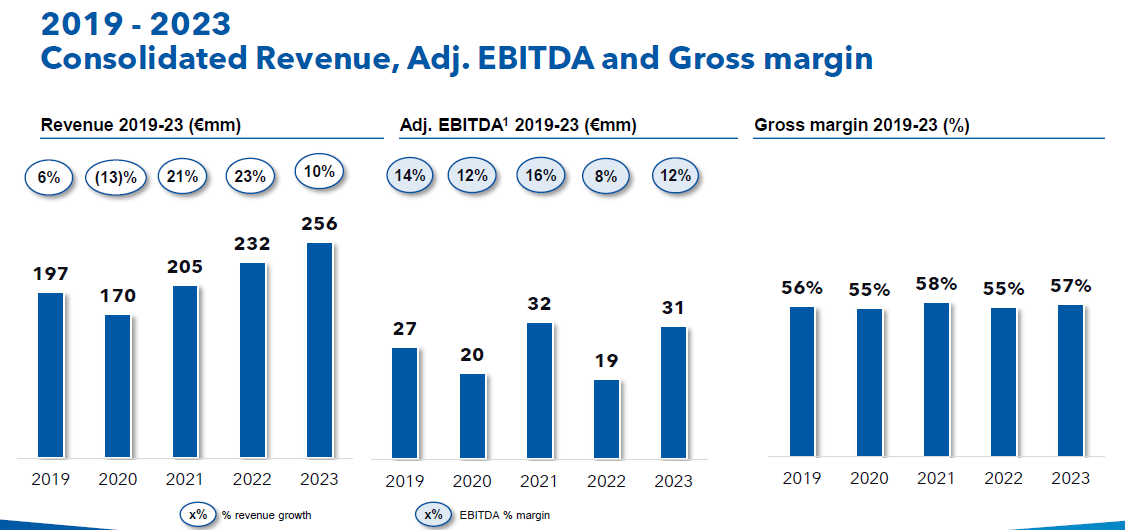

MTLS Revenue:

The type of stock I have been looking for within my “Revenge of Cathie Wood” theme, are stocks who’s revenue chart is dramatically disconnected from the stock price chart in exactly the same way that MTLS is. You can see below, if the circus comes back to town, and 3D printing benefits from enthusiasm again, then MTLS represents quite a lottery ticket that would need to 8x in order to reach past market capitalization, and revenues are 50% larger since that prior peak. However, with EBITDA margins of 12%, and recent revenue growth of 14%, MTLS doesn’t fit into the club of 40 where those aggressive multiples are more expected without the AI narrative shift. Of course 3D printing is likely to be an AI beneficiary, but who can predict how the AI narrative will weave itself through different sectors?

Management is predicting weaker results for next quarter due to the capex for their US expansion. As a value degen, short term bad, long term good, is within my comfort zone. After the stock price has nearly doubled in five months, a pull back is likely on the next earnings call, but in the frothiness of this market, I would never guarantee it. A company trading at a price to sales ratio of 2.0x is hard to think of as a value stock, but in a world where tech darlings driven by a popular narrative can fetch a price to sales ratio of 20.0x, there is potential for good things to happen to MTLS. In the meanwhile, even if it takes longer than expected for the circus to come to town, MTLS is maintaining profitability and growing.

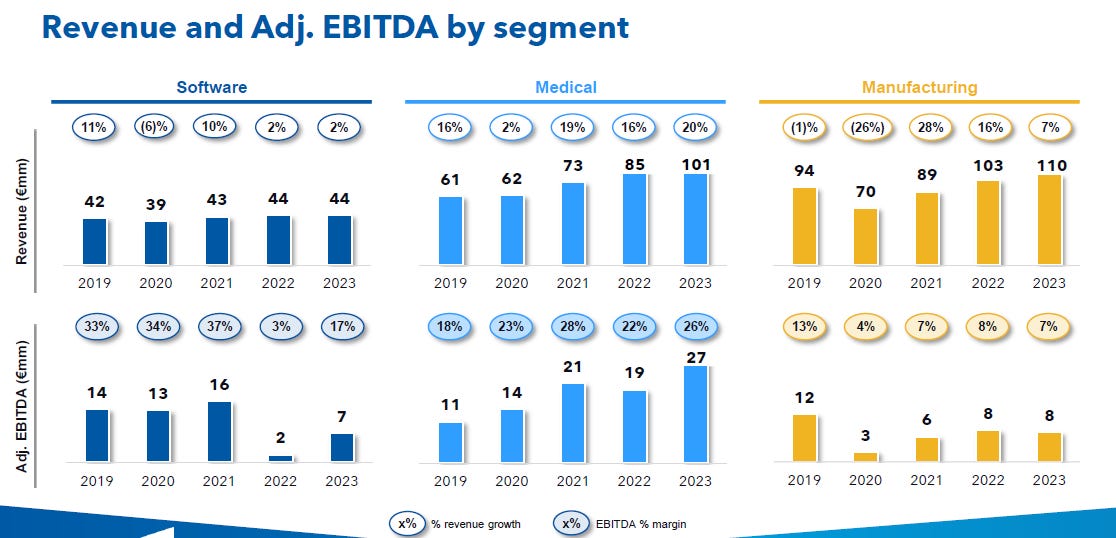

Putting a price target is less of a prediction of what will happen, and more of a prediction of what might happen if MTLS is a beneficiary of the AI narrative. Aside from AI, with the three different business segments, MTLS has a goodco / badco problem, as their Medical segment would likely fetch aggressive multiples due to the 20% revenue growth and 26% EBITDA margins, implying a price to sales ratio of at least 4.0x. A spinoff or sale of the manufacturing business could allow for a significant multiple rerating. Alternatively, the manufacturing segment might not be the deadweight that I am implying due to the fact that the last two years have been a manufacturing recession.

Considering the revenue growth and margins of MTLS’ manufacturing segment despite the recessionary US manufacturing sector, in an economic turnaround, MTLS could catch a significant multiple rerating even without the AI fairy casting her spell on additive manufacturing.

With the rapid growth of 3D printed custom medical devices, the potential for a manufacturing turnaround, MTLS’ position at the epicenter of the sector with their patents and software, and management’s performance during hard times makes me grateful to have had Industrial Tech Stock Analyst point Materialise out to me. It is outside of my typical comfort zone, and I wouldn’t have gone fishing in these waters, but I am not so dull as to be unable to recognize the opportunity when someone bludgeons me over the head with it.

Materialise (MTLS) $9.62: $23.47 by end of 2026 without the AI circus

Materialise (MTLS) $9.62: $90+ if the AI narrative touches 3D printing

| A guest post by

|

-30% on earnings. Oof.

so how does ai and 3d printing intersect for materialise?