Why I am circling Cracker Barrel $CBRL like a vulture.

I might be early but I’m jumping in anyway.

Update: As of 10/25/2024, I have changed my mind on the opportunity with Cracker Barrel. Their turnaround strategy seems like less of a cohesive plan, and more like a “move fast and break things” situation. It was only ever on the watchlist, and now I am taking it off the watchlist. I do have a new favorite restaurant idea:

Paywalled small cap restaurant chain that could 10x to 30x over the next 15 to 20 years.

Hello and welcome to a paywalled small cap stock idea. Initially I was writing one paywalled small cap a week, sometimes I remembered to put my best ideas behind the paywall, sometimes I forgot. Forward Air (FWRD) and Burford Capital (BUR) were probably good enough for a paywall, but hey, I was new at this. Sometimes, the paywalled small cap idea was just mediocre, and I forced it anyway just to try and grow my paid subscriber base. Vital Energy (VTLE) didn’t deserve the paywall, and you have my apologies for it. Conn’s was genuinely a mistake, it had real potential until it went bust.

“Can’t short sumbitchin good biscuits and cornbread until CMG and CAVA offer these on their menus” - Bully McBarbaloot

Not all ideas start out as mine, I would like to thank Bully McBarbaloot for convincing me to look under the hood of Cracker Barrel (CBRL).

Cracker Barrel is down over 60% from their pre Covid highs, their revenues are growing, but their margins are contracting. I must be a masochist, because I love catching falling knives, and I am not smart and / or patient enough to follow the technicals and wait for an inflection. The best I can do is start my position small and average down.

The restaurant space has been a story of winners and losers since the Covid lockdowns were lifted, and there doesn’t seem to be any rhyme or reason to the pattern except for management’s execution. For example, Texas Roadhouse is up 40%, and Bloomin Brands is down 40%, but they occupy the same segment in the space. Similarly Papa Johns is down 30%, but Dominoes is up 30%, and again, they occupy the same segment. To me, it looks like some management teams are delighting customers who are searching for relief from inflation, and some are not.

Cracker Barrel has a new CEO, Julie Felss Masino, formerly of Taco Bell / Yum Brands, and they have just begun implementing a turnaround strategy with 5 pillars and 20 points. The new CEO assures us that they need to make a lot of changes, while at the same time, preserving the uniqueness and essence of CBRL. Listening to earnings calls and trying to predict success or failure based on management’s quality is how I try to add value. The turnaround was only announced on May 16th 2024, so I will have to follow earnings calls for the next several quarters to see if they are hitting milestones or killing a golden goose.

I prefer founder led businesses over slick corporate professional management teams. CBRL is hiring consultants and using the strategies that I remember from my MBA courses all those years ago. But I don’t get as bad of a feeling about the new leadership as I thought I would with all my prejudices against managerial bureaucracy. I am cautiously optimistic.

The new CEO promises that the things which need to be made from scratch, such as dumplings, still will be, meanwhile, things that use up too much labor time, such as cutting fresh pineapple, need to be mechanized and possibly done offsite. Menus will be freshened up with a strategy toward making sure there are items at every price point so that different types of customers can increase ticket size. Prices will be adjusted to the average income levels of the municipalities where they are located instead of being very affordable everywhere. Smart inventory management and brand partnerships can add efficiencies to the retail space. You probably don’t need all 5 pillars and 20 points of the plan, but the plan did sound like it was plausible, and it didn’t raise too many major red flags. I am a little concerned about pricing out their demographic of seniors who’s purchasing power might not be reflected in average incomes for an area.

Store renovations, to maintain the character of the brand while lightening up the color scheme, however, are extremely expensive. CBRL plans to spend $600 to $700 million over the next several years giving the stores a major makeover. And in order to fund this, management is slashing the dividend from $4.90 to $1.00. This was a bit of a shocker to the market, and probably caused a bit of the price drop up to this point.

Management teams really are good at spending shareholder money aren’t they? CBRL is rolling out the changes slowly, and with a great attention to feedback. So hopefully, if they find no return on the capex, they have the presence of mind to change course. Hopefully this slow rollout strategy, starting with 10 experimental locations, and C-suite executives sitting down with diners and getting their feedback, prevents any major mistakes.

In summary, I found management to be a bit cautious, which I find to be a good thing as they are more likely to make changes slowly and carefully. Slow and careful is fine for a business that is still fundamentally profitable, even if at lower levels than in the past. Especially when I believe the cyclicality of the space will turn in their favor, and many of the changes aren’t so urgent, but if done well, could be an improvement.

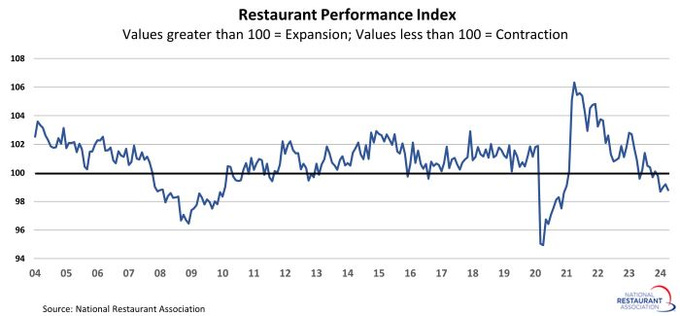

Restaurants generally are in contraction right now. This is probably due to a dining-out bullwhip as people splurged when the lockdowns ended and overdid it a bit, or, we are in a shallow recession that statisticians can’t see due to error in measuring inflation and real GDP. I’m not sure which, but it is pointing to Cracker Barrel’s headwinds eventually turning into a tailwind with a return to normalcy, even if this thesis is just a tad bit early. Longer run, aging baby boomers have $75 trillion in wealth, and Cracker Barrel’s chicken and dumplings are something that can be eaten even without a full set of teeth.

I’m not against jumping in early if the valuations are cheap enough, and the businesses aren’t over-indebted. CBRL has about $472 million in long term debt and their EBITDA covers interest expense 9.4 times. CBRL is trading at a price to sales of 0.3 compared to a pre Covid of 1.0. It is stable enough and cheap enough for me to start building a position, even if I believe things might get worse before they get better.

One good takeaway from management was their intent to experiment with a smaller footprint restaurant to allow profitable expansion into municipalities that didn’t make sense previously. Growth does wonders for multiples. I could easily see price to sales falling a bit further from here if the turnaround has growing pains, but reverting to above 1.0 after CBRL gets their margins back to traditional levels. Buying here would probably result in a return of 3x to 4x over the next few years. I will be starting a small position here, but circling like a vulture hoping for a further decline so that I can average down and eventually have those marginal dollars fetch a much higher return. I do believe Cracker Barrel will survive and even thrive, but I also believe the price hasn’t hit rock bottom.

I will be listening to future earnings calls for any indication that their turnaround strategy isn’t working, or if management sends up any red flags. As for right now, my opinion of them is that their caution and slow rollout of changes will hopefully prevent them from making any major mistakes and destroying the brand.

https://youtu.be/qTliS-Givk4?si=iz1vFPeczpPofIAH

professor strikes first again! https://x.com/marketplunger1/status/1864017019294589236