Who has the most torque to platinum group prices? Anglo American $ANGPY, Impala Platinum $IMPUY, Sibanye Stillwater $SBSW.

Horsepower sells cars, torque wins races.

“Give me a lever long enough and a fulcrum on which to place it, and I shall move the world.” - Archimedes

There are three South African platinum group metals mining behemoths, Anglo American (ANGPY), Impala Platinum (IMPUY), and Sibanye Stillwater (SBSW). Their jurisdictional risk is the same, the market is the same, so if you are a believer in the platinum group metals thesis, which one should you buy? A conservative investor might prefer the lowest all-in-sustaining-cost (AISC), but the value degen might want the one with the most torque to rising platinum group metals prices, provided they have the balance sheet and liquidity to survive until the next bull market.

Forbearance in advance if there are any data errors, Impala is tightlipped with their AISC, and Sibanye Stillwater doesn’t always breakdown the platinum group metals into their components.

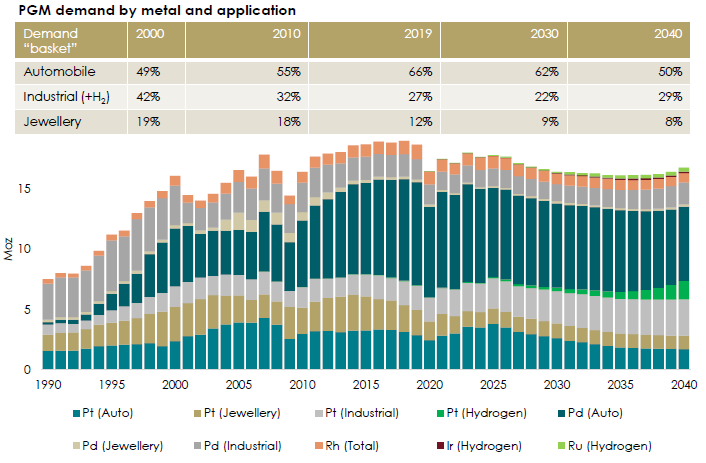

First a reflection on the platinum group metals thesis and its weaknesses. Platinum group metals (PGMs) are a very hard to find group of elements with an enormous variety of uses as catalysts. They are used in hydrogen generation for oil refining, or if governments ever push us into their hydrogen energy fantasy world. But the current largest demand for PGMS is for catalytic converters for internal combustion automobiles. The vast majority of PGMs are found in South Africa, perhaps as much as 90%, so the entire industry is at the whim of South African jurisdictional risk. This makes any non South African PGM deposits potentially that much more valuable in case of South African political failure.

The biggest threat to PGM prices is that trace amounts are found in other sorts of mining, especially copper and nickel, and some of those other sorts of mining move so much earth that their byproduct is an enormous part of the PGM market, potentially 50% of supply. In gold and silver this byproduct supply number is closer to 30%, and in gold, there is so much in storage that annual production doesn’t move price much, but silver can be whipsawed by nearly as much as PGMs. This byproduct PGM might be the reason why current commodity prices are so depressed, Russia’s Norilsk Nickel or Nornickel is an enormous palladium producer, and as a byproduct, attributes zero cost to their stockpiles, which allegedly have been liquidated to raise money for the Ukraine war. We might be nearing a bull market in PGMs if Russia is running out of their stockpiled byproduct. However, if the long term copper bull thesis is correct, the amount of PGM byproduct coming online in ten to twenty years could really wreak havoc on the pure PGM miners in South Africa.

As recently as two years ago, there seemed to have been a consensus that we would all be driving electric cars by 2030, so catalytic converter demand should disappear and lithium demand should skyrocket. But suddenly when benchmark interest rates are 5.3% instead of 0.3%, that narrative seems to have broken down. Furthermore, the hybrid vehicles, which might be the market winner for the next twenty years or so, use more PGMs in their catalytic converters than traditional internal combustion vehicles. Something about the efficiency of the catalysts when they are hot or cold. Shoutout to Trader

for bringing this to everyone's attention. Chemists have figured out how to substitute platinum and palladium, however rhodium remains without substitutes, and rhodium remains mostly concentrated in South Africa with the least byproduct supply, perhaps 20% compared to palladium’s 50%.Platinum and palladium also have some demand as precious metals, with platinum being more expensive than gold for most of history. The current price divergence with platinum selling at a $1,500 discount to gold is an enormous historical anomaly. Platinum demand as jewelry has been finding a new hot market, with grooms at Indian weddings. Gold is considered more traditional for the bride, and grooms are looking for something to set themselves apart. With India’s GDP growing at 7%, and the platinum supply being so small, this could make a big difference in the years ahead.

Taking the three large South African miners, I was surprised to find that their output blend of PGMs was all pretty much the same. I suppose this makes sense since they are all mining the same geologic formation, but I had been hoping one would be richer than the others in rhodium. No such luck. The only exception is Sibanye Stillwater, with about 20% of their production in the US, with a different geologic formation, but that one is particularly parsimonious in rhodium.

Just taking the market capitalization of the miner and dividing it by annual production of PGMs in ounces, with Anglo American you are paying $2,919 for every annual ounce of production. For Impala, that number is $1,651. And for Sibanye Stillwater, that number is $1,343. Of course this doesn’t take into account the enormous differences in their AISC. Anglo American is far and away the lowest cost producer. But looking at the historical commodity prices below, if we see $1,500 platinum, $2,000 palladium, and $20,000 rhodium, they will all earn hefty sums. When you adjust that into a per share basis, those commodity prices would result in an annual income of $3.76 a share for Anglo, $4.58 a share for Impala, and $4.84 a share for Sibanye Stillwater.

All three miners have very manageable debt burdens, with Sibanye Stillwater being in the worst shape. However, SBSW has legacy gold mines and an ownership stake in DRDGOLD, both of which should funnel some income back to SBSW during this period of high gold prices and depressed PGM prices. I consider that more than a fair tradeoff for their debt. The only one of the big three that I don’t like at this price is Anglo American, while many investors focus on the low cost producer, I think at this moment the premium for the market leader is too much. I wouldn’t criticize anyone for owning Impala, but of course, my favorite is SBSW.

Feel free to take a peek at my past writeups on SBSW and DRDGOLD.

Why I love Sibanye Stillwater $SBSW, and thus I hate myself.

Hey ChatGPT, dunk on Sibanye Stillwater (SBSW) in the style of “A Lover’s Complaint” by Sir Thomas Wyatt.

Why DRDGOLD $DRD is the blueprint for how Sibanye Stillwater $SBSW will handle its 60 million pounds of uranium reserves.

DRDGOLD (DRD) is the 50% owned subsidiary of Sibanye Stillwater (SBSW), and it processes the tailings of various South African gold mines in order to extract their proven reserves of 5.79 million ounces of gold. A tailings dump is the pile of crushed rock left behind after a mine has been operating for decades, and they can be enormous.

Anglo American Platinum (ANGPY) 2023 Production 3.244 moz @ AISC $1,050

Platinum - 1.749 moz (53%)

Palladium - 1.269 moz (40%)

Rhodium - 0.226 moz (7%)

Impala Platinum (IMPUY) 2023 Production 2.623 moz @ AISC $1,150

Platinum 1.408 moz (53.5%)

Palladium 1.047 moz (40%)

Rhodium 0.168 moz (6.5%)

Sibanye Stillwater (SBSW) 2024 Forecast: 2.24 moz @ AISC $1,250

SA AISC $1,245 - $1,285

SA platinum - 0.954 moz (53%)

SA palladium - 0.720 moz (40%)

SA rhodium - 0.126 moz (7%)

US AISC $1,365 - $1,425 *Note the Inflation Reduction Act covers 10% unless repealed

US platinum - 0.097 moz (22%)

US palladium - 0.343 moz (78%)

I hold some Generation mining GENM:CN. An interesting pgm play. I’d be interested in your thoughts. It fits your small cap value interest

I would like your opinion on Sylvania Platinum. Good balance and nice dividend.