Who has the Best Razorblades in the Oil Fields? Forum Energy Technologies $FET vs Oil States International $OIS

On my 18th birthday I received a surprise package in the mail from Gillette, one of their signature Mach 3 razors with a single replacement cartridge. While I was a bit miffed that the state of Florida was selling my personal data, I was surprisingly fond of Gillette for the gesture. I think I bought the refill cartridges for that razor for at least a decade, which was the whole point of the marketing campaign. At that time I didn’t understand the razor and razor blade business model. Gillette was willing to give the razor away for free just for the chance to get some of that recurring revenue.

Rig counts and frac fleets have been falling for a couple of years now, but total oil production has still been growing. Efficiencies have been squeezed out of every aspect of shale oil, the frac fleets run for 22 hours a day, six or eight wells are drilled at the same pad which saves on the time it takes to move equipment from well to well, laterals extend for three miles, more perforating charges are used per well, and now several wells are injected with water and sand at the same time, saving on materials and time.

From Oil States International:

I want to look at the companies that are selling the razorblades in the oil patch, and the two at the top of my list are Forum Energy Technology (FET) and Oil States International (OIS). The two are similar in producing manufactured consumable oil services products, and are similar in size. FET had $816 million in revenues in the last twelve months, and OIS had $736 million.

The biggest difference between the two is their exposure to the offshore oil services market. OIS had 57% of revenues coming from offshore manufactured products last year, but FET only had 10% of revenues coming from their subsea category. I am still bullish offshore oil and gas, although the last year has been frustrating as drillship day rates started to chop sideways. Offshore requires a lot more upfront capex compared to shale oil, so in this period of heightened uncertainty, the supermajors are holding back. Meanwhile, more natural gas export capacity is coming online, which drives demand for more shale drilling. I already have exposure to offshore in other ways, so for me, the 57% exposure of OIS is not an attractive quality at the moment.

Both companies’ share prices are in the penalty box, with very low multiples even compared to peers in the beaten down oil services sector. FET is in the penalty box because they were overleveraged coming into Covid, and engaged in an acquisition while their share price was already low. In their defense, the acquisition was $150 million cash and only $40 million in stock, but at such a slow share price, that amounted to a 17% dilution. It might have been the case that the stock component was necessary in order to retain the management team of the acquired company, the only way to tell would be a zoom call with management.

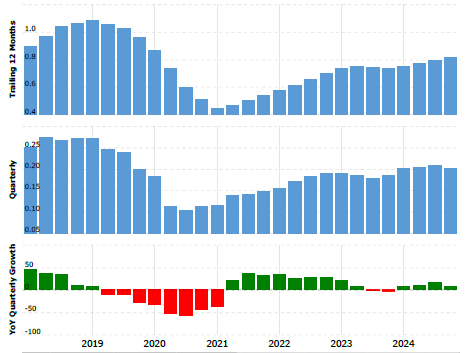

OIS is in the penalty box because revenue per share has been falling since the peak in 2012, and non cash writedowns are masking GAAP net income. Still, FET has been able to maintain overall revenue growth during a tough market while OIS has not, but that revenue growth was partially caused by the dilutive acquisition.

OIS Revenue:

FET Revenue:

The current capital allocation policy of OIS and FET are very similar, both companies have initiated share buyback programs. OIS’ share buyback program has been around long enough to see a few results, while FET’s share buyback program is larger in theory, but is so new that we haven’t seen them implement it yet. FET’s buyback program of $75 million is large enough to sterilize the dilution from the acquisition at these prices, if it is actually implemented. Occasionally some management teams announce share buyback programs for a temporary share price bump, without the intention of ever spending the money, so I will have to wait and see if FET is really serious about their buybacks.

OIS has the better balance sheet, with $125 million of long term debt compared to FET’s $250 million. Both have about $200 million of inventory, but OIS has another $100 million of cash and other current assets compared to FET. So while FET has pre-approved a larger share buyback program, OIS is in the better position to return capital to shareholders.

Both OIS and FET have recent non-cash capital impairments that are hiding their operating free cash flow. FET had $92 million of operating cash flow in the last twelve months compared to OIS’ $32 million. Also, FET consistently has capex of around $8 million a year, compared to OIS’ $30 million a year.

Selling General & Administrative expenses for OIS are only 12.7% of revenues, but for FET that number is 26.8%. FET claims that there are operational synergies to be achieved after their recent acquisition, but that is only half of the story. FET has been focusing on international markets where margins are fatter, but that comes with increased admin costs of operating in so many countries. It does mean that FET has a better chance at growth despite a projected slowdown in US shale, assuming that offshore is in a bit of a doldrum. That assumption isn’t entirely safe as Noble (NE) just announced two new contracts yesterday with Shell in the Gulf of America, increasing their backlog by over $2.5 billion. Those contracts don’t start until 2026, so OIS isn’t likely to sell any extra flanges in the near term, but the rumors of the death of offshore are greatly exaggerated.

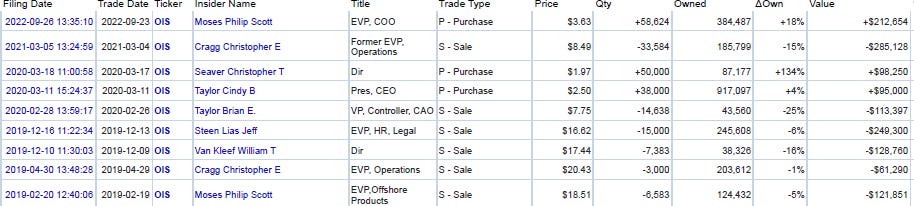

The insider behavior for both companies is slightly positive, with FET being more bullish than OIS. Executives sell stock by default, but they only buy when they believe in the company. OIS had a purchase for over $200,000 by the COO in 2022. FET has had over $800,000 of purchases from the new CEO since 2023, and the new CEO is the former EVP of operations.

Regarding valuation, FET previously traded at a price to sales ratio as high as 3.4x, but OIS only reached 2.8x. But the businesses are similar enough, and those valuations were reached in 2016 and 2017. In the more near term, a return to a price to sales ratio of 1.0x is a reasonable expectation, and reaching a price to sales ratio of 2.0x should be possible with patience. Today OIS trades at a price to sales ratio of 0.32x and FET trades at 0.23x. That leaves room for a 3x to 4x return just on a reversion to 1x price to sales, and much more if momentum carries it back toward prior valuations.

I keep on leaving myself open to the accusation that I love over-levered shitcos, but here we are again. The only thing that I like about OIS better than FET is their balance sheet. In almost every other regard, I prefer FET. Forum Energy Technologies has better insider behavior, fatter margins, growing revenues, and a cheaper valuation. The balance sheet of FET doesn’t give a lot of confidence that their $75 million buyback program is serious, but their 2024 operating cash flow of $92 million tells a different story.

If you buy OIS, it would be for the operational leverage and the improvement that will come when the cycle turns. But for a cheaper valuation, you can buy FET which is already generating decent cash flow today. The biggest risk to FET shareholders would be if management continues to engage in even more dilutive acquisitions. Hopefully the $800,000 that the CEO spent on buying FET’s stock is enough incentive to prevent that risk from materializing.

$FET total debt down to $173.8MM following Q1 earnings. ($100MM of LT notes + $73MM on the credit line which is down from $90MM at 12/31)

Net debt = $146.1MM

The governor on buybacks is the net leverage ratio requirement of 1.5x LTM adjusted EBITDA (~$94mm at 3/31)

I speak with management regularly and they said point blank on the call that they want to buy as much stock back here and it’s still cheap relative to peers at 2x the stock price.

They need to generate ~$7mm cash in Q2 before the ratio is satisfied, after that I expect 100% FCF up to the Q2 ER to go to buybacks. How much? Hard to say. But they had $21mm FCF in Q2 2024, I suspect (guess) they can find $15mm this year. That should allow for ~$8mm of buybacks late Q2/early Q3 (4% outstanding).

They are fighting some EBITDA softness as rig counts fall but should still be able to get $15-20mm into buybacks this year at low end of EBITDA/CF guidance which would be meaningful.

$2mm bought back in January was enough to fuel a beginning of the year run that put them +30% and a huge relative move vs. other OFS names.

I guess LUX does too. It's a turn off for me. Yes they have been buying stock but with the company's money.