When will Goodyear have a Good Year? $GT

Muddling Midcaps

I love being a generalist investor, jack of all trades, master of none. It allows me to stumble across opportunities in any sector, such as when the CEO of Orion Engineered Carbon (OEC) claims that foreign tire manufacturers are dumping inventory in anticipation of US and European import tariffs on tires. Digging a little deeper, the labor union AFL-CIO did indeed submit a claim last November that Thailand was dumping truck and bus tires, and the US International Trade Commission voted in the affirmative to open an investigation. Final determination in this case is due on September 12th 2024. Going forward, since the democrats are pro labor, and Trump is pro tariff, odds might be good that more general tariffs on foreign tires could be forthcoming.

While I am a dedicated small cap value enthusiast, I occasionally flirt with a midcap when they are down on their luck. Goodyear Tire (GT) has been down on its luck for quite a while, and it has been on my watchlist but I hadn’t done a deep dive until today due to my original judgement of their turnaround strategy as not being as serious as Newell Brands (NWL) or Advance Auto Parts (AAP.) Much to my surprise, however, their turnaround strategy is yielding some results, and despite those results, the stock price is lower than ever.

A fallen angel, in 2015 Goodyear had earnings per share of $10.18; today the stock price is $8.70. Market capitalization has fallen from $9 billion to $2.4 billion. A well executed turnaround combined with secular tailwinds from reshoring and tariffs could result in a return to a more historically average price to sales ratio of 0.35 which with $20 billion in annual revenue would be a market capitalization of $7 billion or a stock price of around $24.50, about an 181% return. The turnaround strategy should be in full effect by the end of 2025, so if price follows performance, that price target could be reached sometime in 2026.

First things first, the current data look worse than they are. In 2021 Goodyear acquired their competitor, Cooper Tire, for $2.5 billion. Transaction costs associated with that closing resulted in a $500 million special income charge in 2023. Looking past that special charge, operationally Goodyear still would have lost $189 million that year, but that’s a lot better than losing $689 million. If the turnaround strategy reaches their targets, management wants to reach 2025 operating income of $1.9 billion, which should flow through to net income of between $400 million and $500 million annually, between $1.40 and $1.75 a share. The $24.50 price target would be a price to earnings ratio of about 14. The Russell midcap index has an average price to earnings ratio currently of 17.92.

The Goodyear turnaround strategy has three components, asset sales to reduce debt, cutting costs through efficiency gains, and growing revenue through rationalizing SKUs. Allegedly this should get their operating income margin to double from 5% to 10%. I am not a fan of their chosen asset sales; Goodyear is selling their mining tire business to Yokohama Rubber for $905 million. As I believe we are in a commodity supercycle, and that mining will be a growth industry to fuel green energy dreams, this sort of business is typically less competitive with better margins, and that inflation will evaporate the real burden of that debt anyway, I am not happy with the sale. But the efficiency gains and cost cutting measures have started to show results, despite volumes being down about 3% in the first half of 2024, operating income margin is up from 3.5% to 8.9% in the North American market. This last quarter even had positive net income for the first time since 2022.

The return to profitability, if it holds going forward, is an admirable achievement given the US consumer trading down, the destocking cycle is only just beginning to turn toward increased freight, and allegedly Thailand is dumping inventory ahead of new tariffs. Starting from a foundation of basic breakeven or profitability, it’s a lot easier to give the company time to see if any of the potential secular tailwinds come to uplift them. If truck freight really does pick up, if the US consumer muddles through and stops trading down, or if import tariffs are imposed on foreign tires, then Goodyear could very well be off to the races.

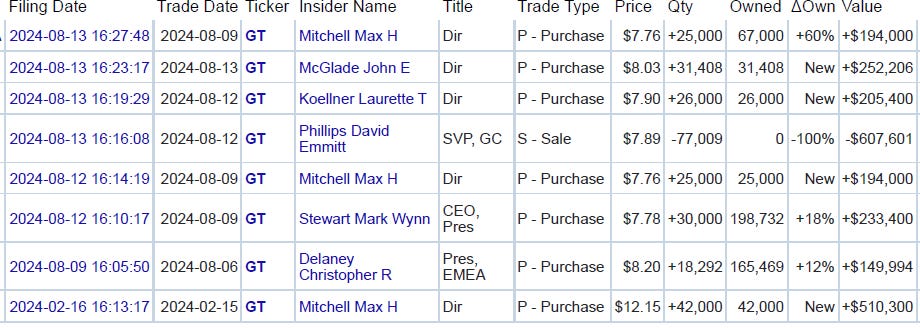

For the first time in years, insiders are buying. There are buys between $150,000 and $250,000 in size from the CEO and three directors. This is the first insider buying activity at Goodyear since 2020, and is a strong indication that buying the stock roughly around the $8 range is a solid value opportunity.

The debt burden is large, about $6.9 billion of long term debt, plus capital leases, plus pension obligations, etc. Total liabilities are closer to $17 billion, and interest expense was $523 million in 2023 compared to $1.28 billion of trailing twelve month EBITDA.

In Goodyear, you have operational leverage and financial leverage, leading to the possibility to generate about a 3x return. But in the small cap Orion (OEC), you have prudent management with much fewer problems, and the possibility to generate about a 45% return based on the same macro trends and theses. This is why sometimes I have to step outside of my preferred small cap arena and take a peek at a few midcaps. Which risk reward profile is best, the base hit or swinging for the fences? I’m of two minds about it.

hmm what about a 3rd mind with more shortterm volatility potential by playing the EC's new ESG-rubber regulations?

Very interesting analysis below, natural rubber suppliers at the end:

https://drive.google.com/file/d/11X9vV6y2YsxsGRppxraVpbalMWiCFUcv/view

Longterm rubber prices preparing for a breakout?

https://www.weber-schaer.com/wp-content/uploads/preischarts/Weber_Schaer-Preischarts.pdf?rnd=1724415362