Vermillion Energy $VET, $VET.TO Westbrick Deep Basin Acquisition Update

For never was a story of worse fate, than this of Vermillion and her degenerate.

I wrote about Vermilion Energy (VET) on June 17th of this year. At that time the share price was $10.92 instead of the current $8.90, a 19% decline. And the shares outstanding were 164 million instead of the current 155 million, a decrease of 5.5%. Market capitalization has fallen from $1.74 billion to $1.39 billion, or 21%. Not a stellar performance, but hardly different than many of their peers in the energy space, especially in Canada. But it is worth noting that there are a handful of Canadian energy stocks that are up 20% this year instead of down 20%, and those are the companies that focused aggressively on share buybacks.

When the stocks you love don’t love you back, Vermillion Energy $VET edition.

Hey ChatGPT, please dunk on Vermillion Energy in the style of Shakespeare’s Sonnets 88-90.

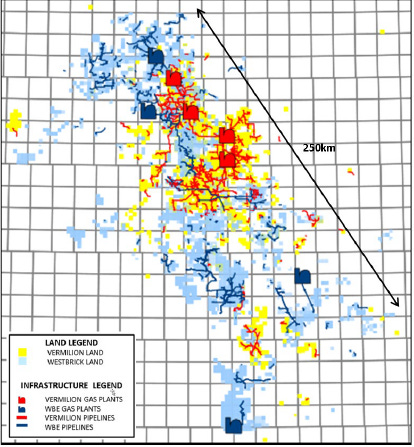

This morning Vermilion announced a strategic acquisition for $1.075 billion CAD of Westbrick’s Deep Basin assets. About 50,000 barrels of oil equivalent per day of production that is 75% gas, 25% liquids, and has a 15 year reserve life. At first glance, this is a good acquisition. Vermillion itself is at 84,000 boe/day and a $2.81 billion enterprise value, or about $33,452 of enterprise value per boe/day with 43% liquids. This new Deep Basin asset is acquired for $21,500 per boe/day with 25% liquids. So even though VET is cheap, Westbrick was even cheaper by some measures. As much as I hate to say it, spending cash this way might be even better than share buybacks.

Also, the acquisition was contiguous to VET’s current existing Deep Basin assets, in many cases already connected via pipelines. This should imply efficiency gains, but VET didn’t tout these in their press release. It’s always a good sign when management doesn’t overemphasize synergies which are often slow to realize.

The elephant in the room for this acquisition is, of course, the realized natural gas price. In another green flag for management, in their projected natural gas prices for Canada, they estimate 2025 prices at $2.34 CAD per mmbtu. I find this estimate to be not overly optimistic, and if this price obtains, then the new asset should generate around $275 million CAD of operational cash flow, $110 million CAD of free cash flow in 2025. With the recent price action for natural gas in the US, and the potential of a cold winter, these natural gas prices might prove to be conservative.

In summary, I don’t hate this acquisition in isolation, and neither did the market with the share price of Vermilion closing just slightly up today, despite an initial selloff on the news.

Outside of isolation, the acquisition does highlight Vermilion’s continuing problems. VET CEO Dion Hatcher is a petroleum engineer, and he has an insatiable lust for drilling programs. On one hand, those drilling programs are done well, and Vermilion achieves results that often surpass their peers, but on the other hand, this weak market is the time for aggressive share buybacks. Even with this new acquisition, the planned 2025 capex just went from $600+ million CAD to $725+ million CAD. Dion already has plans to expand the Westbrick asset from 50,000 boe/day to 60,000 boe/day in the near term. He just can’t stop, won’t stop drilling.

The drilling program is so aggressive, (and growth capex is taken out of GAAP accounting before the net income calculation), that the 2023 growth capex caused VET so show an accounting loss for that year. The quantitative strategies that almost 60% of active portfolio managers use take negative net income very seriously, and there is little doubt that this aggressive growth capex is part of the reason for the suppressed share price.

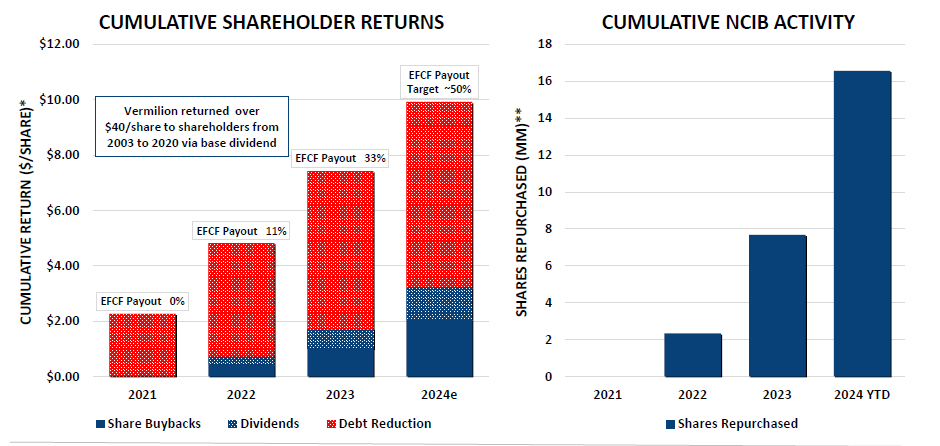

But another part of the reason for the suppressed share price is that natural gas prices were low for two years due to unusually warm winters. And despite the warm winters and low realized prices, VET still generated enough cash flow to retire $1 billion CAD of debt, which of course they have now reacquired.

The biggest complaint against Vermilion is their scant return of capital to shareholders. Management claims that retiring debt is returning capital to shareholders, and this is demonstrably false. Still, at these extremely depressed prices, even the scraps have amounted to a large share count retirement, going from 169 million shares to 155 million shares in the last two years, and accelerating. Returning over $3 CAD to shareholders for 2024 on a $12.77 CAD stock price is not a bad yield at all.

So even though I want to hate Vermilion because they could have done so much more, I have to stop and take notice that during two years of weak energy prices, share buyback programs are accelerating, and despite this new acquisition, the acceleration could continue. If management breaks this pattern of accelerating return of capital to shareholders, then their dismal share price is deserved. But if 2025 reveals a continuing increase in share buybacks, then VET’s share price could easily inflect and start to run higher.

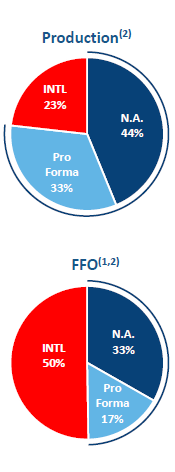

Another possible complaint about this acquisition is that the embedded lottery ticket of European natural gas production is now diminished. Which is true, the International component of VET’s cash flow will drop from being 37% of production to being 23% of production. However, in another very important way it is not diminished, and that is that this was not a stock based acquisition. VET still owns their European assets, and the share count has been reduced. So on a per share basis, the potential upside from a cold European winter is now stronger than ever, not weaker.

Vermilion energy spent two years retiring debt, and now they just unretired it. In exchange for that roundabout journey, production is growing from 84,000 boe/day in 2024, to 126,000 boe/day in 2025, and that is on top of a reduced share count, which will be reduced further as the share buyback program is ongoing, and the share price is still absurdly cheap. And now there are two embedded lottery tickets instead of one. VET will not only do well on a cold European winter, but now they will do well if North American natural gas prices have any sort of recovery toward $4 per mmbtu. North American natural gas was 32% of 2024 production, but only 3% of 2024 operating cash flow. The realized price of North American natural gas for 2024 was $1.45 CAD. These Canadian wells were profitable on just the liquids production, with the natural gas just barely above breakeven.

I want to hate Vermilion as much as Vermilion’s management hates shareholders. But I just can’t bring myself to do it. It is so cheap, has so much potential, and is taking steps that are fundamentally in the right direction. One of these years, one of those lottery tickets should pay out, and when it does, the share count will be lower than when I first bought my VET shares. Until then, every day around $70 WTI is a good day for Vermilion as they generate a 23% return to shareholder yield, and a 33% trailing twelve month free cash flow yield.

The largest risk for Vermilion is a hostile takeover. At prices this cheap, they are a potential target. And if VET is acquired for a 20% premium to the current share price, then I won’t be able to enjoy the journey to $40 or higher. Canada has a legal system that is more amenable to acquisitions, and management won’t be able to use poison pills or other defensive tactics to stop it. Their best defense against acquisitions is that their scattered assets are unattractive to most larger companies, and their debt burden could deter an acquirer. With this recent acquisition, however, the assets of VET are much less scattered, as the Deep Basin acreage is now substantial. Hopefully it doesn’t attract attention. If management starts retiring debt too eagerly, the risk of a hostile takeover only increases. I have written a letter to the board of directors asking them to take the takeover risk seriously, but I am sure I am not the first person to ask them to increase their share buyback program. I might be the first to ask them to stop paying down their debt early.

Any preference on buying on the TSX or NYSE? Surprisingly seems like volume is higher on the US listed stock than the Canadian and IBKR charges a lot more commissions on TSX purchases. I just went with $VET vs $VET.TO but willing to hear reasons to go Canadian.

I like the acquisition - have to wonder why vermilion has high lease operating costs per boe though