The Rocket Rollup Roundup: Rocket Companies $RKT

In the span of three weeks, Rocket Companies (RKT) announced the stock based acquisitions of Redfin (RDFN) and Mr. Cooper (COOP). A downturn in a cyclical industry is typically a great time for consolidation, large players with strong balance sheets can acquire overleveraged smaller competitors, and then come out of the downturn with more market share or new competencies. But with a share-based acquisition the math works out a bit differently.

I have written about Rocket Companies before, formerly Quicken Loans of Detroit, they were a lending company focusing on mass market customers. Mass market is a euphemism for lower class with poor credit. My hat is off to anyone who is able to calculate those repayment rates well enough to make that business work. In this case, that person is Dan Gilbert, the billionaire founder of Quicken Loans who still owns approximately 93% of the company, although after the two acquisitions that number will be closer to 65%.

With so many shares held by the founder, the float of RKT is incredibly thin, and this typically leads to increased volatility and lower valuations. The increased volatility has made RKT a meme stock at times, as the large price swings attract attention on social media from gamblers who like things with large price swings. One of the consequences of making two share-based acquisitions is that the public float is about to increase, and this might bring some share price stability to RKT.

Rocket Companies has evolved since their Quicken Loans days, with a push toward becoming a fintech company, but again, one that has a DNA of focusing on the mass market. In the days before the Artificial Intelligence revolution, the question of which fintech app would be on everyone’s phone was a major topic, Goldman Sachs tried and failed to go directly to main street with their Marcus program. Even though they are a long way from Silicon Valley, I think that RKT has a decent chance of coming out as one of the winners of this fintech contest. The free version of their Rocket Money phone app works with mass market customers, teaching them how to improve and monitor their credit scores, so that when they search for a home on the Rocket Homes app, they are more likely to qualify for a mortgage. Then those app users are highly likely to originate their mortgage through Rocket Mortgage, in which case, the mortgage originates with almost no cost.

For a typical mortgage origination, marketing expenses can be as high as half of the origination fee. Rocket Companies is slowly creating an ecosystem for their repeat customers that approximately half of their current mortgage originations come at no cost. The process is so painless, that they have an 80% recapture rate; when people move to a new home, or refinance their mortgage, they stay with Rocket Companies. The industry average is a 25% recapture rate, because most people are pretty ambivalent about who their mortgage lender is. Also, Rocket has expanded into title insurance and escrow in order to capture even more of the home purchase value chain.

Fitting into this ecosystem very nicely will be Redfin (RDFN), which will widen the top of the mortgage origination funnel, also at very little marginal cost per origination. Redfin is not currently profitable, most tech companies aren’t until they choose to be. That’s just venture capital culture, which will potentially change under the Rocket Companies umbrella. Don’t misunderstand me, Rocket has spent a lot on R&D themselves, but they do it on top of a basically profitable base. If you take out R&D expense, Redfin is about at breakeven already. But how many mortgages need to originate from Redfin’s 50 million monthly visitors before the $2.36 billion acquisition pays for itself? Redfin currently only captures about 27% percent of the mortgage origination from real estate transactions that are caused by their platform, there’s a lot of room for improvement. It was a share based acquisition, so is Redfin worth 5% dilution? I think unequivocally yes, this strengthens the Rocket ecosystem, widens the top of the funnel, and will be highly accretive to Rocket Companies once the two companies are integrated smoothly. Adding Redfin’s $1 billion of annual revenue to Rocket’s $4.6 billion for only 5% dilution is an incredible acquisition.

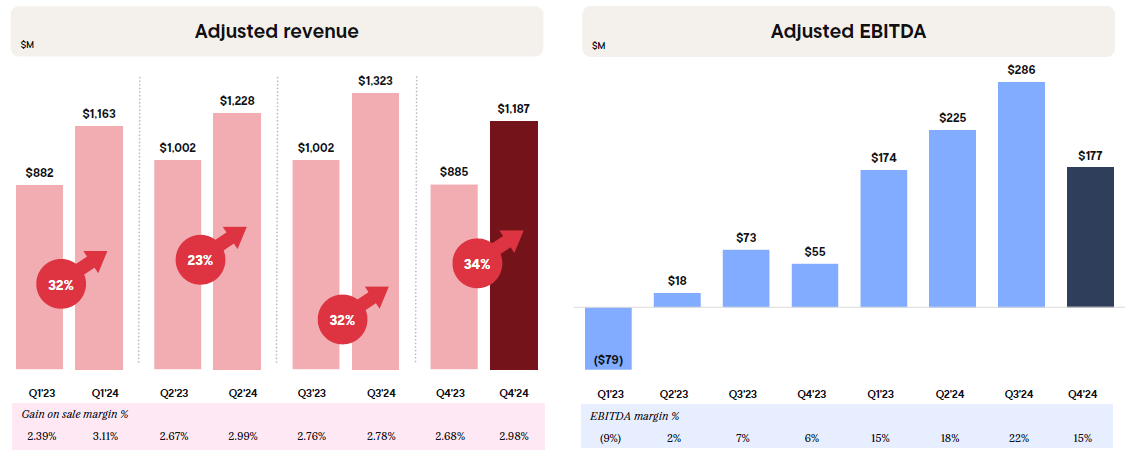

But mortgage origination is feast or famine, and in the last two years, it has been famine. Real estate transactions are way down with the higher interest rate environment. The part of Rocket’s business that provides stable income during tough times is mortgage servicing. Rocket Companies services about $590 billion of mortgages spread across 2.8 million loans. This provides about $900 million of recurring annual revenue in good times and in bad.

Mr Cooper (COOP) is also a mortgage servicing company. This acquisition is not about adding new competencies, it’s about taking market share, and it takes the most stable recurring revenue in the mortgage market. Adding COOP’s $1.6 trillion to RKT’s $590 billion makes over a $2 trillion mortgage service book, and it should provide combined over $2.2 billion of annual recurring revenue. This acquisition cost about 25% dilution, but this time it was for a profitable company with around $670 million of net income in the trailing twelve months, and $3 billion of revenue. And remember, the trailing twelve months were terrible for the mortgage business, COOP also operates as a mortgage originator.

Strategically, I believe the acquisitions are fantastic. And as for valuation, amazingly RKT was trading at a higher price to sales ratio and price to earnings ratio than COOP, which means that a share based acquisition should increase the earnings per share and revenue per share of RKT shareholders. Usually with acquisitions we see costly mistakes from empire-building CEOs who make questionable deals that destroy shareholder value. But in this instance, we see an immediately accretive acquisition with COOP, and a very high probability that Redfin will provide enough synergies to be accretive as well. The only criticism I can see for the share based acquisition of COOP would be that in past boom years, COOP had much less responsiveness to the boom, as such a relatively small percentage of revenues are from origination versus servicing.

On many metrics, RKT is not a cheap company, 16x forward price to earnings, and 5.65x price to sales is not typically deep value. Rocket Companies only had $5 billion of revenue in 2024, but in 2020 that number was $15.6 billion, and in 2021 that number was $12.9 billion. The current state of interest rates and the frozen housing market has dramatically depressed transaction volumes. Mr Cooper is much more stable, with only $3.3 billion of revenue in 2021 compared to $2.2 billion in 2024, but net income in 2021 was $1.4 billion compared to the $670 million last year. Rocket Companies’ GAAP net income isn’t impressive, as a tech company they keep on ploughing profits into research and development, but EBITDA in 2020 was $9.7 billion compared to $930 million last year.

A housing transaction boom like 2020 and 2021 might not come again any time soon, but we could see a return to a more normalized housing market if Treasury Secretary Bessent were really able to get the 10-year treasury down to 3.5%, allowing for a 5.5% 30-year mortgage. As an aside, Rocket Companies is preparing their marketing materials to heavily pursue refinancing of more expensive mortgages, as that allows them to capture a new origination fee, and they soon will have a $2 trillion loan book, with 20% of that above a 6.0% interest rate.

A return to a normalized housing market could see a Rocket Companies with over $7 billion of EBITDA, and revenues of $13 billion, give or take. After the dilution from the two pending acquisitions, EBITDA per share could go up about 5x on a return to more normal market conditions, and revenue per share could easily double. How much should you pay for a company that doesn’t lose money in a terrible year, makes around $7 billion in a normal year, and probably makes around $16 billion in a boom year? At the current share price, after the dilution from acquisitions, that would imply about a $37 billion market capitalization currently.

I would call that about 2.3x peak EBITDA, about 5.3x normal EBITDA, and about 7.4x trailing 12 month adjusted EBITDA. Still not outrageously cheap, but things start to look much better when organic growth rates are included. Since 2020, Rocket Companies has organically increased market share for refinancing from 10% to 12%, and for mortgage originations, market share has increased from 3.3% to 4%. And all of this is before any increase in volumes from acquiring Redfin, or any of the $500 million annual potential synergies from the acquisitions. RKT is currently the market leader in both, and has a longer term goal of taking 20% market share for refinancing, and 8% market share for mortgage origination.

So while the current valuation of around 5x normal EBITDA or 2x peak EBITDA isn’t screaming value, if RKT is able to grow into their desired market share over the next several years, it is a very attractive price. Beyond growth, in recent years all profits have been reinvested into technology. With this new economy of scale from the acquisitions, Rocket Companies should be closer to the point where they are comfortable returning capital to shareholders. I have no idea what form that would take, dividends or share repurchases, but RKT already trades at 5x EBITDA without any return of capital at all.

Looking out to full year 2027, if Redfin is integrated well, we could see a Rocket Companies with 50% more market share than they had in their peak years of 2020 and 2021. That would put 2027 full year EBITDA somewhere around $9 billion in a normal year, or upwards of $18 billion during a housing boom. If there is no multiple expansion or compression, that would be around a 27% price increase from here. Obviously growth stock investors would be looking for multiple expansion to drive their returns above 27% for two years, but I am reluctant to rely too heavily on synergies and the Redfin pipeline to value RKT.

Rocket’s growth has been so aggressive, even in a dismal market environment, I believe there are good odds of being pleasantly surprised. So while I am not putting too high of a price target on RKT, I do believe it has enormous potential to surpass my target.

Rocket Companies (RKT) $13.19: $16.75 by the end of 2027.