The Little Forklift That Could: Hyster-Yale $HY

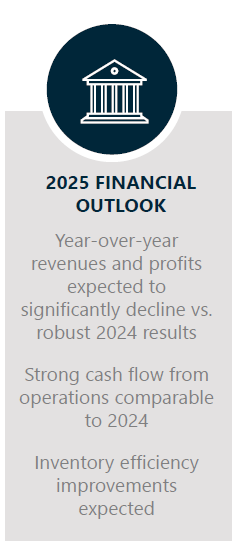

I wanted to dive deeper into forklift manufacturer Hyster-Yale (HY) as a part of my due diligence process on Alta Equipment Group (ALTG). As a standalone investment, HY is undervalued, but it is very early. Due to Research and Development expense for a product refresh cycle, HY is projecting dramatically decreased GAAP net income for 2025, so while the stock price is currently weak, I think odds are very good that over the next six months at least, the stock price will become weaker still. I think it will be a good idea to watch HY closely, because if the stock price continues to decline, the opportunity might arise to buy it at a valuation that would lead to a four bagger. Not today, but at some point in 2025 or early 2026.

As I started digging into this new little Industrial, I was hoping to find a family business. Unfortunately it was a bit too old to still be a family business, Linus Yale started in 1840, the company was sold to NACCO of Japan in 1989, and was spun off in the US again as a standalone entity in 2012. So instead of a scrappy entrepreneur with aligned incentives, we get a much more mature global corporation in Hyster-Yale (HY), but surprisingly with a significant anchoring shareholder, albeit without the incentive alignment.

The starting CEO at NACCO after the acquisition of Hyster-Yale in 1989, Al Rankin, is still alive and kicking, and still the executive chairman of Hyster-Yale. I don’t know if he ever bought into the company over the last 36 years, but his stock based compensation leaves him, his charitable trusts, and his family members with something around 38% of the company. Hyster-Yale unfortunately, does not have a culture of returning capital to shareholders as much as a culture of outrageous executive compensation. Even with $5 million of share buybacks last quarter, it isn’t enough to sterilize stock based compensation. This would normally be where I would stop my deep dive into the company, but I will trek onward for the sake of Alta Equipment Group.

This sort of professional manager controlled business does usually have a few good ideas operationally here and there, even if they routinely loot shareholders. Several years ago, HY initiated a process of rationalizing their dealer network, consolidating and replacing the worst performing dealerships. This is what initiated ALTG’s 16 acquisitions since their IPO. Many of which were dealerships that were operated by proprietors who had lost their chutzpah after a long career, or their children who never had any chutzpah to begin with. This means that not only is HY’s America revenue growing in a very tough market, but ALTG’s acquisition prices of 4x-5x EBITDA is understating what those dealerships will be when they take the market share that HY can typically take with their product offering.

I mentioned that Hyster-Yale was in the middle of a product cycle, they are bringing forklifts out of the 4th generation and into the 5th generation with an emphasis on compatible and versatile modular systems. This is going to wreck their GAAP accounting financials for at least the next six months, maybe more, but it could provide an opportunity for ALTG as forklifts can often last upwards of 30 years, and there haven’t been all that many new product cycles since the first Yale lifting machines of 1920. Eventually, the goal is for these modules to be assembled at the dealership so that the client can receive their customized forklift quickly without the need for a custom order from the factory. This could be a driver of future profitability for both HY and ALTG if the market is willing to pay up for customizability.

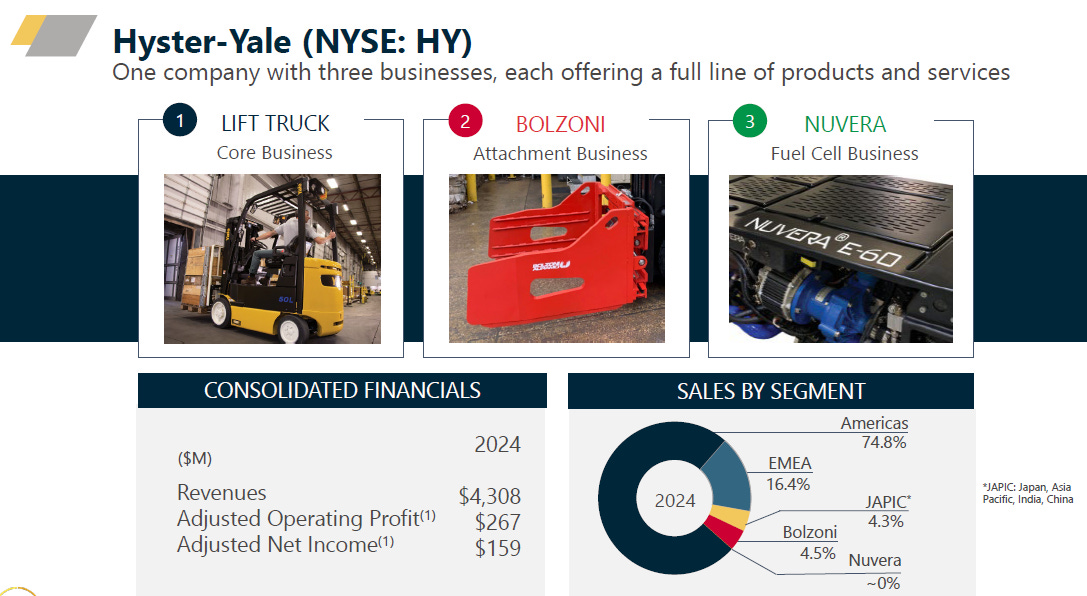

Hyster-Yale has been expanding the breadth of their offerings through acquisitions. While HY derives 76% of their sales from the Americas, Bolzoni is one of the largest forklift attachment manufacturers for the EMEA region (Europe, Middle East, and North Africa). If executed well, Bolzoni attachments could help HY penetrate EMEA, and HY can help Bolzoni penetrate the Americas.

Other acquisitions include a telematics company as well as Nuvera, a hydrogen fuel cell company. HY has also deployed about 700 automated forklifts, with software from a third party. Hydrogen fuel cells, telematics, and automation are still early, but it is probably a decent signal that Hyster-Yale is positioning itself to be where the market might move to eventually. I find this helps to remediate a major risk from Alta Equipment Group, they wouldn’t like to see a Tesla type forklift tech startup bypass the dealership business model.

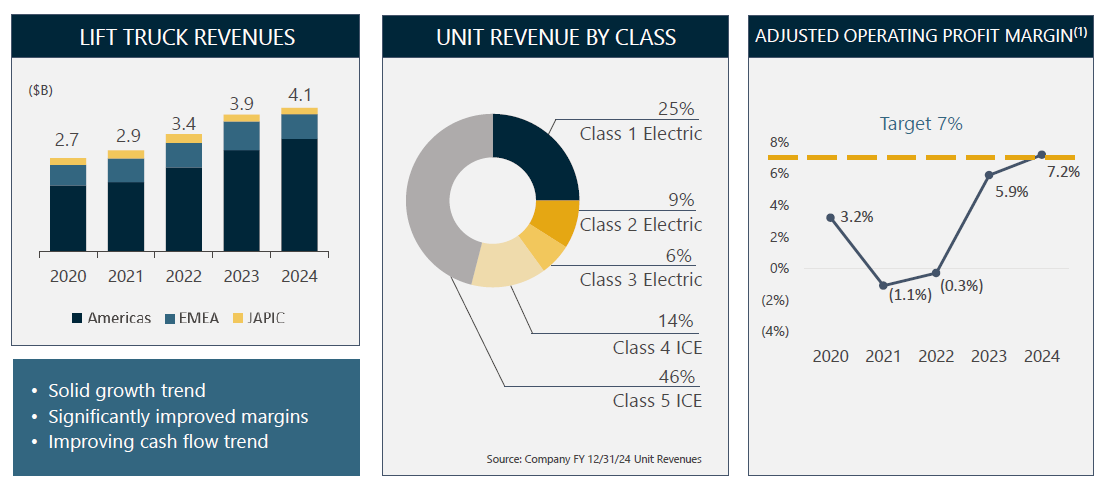

The current product mix of Hyster-Yale tells a lot about Alta Equipment Group’s current customer base, as well as potential for growth in the future. A full 60% of HY’s sales are from class 4 & 5 internal combustion forklifts, the huge honking industrial machines. Globally, this segment is less than a fourth of the total market, which means that HY has disproportionate market share in the industrial segment, as well as the potential to use their dealership network to take market share in the class 3 electric forklift segment which comprises 6% of HY revenues despite being 52% of the global market.

Also, despite a dramatic increase in demand in 2021 and 2022 due to the Covid supply chain crisis, HY suffered during this period as ALTG thrived. Even with a dramatic increase in demand for products, the increased cost of shipping and the disruption from unavailable components crushed HY’s thin margins.

Regarding tariff risks, HY does a significant amount of their manufacturing in the United States, however, most electronic components are sourced abroad. Also, an increase in steel and aluminum prices could become a cost driver. The large domestic competitors for the class 3 electric forklift, Toyota Materal Handling and privately held Crown, also both have a significant US manufacturing footprint, so the competitive effect of tariffs is probably a wash for Hyster-Yale. Most companies have been moving assembly to the US for years to be competitive.

Regarding valuation, Hyster-Yale has dramatically grown revenue per share over the last few years, driven primarily by the dealership consolidation and optimization. Revenue per share is up from $160 per share in 2014 to $243 per share today, despite the stock price falling from $76 in 2014 to $45 today. A return to the past peak price to sales ratio of 0.5x from the current 0.19x would be more than a double. However, the catalyst for positive stock price momentum will probably come when the earnings impact of the current research and development cycle wears off. Management believes the return to earnings growth will start in the second half of 2025, however, management is guiding toward revenue and profits to “significantly decline” before that.

I wonder how accurate management’s predictions will be, given that the dealership consolidation and optimization program is working, they are taking more market share, and ALTG said that volumes were up immediately after the recent election. Also, due to a working capital drawdown, 2025 free cash flow is expected to be steady. Sometimes the stock price can move on this alone, as recently occurred with Titan Machinery (TITN) releasing $300 million of working capital unexpectedly last quarter, bringing the stock price from $12 to $17.

The 2022 lows for Hyster Yale were around $21 a share compared to today’s $45. Will the next six months be bad enough to cut the stock price in half? Is the market still in its unforgiving mode, or have we moved back into a period of bullish euphoria? With my very limited technical analysis, gaps often get filled, and HY had a gap up from $32.60 to $47 in March of 2023. And that $32.60 level was a point of strong support in the past, but so was the $36 level before that. So I would put Hyster Yale on a watchlist and look to enter in the low to mid $30s, relatively confident that at their next peak valuation, they could return to the 2014 and 2021 peak of $100 per share, or even as high as $150 a share based on peak multiples of 0.5x price to sales and the recent rapid revenue growth from dealer optimization. HY has very little long term debt, and even with their dreary forecasts, expects to be net income positive through 2025.

Hyster-Yale (HY) $45.19: Try to buy below $36 per share, price target of $120 by the end of year 2030.