The good, the bad, and the Peabody: Peabody Energy $BTU

Coal, the new whale oil

“I was born one mornin' when the sun didn't shine

I picked up my shovel and I walked to the mine

I loaded sixteen tons of number nine coal

And the straw boss said, "Well, a-bless my soul"

You load sixteen tons, what do you get?

Another day older and deeper in debt

St. Peter, don't you call me 'cause I can't go

I owe my soul to the company store”

The sun is probably setting on the age of coal, not because of windmills certainly, but because the artificial intelligence revolution made nuclear fission permissible to public opinion makers. The West turned their backs on nuclear fission in the 1970s, then propagandized us endlessly with shame, guilt, and fear over the impending calamity that would be caused by our immoral energy consumption. It was like growing up Catholic all over again. But there are only two kinds of people, those who are pro nuclear, and those who don’t understand nuclear. Expect a post on my favorite uranium companies within a week or two.

So why am I attracted to a sunset industry? Because that sunset will take decades, and in the meantime, supply might contract faster than demand leading to outrageous profits. Who wants to build a new coal mine with a ten-year breakeven, when the industry trades at a price to earnings ratio of six? And on top of that, no bank would lend you the money as they have ESG pressure to stop lending to fossil fuel companies generally, and coal companies more specifically.

You may have seen this chart on the whale oil industry; whale oil volumes started to decline by about 1847, but prices rose and profitability improved dramatically, reaching a peak around 1867, and profitability per unit remaining high until at least 1885 but on lower volume.

A threat to this pattern repeating in coal is development outside of the OECD countries, but they tend to have poorly developed capital markets. Walking into coal I don’t expect a multiple rerating industry wide, although perhaps for specific companies. For the most part the market is only relying on cashflow returned to shareholders, and those cashflows could be huge. And after every year of outrageous profits, those who missed out will comfort themselves with sour grapes by proclaiming that coal only has just a few more years left to go. We are fools to buy them at a price to earnings ratio of five or six, they will say, and there is a good chance they will say this every year for twenty to forty years.

There are two main types of coal, thermal coal and coking or met coal. One is burned to spin turbines for electricity, the other to add carbon to iron to make steel. My understanding is that technologically thermal coal is more easily replaced in the near term than metallic coal, but logistically, the size of the electricity generation industry and the slow speed at which new capacity can be brought online, as well as the ever increasing energy demand, make thermal coal a moving target. Coking coal is harder to replace technologically as the recipes for making virgin steel without coke are not really ready to be taken off the shelf and scaled up quickly. But logistically, currently about 60% of steel is recycled, and 40% is virgin, so there is room for electric arc furnaces to decrease coking coal demand somewhat. Except that the capex required for electric arc furnaces is huge, and steel mills trade at cheap multiples also, so rapid expansion is unlikely. The amount of coal used in steel making is much less than thermal; in 2022, the world burned 8.4 billion tons of thermal coal, and probably about 1 billion tons of coking coal, but that second estimate may be off.

Borrowed this chart from Thomas J Shepstone who didn’t say where he got it from:

So in summary, the expert consensus right now, even if eventually incorrect, is that coking coal has greater longevity than thermal coal, and this view shows up in the price to earnings multiples that met coal miners receive, around seven to ten, compared to thermal coal, around six. I do believe there is room for multiple contraction here, if you buy coal stocks, don’t be shocked if the price to earnings falls to three, just buy more.

Another attraction to the coal space is the recent commodity price squeeze that took place after the start of the Ukraine War. This has provided most of the coal miners with a sudden windfall of cash which most have used to retire their debt. Warrior Met Coal (HCC), for example, retired half of their debt in a single quarter. To all those who think that small caps are depressed due to debt maturity walls from rising interest rates, well not in coal. But a caveat to those of you who are in coal for a repeat of that price squeeze, those things don’t tend to happen in the same commodity twice in a short period of time. The price squeeze was caused by Europe building up their reserves in an emergency setting, and after two warm winters, are sitting with comfortable coal storage. It will be interesting to watch what happens to coal prices if the winter is average, or maybe a bit colder than average, but I do not expect another price spike like the one below.

A threat to the coal thesis is that energy is somewhat substitutable, there are furnaces that can switch between coal and natural gas. So even though I am not aware of any public thermal coal companies expanding production of thermal coal, the incessant shale revolution and its associated natural gas has the potential to suppress thermal coal prices domestically in the US. There are export terminals and LNG tankers coming online in 2025 to relieve some of the pressure in the US, but the difficulty of transporting natural gas, especially with the need for import terminals and storage tanks on the other side of the ocean makes me think that US natural gas prices, and therefore US thermal coal prices, could stay somewhat depressed for a long time. Internationally this threat is much less, so coal exports are critical to profitability.

To me as a generalist, I have to treat coal commodity prices as an existential risk that limits my position size. I have my opinions about what will happen, but then I remind myself that I am not a coal expert, and this writeup is becoming too long anyway.

I had initially started writing a comparison of several coal companies, but as a value degenerate, Peabody Energy (BTU) is just so much cheaper than the rest, and probably for temporary reasons. So here I am once again at my filthiest habit, embracing the laggard.

BTU is cheap, really cheap, half of the price to sales and a third of the price to book ratios of their thermal coal peers, and things that are cheap usually have problems. But the good kind of problems are the ones that go away on their own, or in the regular activities of reasonable management. Even better problems are the kind that the market believes are a negative, but are actually a positive that is unappreciated by the consensus.

The Good:

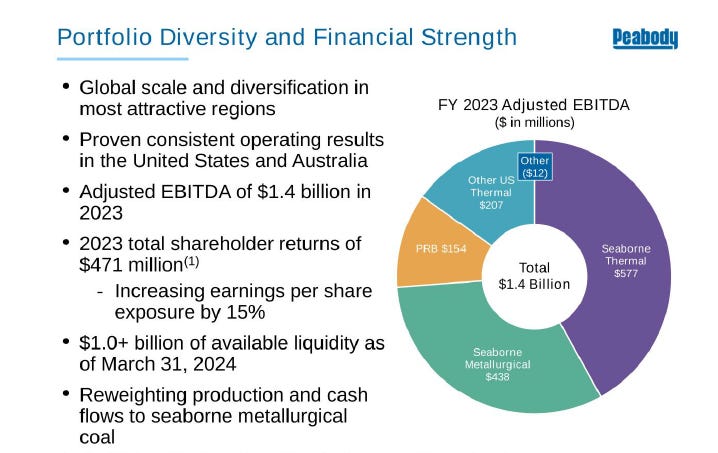

Peabody Energy is large, and for the last twenty years, the market leader tends to fetch a higher multiple, and this might be exacerbated by market-cap weighted ETFs. BTU doesn’t have a higher multiple right now, but there is a chance for a multiple rerating not just to catch up to peers, but to surpass them. In 2022 BTU mined 17% of all domestic US thermal coal, 102 million short tons; they are 38% of the Powder River Basin coal production.

Peabody Energy is growing, while most of their peers are looking to transition away from coal, such as Alliance Resource Partners (ARLP) plowing their profits into Permian mineral rights, BTU is building out a major met coal deposit in Australia with the Centurion mine expected to produce 3.7 million tons of met coal in 2026, not quite doubling BTU’s met coal composition. The only competitor doing a similar large met coal buildout is HCC. The market has BTU at the same price to earnings multiple of six as their thermal peers, but their thermal peers aren’t spending on capex, so BTU has a lower multiple when measured by gross profit. It is unknown if management will continue growth capex after Centurion, that is a risk to a short term rerating.

Peabody Energy is pivoting toward met coal, the likely longer term success story over thermal coal. Price to Earnings multiples on met coal competitors are consistently higher than on thermal coal. If BTU can be a primarily met coal company, and get placed into a different category in the datasets used by the quantitative strategies, they could get a price to earnings multiple rerating from six to seven or higher. So not only will BTU have higher earnings when Centurion is finished, they could even get a multiple increase on those earnings, and again, a multiple increase for being the size leader.

At 2023 coal prices, the Centurion met coal mine should add $234 million to EBITDA in 2026, and BTU spent about $150 million on growth capex in 2023. So that free cash flow swing will be somewhere around $380 million increased free cash flow. Without a multiple rerating, that would imply a stock price of $37, and with a rerating to a price to earnings of 7 for being a met coal producer, a stock price of $50, not including share buybacks.

The Bad:

Peabody Energy was on the brink of bankruptcy before the coal price spike. While most of their competitors are near debt free, BTU started from so far behind that they still have $380 million or so of long term debt to pay down. They want to be debt free, because before the Ukraine War windfall, ESG pressure on the banks was cutting off access to debt markets. This has caused management to want to maintain $1 billion in cash to weather down markets. Shareholders don’t like dead money, but it provides an uncertainty cushion, and at least that’s another $50 million in annual EBITDA from short term interest rates.

The precarious state of their finances prior to the windfall caused their insurers to place restrictive covenants on Peabody. Mining companies need a special type of insurance policy to cover the cost of remediating the land back into reasonable condition, this is called a surety bond. BTU’s surety bond holders restricted any return of capital to shareholders until it was renegotiated in April of 2023. The new covenants simply require BTU to keep a minimum of $400 million in cash as collateral. Investors are unhappy with the status of this dead money, but I am less bothered by it. It’s just one of many barriers to entry that protect Peabody’s monopolistic status.

Peabody’s competitors had a huge head start in their share buyback programs. This caused an enormous negative sentiment from retail investors who are unhappy with the laggard status. BTU did eventually allocate $1 billion to a share buyback. So far, about $430 million has been spent, last quarter $85 million shrank the float by 3%, and there is $570 million left to go. Investors are unhappy with the slow pace of the buyback, and the lack of effect this has had on the stock price. I think it’s fantastic that BTU has been able to reduce the float so cheaply. I hope that Peabody stays at below a price to book of one for the next six quarters so they can reduce the float accretively and by another 18%. Why would investors want the stock price to rise into their own share buyback program? A share count reduction of 18% turns that prior estimated share price of $37 to $45, and the $50 target to $60.

So not including what Peabody Energy earns in the next eighteen months after capex and paying down debt, probably an additional $600+ million at current coal prices, just trundling on and dribbling their share buybacks out at a slow pace, the stock has a path to triple in two years. Of course, even if the share price tripled, why would you let go of something that would have a 2026 free cashflow of $1 billion even if it traded up to a market cap of $9 billion from $2.7 billion, if it was plowing that money into buybacks and dividends? If the $600+ million Peabody could earn in the next 18 months is spent well, and if coal prices improve at all, BTU could even see a higher stock price than the rosy estimates here.

The biggest threats to Peabody Energy are unpredictable coal prices, and management’s capital allocation decisions. There has been no insider buying, and there are no large shareholders or activist investors reminding management about their fiduciary obligations. Management’s language on earnings calls and on their investor day presentations leave me cautiously optimistic that BTU will err on the side of returning more capital to shareholders and not less. But if I see a large capex plan to expand thermal coal production, I will cut my losses and close the position. Until then, I love this laggard.

I need to check but Russia is a huge coal exporter right? I wonder if their coal is banned now in the west and how coal price will be impacted once the war is over.. cause we are approaching rather end of the war now. Before entering coal it is good to check if we don’t have oversupply issue coming up