Status Update: Applied Optoelectronics $AAOI

I am slowly starting to appreciate the data center buildout. Maybe that’s a sign of the top, I hope I’m not your contrarian indicator. But I believe the data center buildout will go on until lenders are unwilling to lend any more for it, and we only recently saw the very first hyperscaler use any debt at all when Meta used $26 billion of debt for their new Louisiana Hyperion project. Meta has $90 billion of trailing twelve month operating cash flow, so they could have self-funded, but they chose debt so as not to impact return of capital to shareholders. In 2024, construction began on 7GW of new data centers in the US. In 2025, that number is projected to be 10GW, and to stay relatively flat around 10GW of capacity per year until 2030.

Applied Optoelectronics (AAOI) has been one of my favorite companies to use for generating income by selling a modest handful of puts here and there. The implied volatility is enormous, and they are a data center hardware supplier. We are still in the stage of the AI revolution where all suppliers will be needed to satisfy demand, and the rising tide lifts all the boats. At some point, when the AI narrative matures, the winners will be able to build out capacity and the losers will suffer a loss in market share. As long as we are a year or two away from that, I am still comfortable selling a put here or there on AAOI. But I do need to check in occasionally and see if they are on track to be a winner or a loser in their niche when this whole AI thing starts to calm down.

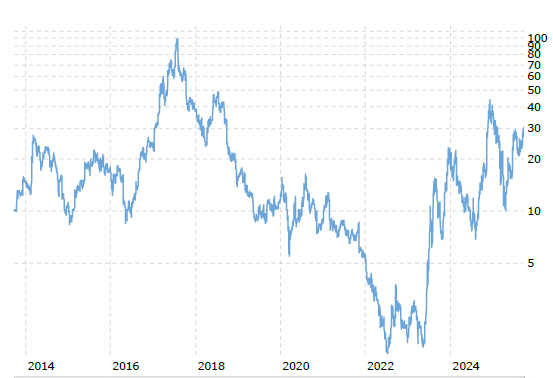

I first wrote about AAOI on September 5th of 2024 when the share price was around $13, and it was behind a paywall:

Applied Optoelectronics manufactures the connectors which convert fiber optic data signals into electronic data signals and vice versa. These transceivers are critical for the data center buildout, but are also needed for everyday cable and telecom. AAOI is not alone in this market, in fact for data centers they have about one tenth the market share and are about one fourth of the size of the market leader, Lumentum (LITE), with about 20% of the data center transceiver market. For cable and telecom, they are about one tenth the size of Sumitomo Electric (5802.T).

But Applied Opto has been approved to be a supplier for three of the five major hyperscalers. AAOI is an approved supplier for Microsoft, and while client relationships are mostly kept confidential, former Meta employees have indicated that Meta is a new customer as well. Amazon is the third potential major hyperscaler customer, as recent SEC filings show they hold AAOI warrants.

The first step to becoming a supplier to the hyperscalers is to submit their technology for testing, and receive inspectors at the manufacturing facility. Only after approval can orders be placed. AAOI’s equipment has been weighed, measured, and found to be satisfactory by the majority of the potential market. Only Google and Oracle have yet to be satisfied.

Applied Opto made big news with a supply agreement with an unnamed hyperscaler, but due to the warrant information from the SEC, it’s almost certainly Amazon. Unfortunately this supply agreement is not a firm purchase order, rather, if Amazon buys $4 billion of hardware from AAOI over a ten year period, then Amazon’s warrants in AAOI activate. This type of arrangement is not unusual; when one party is so much larger than the other that their business would dramatically increase the value of the smaller company, the larger company often demands compensation for the value added to the smaller company. To the horror of people unfamiliar with the practice, Howard Lutnick wants the US government to start doing the same. From the perspective of AAOI, a $400 million annual revenue increase would be transformational, and they would agree to give away a few warrants in exchange for it any day of the week.

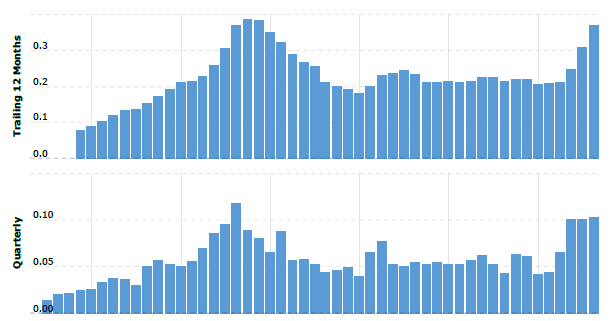

With trailing twelve month revenue of $368 million, the Amazon contract alone would double AAOI’s volume. But again, this is not a guarantee that Amazon will buy, it’s just a strong indication that they probably will.

Meanwhile, the product is already being shipped to said unnamed hyperscaler, with Q2 revenue a whopping 139% increase over the same quarter last year. To be fair, they were lapping a weak quarter, but trailing twelve month revenue is 77% higher than the same time last year, and next quarter is projected to be between $115 million and $127 million, which would be a 12% to 23% increase over last quarter’s $103 million.

AAOI Revenue:

But you will notice that this is not yet a record setting volume for AAOI, they had been close to these levels before. In 2018, they suddenly had some quality problems with their transceivers, and a major client, again unnamed but probably Amazon, suddenly stopped ordering from them. This past failure has the share price of AAOI firmly in the penalty box. Investors have a memory for major blunders, and it will take sustained performance to shake off the cloud of past failure. When so much of a company’s business is to a single customer, the loss of a supply contract can cause the stock price to collapse from $70 to $2 as happened to Applied Opto. This is probably the main reason why the options contracts are so valuable, there are put buyers hoping for a repeat of the quality failure leading to near bankruptcy.

It is, of course, impossible to predict whether or not AAOI will have another quality failure. The CEO and two directors are repeatedly buying AAOI stock, but the CFO and other directors are repeatedly selling it. Frank Knight in his 1921 book “Risk, Uncertainty, and Profit” claimed that it was bearing uncertainty which was the ultimate source of entrepreneurial profit. And that is why I am a value degen, bearing uncertainty and trying to get paid on average.

When I last wrote about AAOI, they were a $13 stock which had been approved by three out of the five hyperscalers, but quarterly revenue was only $40 million. Today they are a $26 stock with $103 million of quarterly revenue, and management is guiding for double digit growth next quarter. There is still uncertainty regarding how many orders will actually arrive from the hyperscalers, but this uncertainty is slowly lifting as the orders come in.

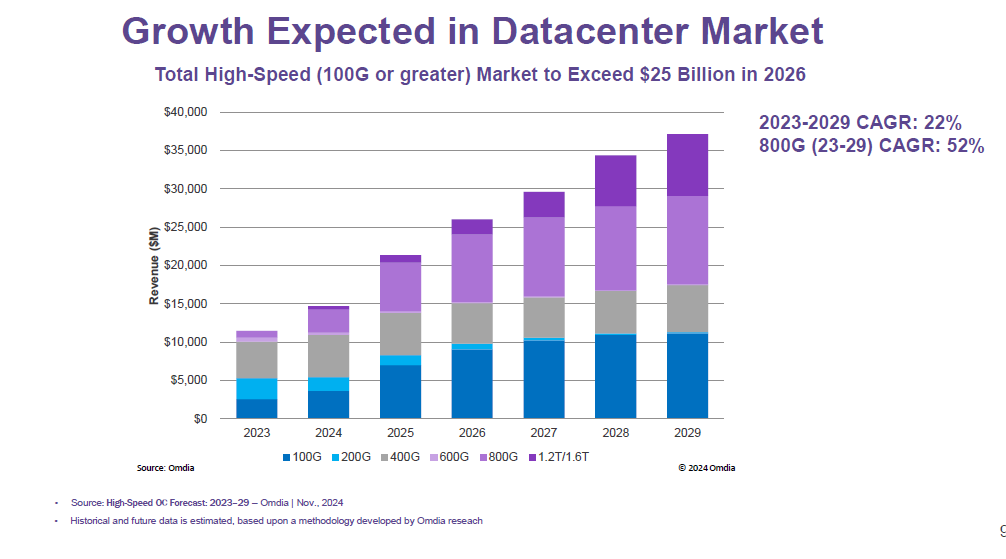

The current price to sales ratios of their peers is between 4.5x and 6.5x up from a more historical 3.5x. This increase in valuations across the board anticipates the enormous growth rate of the data center buildout, with the demand for 800G transceivers projected to be growing at 52% a year through 2029. Forecasts are for the $15 billion transceiver market to reach $25 billion in 2026, and $35 billion in 2029.

Today there are about 25 GW of data centers in the US, ground is being broken on 10 GW in 2025, and projections are for there to be 80 GW of data centers in the US by the end of 2030. It takes about 18-24 months from breaking ground until completion, longer if the site needs power generation buildout. It takes about 12 to 15 months on average from breaking ground on a data center until AAOI can log the revenue for selling transceivers. Transceivers need to be replaced every 3-5 years, with conservative operators replacing pre-emptively every 3 years before equipment failure. If the data center buildout trajectory doesn’t change before 2030, just the replacement transceivers in 2030 will be more than double the entire market in 2025.

If AAOI doesn’t take any additional market share, a 50% revenue growth rate would put 2029 revenues somewhere around $1 billion to $1.2 billion, up from $368 million. I am ignoring any potential growth in AAOI’s cable and telecom businesses. The past price to sales multiple on telecom hardware companies was 3.5x, the current 4.5x to 6.5x includes growth assumptions. An AAOI with a 3.5x price to sales multiple and $1 billion of annual sales would have a $3.5 billion market capitalization, a little more than double today’s valuation. A double over five years is not very impressive for an AI beneficiary, but this is the problem with growth traps, the multiple compression as the growth is realized makes gains humble.

However, before the 2018 quality fiasco, AAOI had 10% of the data center transceiver market, not their current 2%. Hyperscalers are hyperfocused on preventing disruptions to their extremely delicate and fragile businesses. The hyperscalers will most likely attempt to balance their suppliers to avoid over-reliance on a single vendor, which means odds are good that AAOI can climb back to a larger market share. Amazon and Meta want to funnel orders to AAOI so that Lumentum doesn’t’ grow too big for their britches like Taiwan Semi or Nvidia.

AAOI has competitive products, and they are certified to be a supplier to at least three out of five hyperscalers. At a 5% data center market share, still far below their past 10% market share, 2029 revenues would be closer to $2.5 billion, and a 3.5x price to sales ratio would imply a market capitalization of $8.75 billion, up from the current $1.6 billion. This would imply a share price of $141.38. But this does not take into account any dilution that would be necessary to expand capacity, or any share buybacks that might take place with the profits. AI seems to think that AAOI could scale up to 5% market share using only internal cash flows, although it would consume nearly all of AAOI’s cash flow.

And of course, the biggest threat is that the data center buildout slows down between now and 2030. For the moment, the large tech companies are in a knife fight for first place, ROI be damned. But if AI continues to fail to deliver returns, at some point the capital markets will force the hyperscalers to stop. But with the hyperscalers having a combined market capitalization of over $10 trillion, and combined operating cash flows of over $400 billion, the five hyperscalers could self-fund 10GW of data centers per year into perpetuity. If all they really care about is coming in first place, there is no indication that the buildout will slow down before 2030, even if in five years AI is still predominantly used for college students to cheat on homework. Maybe I haven’t been buying enough AAOI?

Applied Optoelectronics (AAOI) $26.69: $141.38 by the end of 2029

I know I am getting old, but every time I look at the datacenter buildout I remember Global Crossing and the dotcoms.

hi, i also bought this at 15$ importantly in the last two earnings calls, and apologies if i wrote this in another comment already, they talk about a large production increases with new facilities building out e.g. in last call

" As you may have heard me say at OFC, we expect to increase total production of 800G and 1.6 terabit products by 8.5x by the end of the year, and we are dedicated to achieving this goal."

these are not just 30% growth numbers but higher which makes me want to add to this a lot on the next pullback as its one of the few cheap forward P/S datacentre stocks I find.