Some Big Portfolio Events: $OPEN, $PTLO, $BW, $SPRY

Opendoor (OPEN):

The much anticipated moment has arrived, Opendoor has reclaimed its founder DNA from the custody of the temporary bureaucrats. Two original co-founders, Keith Rabois and Eric Wu will be added to the board of directors with Rabois as the Chairman. Keith Rabois is the managing director of Khosla ventures, and with 15% of OPEN owned by Masayoshi Son at Softbank and another 15% or so owned by the co-founders and some other early stage investors, I was fairly certain that he had enough votes to do whatever he wanted with the company.

If the history books remember Opendoor, they might write volumes about the incessant stock pumping by some vocal twitter accounts, but this game of thrones was always in the bag behind the scenes with big venture capital money and plenty of proxy votes already in the bag. But those stock pumpers are contributing about $40 million a day of free advertising, which has already increased the daily volume of transactions at OPEN significantly. The company is already on track to significantly beat guidance on the back of this newfound name recognition.

Rabois was always in control, and he has hand-picked a CEO to try and turn Opendoor into the network sitting on top of the $2 trillion housing market. That new CEO is Kaz Nejatian, the COO of Shopify, who also has experience as the founder of a company, Kash, a payment company startup which was acquired in 2017. Sadly, the details of the acquisition, even the name of the acquirer, were never disclosed. But the important thing is that Opendoor will be run by rapidly iterating entrepreneurs, and not managerial bureaucrats.

As a part of this return of the founders, Opendoor is selling Keith and Eric $40 million of common stock. At the current market capitalization, this a negligible amount of dilution in exchange for the incentive alignment.

Opendoor closed Wednesday’s trading at $5.86, and after the announcement in the thin volumes of after hours trading, the stock price ran up to $8.11, a 38% rally. Around 24% of the float is sold short, and that kind of a gap up will be incredibly painful. The thin after hours trading is often not indicative of where the stock will trade the next day, but if I were a short seller, I would be terrified. A tech network with a world class CEO and secular tailwinds could easily rally to many multiples of where it is trading now. The short interest was also 24% in July when the price was $0.51, so unless every hand has turned over, someone has lost 16x their initial position.

Nothing moves in a straight line, there will be pullbacks and maybe even short squeezes. I have no idea at which point I will start to trim some of my position, but I will broadcast any sales to my subscribers transparently. The daily volume of Opendoor is so large, even with 24% of the float sold short, that is less than one day’s trading volume, so an outrageous short squeeze is not my base case prediction.

This journey is just getting started, it will take years to transform the company, but seasoned tech entrepreneurs will do their best to keep a constant stream of new and exciting catalysts to keep the market entertained. A roadmap of potential changes has been laid out in detail on Twitter, some coming from Rabois, some retweeted by him, but I will spare you the details. Before this leadership transition, I had placed perhaps a 10% chance that Opendoor could successfully be the network leader, but now those odds have improved dramatically.

Babcock & Wilcox (BW):

Babcock & Wilcox signed a partnership with Denham Capital to jointly pursue coal conversion for supplying electricity to data center clients. Denham Capital is a private equity / private credit fund that has funded 10 GW of energy projects previously. With Denham Capital able to front the money to fund the conversions, and BW able to do the engineering, this has the potential to significantly drive new revenue growth over the next several years. The press release emphasized speed and time-to-power as key elements of the strategy due to the immediate needs of the hyperscalers.

A single coal conversion contract in Indiana was worth $246 million in revenue over the course of three years for a 1,160 megawatt project. With BW’s trailing twelve month revenue at around $600 million, every additional coal conversion project is a 10% revenue bump for three years.

The stock rallied from $2.01 to $2.63 on the news of the partnership, a 30% gain on the day. And BW still trades at 0.44x price to sales after that rally. The path to $5 a share and a 1x price to sales ratio could come relatively quickly.

When the surge of coal conversions takes place to power data centers and bridge the gap toward hopefully nuclear energy, BW should still benefit from the parts and service contracts to maintain those facilities. But the sun is setting on their business as their spinoff BWXT handles the boilers for nuclear power. So within the next few years, I will be eager to exit completely unless management pulls a rabbit out of their hat and reinvents themselves.

Portillo’s (PTLO):

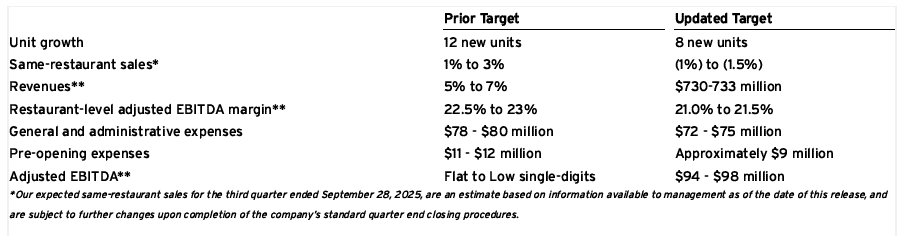

Portillo’s slashed guidance outside of the regular earnings call schedule. It appears the consumer is even weaker at the moment that anyone had anticipated. They also guided that their goal of 12 new restaurants in 2025 has been pared down to 8. The reduced capex does help the free cash flow profile, however, and management is guiding for positive free cash flow in full year 2026.

The stock sold off even further, down 5% to $6.15 a share. This brings Portillo’s to a price to sales ratio of 0.64, and a market capitalization of $463 million. When Berkshire Partners originally acquired the chain of 40 locations for $1 billion, that came out to about $25 million per location. At the current market capitalization, it comes out to $5.3 million per location. Somewhere between six and eighteen months from now, the consumer should be stabilized, and Portillo’s will be a cash cow, but the efficient market seems to only look one quarter ahead.

Meanwhile, Portillo’s found their new Chief Marketing Officer, Denise Lauer, formerly the CMO of Marco’s Pizza, a 1,200 franchise limited-service restaurant pizza chain. While at Marco’s, she was able to average 6.9% annual same restaurant sales growth, compared to 5.4% at Little Caesars, 3.1% at Pizza Hut, and 1.8% at Papa Johns over that same time period. Only Domino’s beat out Denise with 8.2% same restaurant sales growth for the two and a half year period.

One of Ms. Lauer’s focuses was on the rewards program, and Portillo’s only rolled out theirs in March. On September 22nd, she steps into the role as CMO with over 1.9 million rewards members for 86 locations, over 22,000 per location, more than four times what Chipotle has, and more than six times what McDonald’s has. I know that the consumer is stretched right now, but what is going to happen in October when 1.9 million people get a ping on their phone that they can get a free order of small fries if they order a hot Italian beef on Tuesday afternoons? Or perhaps a free milkshake with any two combo meals on Wednesday evenings? The possibilities are endless, and there is some evidence that Denise will know how to wield this awesome power.

Portillo’s has a very deep bench for an 86 restaurant company, they even got the former President and Chief Strategy Officer of Chipotle, Jack Hartung, to join their board in January. High caliber people can see the amazing opportunity and want to join a winning team. I am optimistic that their choice of CMO is going to be on top of her game. But we will find out soon enough.

ARS Pharmaceuticals (SPRY):

ARS Pharmaceuticals holds patents for Composition of Matter, Formulation and Dosage Innovations, Methods of Treatment, Delivery Devices and Systems, and International and Extended Coverage expiring in 2039 for their nasal spray delivery mechanism for epinephrine and a companion drug that facilities absorption through the nasal membrane.

Those patents are under attack by an Indian company, Lupin, who is suing to produce a generic version. ARS will contest the lawsuit, which gives them an automatic 30 month delay, whether they win or lose. So for the next two and a half years, there is no competition from generic versions of their nasal spray. Regarding whether or not they will win, that is so far outside of my competence that I can’t venture a guess, but AI seems to think that Lupin only has a 30% chance of winning. These types of lawsuits go to the generic about 45% of the time historically, but ARS has eight interlocking and very recent patents. Courts typically try to give patent holders at least some time to recoup research and development expenses, even if ARS won’t have until 2039. There is also a strong chance that ARS and Lupin settle out of court, giving Lupin permission to enter the market in 2030 instead of 2039. Lupin is a top 10 global generic manufacturer, and they are skilled in these types of lawsuits, but ARS has a big enough cash pile to fight them.

This is the danger of investing outside of my circle of competence, I had no idea that generics sue for infringement and win about 45% of the time. But even if generics are in the market, doctors often prescribe the name brand, and customers are not price sensitive if it is covered by insurance. Speaking of insurance, ARS is up to about 60% of insurers covering Neffy, with a predicted 80% insurance coverage by the end of 2025.

The second threat to ARS comes from Aquestive Therapeutics (AQST), who has a dissolving mouth film delivery mechanism for epinephrine. The FDA chose not to convene an Advisory Committee regarding AQST’s approval. This implies about an 80% chance of receiving FDA approval and entering the market as a competitor to SPRY in January of 2026.

While SPRY still has a first mover advantage, that advantage is diminishing more rapidly than anticipated. Also, in data submitted to the FDA, it appears that AQST’s Anaphylm product acts faster than Neffy. While Neffy takes about 18 minutes to work, Anaphylm works in about 12 minutes. This difference has not been verified at scale, AQST only has 20-30 real world observations compared to SPRY’s 545.

I had anticipated SPRY to take similar market share as they did when they competed against the mouth film for the Narcan market for opioid overdoses. In that competition, SPRY’s management team took 95% of the market. But in the Narcan market, the mouth film was never FDA approved due to lower efficacy, 50% absorption vs the nasal spray’s 60% absorption. It looks like SPRY might face stiffer competition this time if the mouth strip is eventually approved.

Regarding delivery, nasal spray has an advantage that the first responder doesn’t have to worry about opening the mouth of a non-cooperative patient, or worry about having their fingers bitten. But, if the patient has nasal congestion, Neffy requires a second dose about 10% of the time. The mouth strips don’t need a second dose if someone has a cold, but a relatively common aspect of anaphylactic shock is vomiting. Would doctors prescribe mouth strips over nasal spray when vomiting is a potential confounding factor? Perhaps, if Anaphylm really works six minutes faster, then maybe.

SPRY still has a tested management team that won 95% market share before, but they did it without serious competition. It looks like this battle will be more of a knife fight. So far SPRY has only taken about 5% of the epinephrine market, a slower rollout than anticipated. But they do have a head start, and this head start has already given them a 49% brand awareness. SPRY is also already licensed internationally, and AQST is farther behind outside of the US.

I still think SPRY is in a better position to take market share, but it isn’t a slam dunk at the moment. I am not impressed by AQST enough to want to hedge my position by buying both, but I am concerned about SPRY enough to want to limit my position size. If you were considering having an outrageous weight to SPRY, I don’t think that’s as wise as I did two weeks ago before the FDA’s no advisory committee ruling for AQST.

$PTLO In listening to recent investor conference and earnings call, a theme that I noticed in both is that Wall Street is trying to ruin the co like they did with Chipotle in freaking out on the short term rev. and profit over the long term value of the brand. Luckily management refuses to give in and uphold the integrity of the product and price... Chipotle is getting clowned on now for constantly raising prices and lowering quality especially quantity of meat. And despite some headwinds CFO is on point with the cards she is dealt like buying forwards on beef and exploring alternative financing for expansion a mention of sale leasback of sorts was thrown out.

patients may be indifferent to price if covered by insurance, but insurance companies and pharmacy benefits managers are NOT. except in very rare instances in which the pbm makes a special deal with the brand name. the pbm's and insurers ALWAYS insist on the generic. a doctor can appeal this, but is then required to provide evidence that the patient doesn't do as well on the generic. since anaphylaxis is a rare event, this will be hard to do. you should assume that the maker will be forced to sharply lower its price 6 months after generics appear. [the first 6 months only one generic maker is allowed and will in general also charge a high price. after 6 months if it's a significant market other generic makers will enter the market and the price plunges to a markup over the cost of manufacture.]