Schrodinger’s JAKKS, the paradox of JAKKS Pacific $JAKK

JAKKS is in a state of good and terrible superposition until you open the box.

JAKKS Pacific (JAKK) is a toy designer and manufacturer with 70% of their sales FOB, or free on board, meaning that they fill cargo containers and bring them to the port of export, and the buyer assumes liability for damaged or lost cargo from that point forward. JAKKS focuses heavily on licensing and their toys cover a wide variety of intellectual property franchises.

The toys they design and manufacture are of two major categories, the first is mostly around a $30 price point and on the shelves all year or evergreen, and the second is content-led, timing popular children’s movies and television shows such as the upcoming Moana 2 or Sonic 3.

JAKKS is somewhat of an enigma, they were founded in 1995 by Jack Friedman and Stephen Berman, with Jack Friedman as the CEO until 2010, and Stephen Berman as the CEO afterward. These last 14 years with Stephen Berman at the helm are a real hodgepodge.

Revenue:

Share price including massive dilution:

JAKKS was knocking on bankrutpcy’s door pretty hard in 2019, not only because of Covid, which for toys sounds a bit like a lame excuse anyway, but because of years of decline following the closure of Toys R Us in 2017. JAKKS also had financial troubles in 2013, when at that time they blamed the weather, among other things. Listening to management’s reasons for poor performance during this period, I am left with the conclusion that management was the reason for the poor performance.

In 2019, in a last ditch effort at survival, JAKKS underwent a restructuring, issuing a large amount of debt and preferred stock, the preferred stock having a covenant which precluded any return of capital to shareholders. Since that time JAKKS was able to refinance the debt in 2021, pay it off completely in 2023, and intended to pay off the preferred stock in 2025, but the holders of that preferred stock came to JAKKS and asked to be bought out in a hurry and JAKKS agreed at a discount. So now JAKKS is completely liberated in its capital structure, although it only has $22 million in cash remaining, but feels that while things are tight, they can manage.

So JAKKS while still under the same flailing CEO, has gone from riding the struggle bus, to suddenly performing at an incredibly high level. And the toy business operates with no moat, they have to license these intellectual properties, structural headwinds, Americans and Europeans are having more dogs than children, and cyclical headwinds, we have been in a consumer cyclical bear market for most of these years. If that change in performance, without a change in leadership, doesn’t make you scratch your head, I don’t know what will. So this is the paradox of Schrodinger’s JAKKS, when you open the box are they still the same old terrible company, or are they the new amazing company going forward?

I believe the answer to the JAKKS paradox is that Jack Friedman was the real capitalist behind the business, and when he passed away in 2010, Stephen Berman, even though he co-founded the company originally, was more of a hanger-on than a businessman. Under Berman’s leadership the business was in constant decline. Things turned around in 2019 because of the new CFO and Executive VP they hired, John Kimble. If you look at what management attributes the turnaround to, it has to do with ending unprofitable toy lines based on a total cost analysis, including warranty’s, recalls, etc. In other words, JAKKS needed somebody to put some numbers in Microsoft Excel and just do their damn job with a reasonable degree of competency.

I believe there is a good chance that JAKKS continues to execute at a high level as long as John Kimble is the EVP/CFO, and in this rare instance, I would look at the CEO stepping down, even without a succession plan, as a positive development.

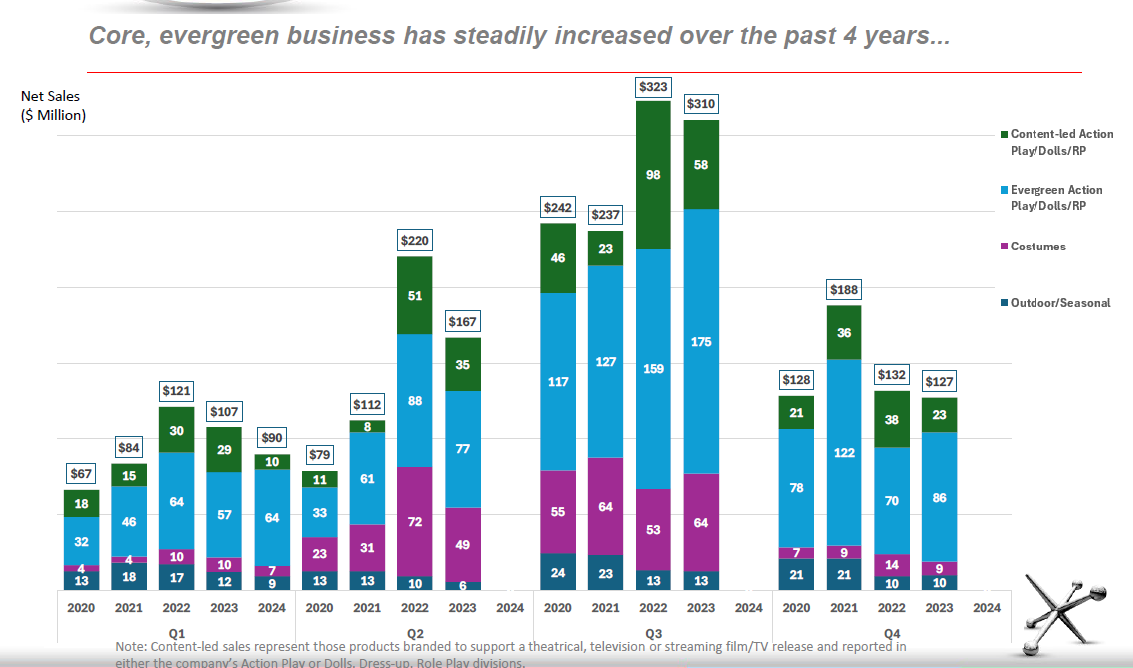

Going forward, I believe that JAKKS will benefit from cyclical and seasonal tailwinds. Cyclically, the US consumer is rebounding from falling real wages, and the next phase of the business cycle might be an expansion if we have just passed through a shallow recession masked by inflation measurements. Seasonally, Q1 is the worst quarter of the year, and management warned that Q2 this year might be rough as well. But if you break down the recent decline in revenues from the 2022 peak, and separate the cinema content-led toys as a portion of its revenue, you will notice that the evergreen toy segment has been growing steadily this whole time. The recent decline in revenues from 2022 was due to what management described as a major cinema disappointment without naming explicitly that Disney’s Wish bombed hard at the theater and failed to drive merchandise demand. The good news going forward is that Moana was an incredible success in 2016, and there are good odds that Moana 2 this year will drive their content-led business to new heights.

When I see the evergreen vs content-led business segments, it reminds me of a restaurant that expands into catering. Running a restaurant is a crummy business, but with the restaurant to cover your fixed costs, marginal revenue from catering has a very high margin. JAKKS’ marginal revenue from additional content-led sales has a 25%-30% flow through to EBITDA, and now that they are debt free, we can drop the “I” in EBITDA. So even though toys would normally strike me as a thin margin business, maybe not if you are big enough to compete over these cinema merchandising licenses.

The current share price of $17.90 might not be the trough with bad Q2 earnings likely ahead, but retailers will buy aggressively ahead of the Moana 2 release in November, so there are good odds we see a very strong Q3. For the longer run, as long as JAKKS continues to execute well, now that they have someone on the staff who actually knows how to use a spreadsheet, there is no reason they can’t trade up to a price to sales ratio of 1, with growing revenue, and start returning capital to shareholders. At a current market capitalization of $193 million, JAKKS could over the course of three to five years reach a new $1 billion annual revenue peak, trade at a price to sales ratio of 1, and generate a 5x return from here.

Going forward there is also a strong probability of M&A activity, just as JAKKS did under Jack Friedman, because John Kimble was the head of M&A at Mattel. Here’s hoping the CEO stays happy golfing while the EVP/CFO does his job for him.

I am disappointed in the lack of insider buying, but 80% of c-suite executives never buy stock in their own company, they are employees in their minds. In this case that applies even to the co-founder Stephen Berman. John Kimble did spend a couple of years co-founding a startup, and this experience might be why his attitude on earnings calls is sympathetic to shareholders.

Despite a lot of one-off events last quarter, he didn’t dump them into an ad hoc adjusted EBITDA metric and treat investors like idiots. If I can’t have a capitalist in charge, having an entrepreneur-adjacent EVP/CFO who has courtesy and respect for shareholders is not a bad second best. I would immediately liquidate the position on news that John Kimble is no longer with JAKKS.

Agree with the Berman/Kimble read. Think market has been sleeping on next quarters re Moana 2, Sonic 3, even potentially Dog Man, so I have a large stake in the co. However, seems like potential tariffs from a new admin are an overhang, and a real risk.

too hard pile.