Ro Ro Ro Your Boat: Höegh Autoliners $HOEGF

Probably Not a Value Trap

Welcome back to the “Probably Not a Value Trap” series where I discuss businesses with a 10%+ dividend yield which I believe probably won’t get cut and why, but don’t come after me on Twitter if they do.

This is also a part of the “Riddle of Steel” series where we focus on different shipping sectors. While I personally prefer gold, oil, and land to mitigate inflationary risks, another popular strategy is to own “embedded energy” purchased at a discount to replacement cost. The pitfalls of owning embedded energy to combat inflation were laid out by Warren Buffett in 1977 in his article “How inflation swindles the equity investor.” When you go to replace that ship at the end of its life, you will be doing so at much higher costs, but the money you earned in the past was at lower nominal prices. To mitigate this problem, I believe it is important to use a healthy amount of debt so that the real value of the nominally fixed debt evaporates.

How Inflation Swindles the Equity Investor | Holland Advisors

Special thanks to

for bringing to my attention Höegh Autoliners (HEOGF), a shipping company that specializes in RoRo, “Roll on Roll off” automobile transport ships.The best thing about shipping is that the supply of new ships can be seen as the orderbooks of shipyards are collected by research firms and sold to equity investors. At the moment the shipyards are full of cargo containerships and LNG ships. At the other end of the spectrum are deepwater drillships where so many shipyards went bankrupt from abandoned rigs after 2014, that shipyards require as much as 60% down to be convinced to take the work.

In the muddling middle of the orderbook are tankers, chemical tankers, dry bulk, and RoRo.

While the orderbook is not as restrictive on supply as I would like, there is an added demand force affecting the sector, electric vehicles. Battery fires from lithium ion batteries, while rare, given the law of large numbers on a full RoRo, are a major hazard. At least two RoRo’s have already been destroyed this way. In mitigation, shippers are spacing vehicles with lithium batteries farther apart in the ship to avoid a chain reaction. This means that more RoRo’s are needed to carry hybrids and EVs than internal combustion vehicles.

Report: Volkswagen Sued by MOL for the Loss of Felicity Ace Car Carrier

That excess demand for RoRo’s could dry up if there is a technology shift away from lithium ion batteries and toward a different technology. While China is making large advancements in sodium ion battery production, these sorts of changes typically take years.

Also, the excess demand for ton miles from the Houthis redirecting ship traffic away from the Suez canal could potentially reverse. It is possible that a new Trump administration, in an effort to go down in history as the great dealmaker, would try once again to have peace in the Middle East. It is also possible that a new Harris administration could embolden the Arabs to keep up pressure on Israel for many years.

Due to the near term risk of falling day rates from peace breaking out, I am reluctant to grab on to any shipping stock with both hands at the moment. But the structural tailwind for RoRo’s from lithium batteries is compelling for the medium term, with the longer term having the risk of the shift away from lithium ion and to some safer technology eventually crashing the market.

But now for Höegh specifically, Höegh Autoliners is 35% owned and controlled by two of the grandsons of the original founder Leif and Morton Høegh, with another 5% owned by Emanuele Grimaldi of the Grimaldi Group. It’s always important to know that bureaucrats with agency conflicts aren’t making decisions that keep capital away from shareholders.

Speaking of returning capital to shareholders, about nine months ago management implemented a new capital allocation policy. Going forward 100% of free cash flow will be paid out in dividends. Last quarter, Höegh made $127 million in adjusted EBITDA, and then immediately paid out $127 million in dividends. Not bad for a $2.33 billion market cap company. At that run rate, the dividend yield going forward would be over 20%.

Management is guiding for Q3 to be similar to Q2, but the natural question to ask is are those sorts of profits stable? When transportation costs were rising due to the effect of the Houthis on the market, Höegh pursued spot rates as much as possible. Now that rates are high, the strategy has shifted to locking in contracts of as long a term as possible. Currently 75% of the fleet is contracted out giving the whole fleet a weighted average of 4.3 years. That would indicate to me that Höegh is probably not a value trap until at least after 2028, not including any new contracts that management can close in the meantime. I believe that this is precisely the correct strategy, no sense being too greedy.

Höegh isn’t exactly a deep value stock with a market capitalization of almost exactly the amount that management estimates the current resale value of the ships would be today. However, value stocks typically have problems which are responsible for the mispricing, and as of today, I can’t find any problems with Höegh. It’s full price, but it’s a good business.

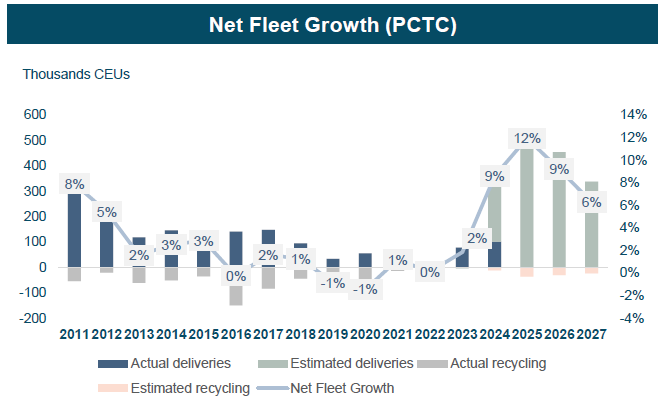

Looking beyond 2028, the orderbook for RoRo’s is more aggressive than I would like, with 216 newbuilds coming online in the next four years, that would represent 41% of the current fleet. To counterbalance that, however, is the projected increase in Chinese exports of automobiles. As a generalist, it’s hard to know which force will overpower the other, but given the contract backlog, it’s not a terrible idea to buy some Höegh, let the dividend return your initial risk capital, and then re-evalute the state of the RoRo market at some future date.

So with Höegh you have a nice little family business in an overlooked corner of the market, able to provide a handsome income yield for at least the next five years. Somewhere along the way, we will discover which force wins out, Chinese auto exports, or the newbuild backlog. If the forces are somewhat balanced, then Höegh might maintain a greater than 10% dividend for a very long while indeed. For me, I don’t mind giving them five years to enjoy their fixed contracts, and then see what inflation does to the value of their embedded energy assets. But I would size the position small in hopes of a better buying opportunity on a pullback.

A guest post by

|

Thanks for the shout out! @40sprof gave me the idea.

I’m liking your work more and more with all the different ideas.

I own a small position in Seatrium along with Marco Polo as well as looking at more ship builders…