Razorblades Up In Smoke; Traeger Grills $COOK

As the worst performing sector year to date, I have been going sifting through consumer discretionary companies. And I had found two companies over the weekend that I wanted to write about for this week. I chose to write about American Eagle Outfitters (AEO) for Monday’s writeup, and Trager Grills (COOK) for Tuesday’s.

As luck would have it, Traeger Grills rallied 26% on Monday, before I could get my article out. I still think it has plenty of room left to run, but short term traders are quick to take profits, and I have no opinion on where the stock price will go in the next few days. I hope we all get a chance to buy it a bit cheaper, but we may not. Over the longer run, Traeger looks like an undervalued company, and the CEO, Jeremy Andrus, agrees, having spent around $3 million on insider purchases between April 3rd and June 4th.

The last company I did a writeup on because corporate officers were engaging in insider buying so aggressively was Newell Brands (NWL). That story has not come to fruition yet, and it has been painful along the way, but I have a suspicion that consumer discretionary is due for a bounce.

Traeger doesn’t have a complicated business model, after stretching myself to understand a tech or software company, it’s nice to analyze an easy business. But Traeger does have an edge to try and eke out some profitability in the thin margin world of consumer durable goods. Traeger sells their grills in several places, but Costco drives a lot of revenue. The good thing about selling at Costco is the access to legions of upper-middle class customers, but the bad thing is that Costco plays hardball, to get in their store, margins have to be thin.

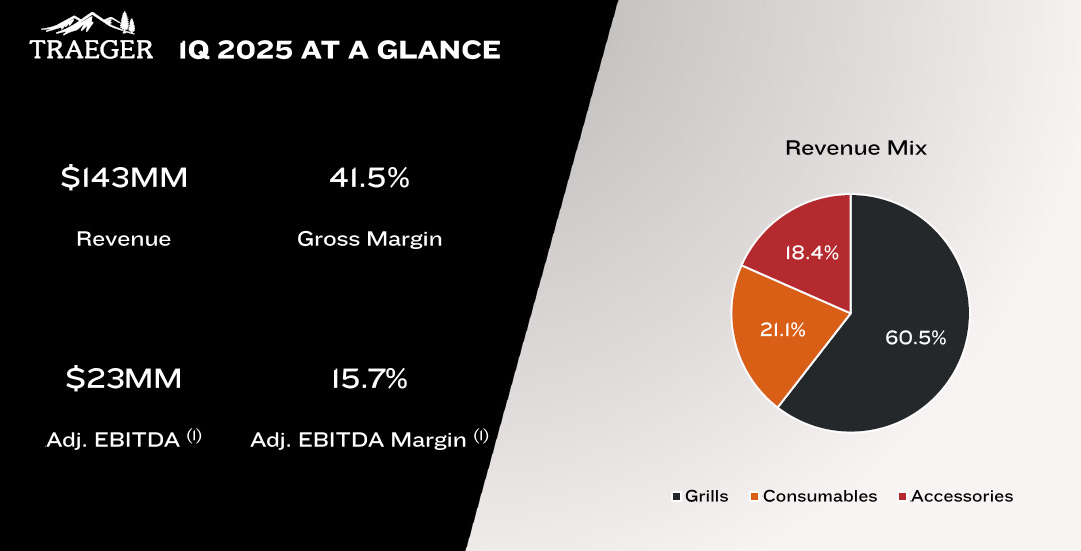

Traeger’s innovation is to sell grills that use wood pellets to give a smokey flavor, and those wood pellets, specifically designed to work with the grill, can be purchased through Traeger, where margins are significantly better than at Costco. It’s the razor and razorblade business model, but in a modest way. Grills still account for 60% of revenue, and consumables only account for 21% of revenue, but put that in perspective for a company with $600 million of revenue for the last twelve months. It means that Traeger sells about $120 million of wood pellets, barbeque sauces, and rubs in a year. The EBITDA for 2024 was only about $48 million, while the company doesn’t break down margins per segment, I don’t think it’s farfetched to think that wood pellets are 21% of revenue, and approximately 100% of profits.

Traeger Grills isn’t the sexiest business of all time, but in the world of consumer durables where competition drives profitability toward zero, and you either give away your profits to Google for advertising or to Costco for the floor space, they have managed to secure a nice little niche for themselves.

It probably wouldn’t be so cheap if it didn’t have a hearty helping of debt attached to it. Traeger has $403 million of long term debt at SOFR +3% due in June of 2028. For the last two years, management has been focusing on reducing that debt burden, and they have put a dent in it, total liabilities are down by about $50 million over the last two years. It’s a relatively modest result for the last two years, but taken in the context of the greatest relative interest rate increase in human history, I see it as a very good performance.

In 2021, before the interest rate hikes, revenue was about 25% higher, and EBITDA was double. Traeger has operating leverage to benefit the next time the cycle is in their favor, and as I wrote in yesterday’s article, it isn’t unreasonable to think that the cycle might be in their favor within the next 18 months.

A return to a price to sale ratio of 1.0x, and a return to peak revenues of $780 million, would bring Traeger to a share price of $5.96. It reached right around that price in August of 2023, but it didn’t stay there for long. Traeger hasn’t been public for long, they had their IPO in July of 2021, right at the top of the zero interest rate market. At the IPO, shares reached an absurd valuation, which I don’t expect the stock to reach again any time soon. Traeger has some claims to proprietary technology and Internet of Things compatibility, but come on, it’s a grill. The real story is that the smoker burns over one pound of pellets an hour, and Traeger sells the pellets for $1 a pound. So these grills cost over $1 an hour to operate.

I obviously wish I had written about Traeger for Monday, and when the short term swing traders exit, the stock price might fall a bit. But there is room for COOK to double or triple on the next consumer cyclical boom. The biggest risk longer term would be if the shares held by private equity were to be liquidated. It would take years of suppressing the share price for private equity to achieve a full exit, and it wouldn’t be fun to be a shareholder in the meanwhile, unless of course management starts returning capital to shareholders through buybacks at low valuations. Capital allocation is all about debt retirement for now, but things can change over the next couple of years.

Any input cost risk (higher prices on things like wood chips or plastic etc.) for companies like NWL and COOK with a potential recession on the horizon?