Razorblades in the Oilfields: Forum Energy Technologies $FET

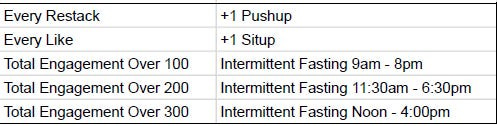

For the last article, I owe you 4 pushups and 32 sit ups. As a quick reminder, for the month of January, I will do 1 pushup for every restack and 1 sit up for every like that each writeup receives. If the combined number of likes and restacks reaches certain milestones, it will create a narrowing window of intermittent fasting.

Update 1/20/2025

It came to my attention that one of my subscribers has also written about FET. He had originally posted the idea to me in the chat, and I did not know he also had a substack and had written about it. Thank you

After my last writeup on Mattr Corp (MATR.TO), I was inundated with requests to take a look at Forum Energy Technology (FET). It fits in line with the prior thesis that the increase in natural gas export terminals as well as the demand for electricity from the data center buildout, should drive increased volumes of oil and natural gas drilling, even if the prices of those hydrocarbons don’t behave as predicted. FET produces consumable hardware that is needed for drilling and fracking, they are the replacement razor blade business model in the shale basin, but they also have exposure to offshore drilling as well. It’s hard to think of a better slice of the energy cake. Comparing them to ProFrac Holdings (ACDC), the attraction of ACDC is the vertical integration to create the low cost provider that will survive a cyclical downturn, but ACDC is like a full service barber shop while FET is like Harry’s Dollar Shave Club. Other things equal, the Dollar Shave Club business model has the potential to provide higher returns.

With a recent sale-leaseback, FET positions itself not just as a replacement razor blade business, but as a capital light one at that. This combination of characteristics is a highly desirable business model. When a highly desirable business model is cheap, 0.29x price to sales and 0.53x price to book, I have to ask why. In the oil price downturn after 2014, FET found itself overleveraged after aggressive acquisitions. In order to survive, they sold off a lot of non-core assets, and kept what they claim is the better, higher margin businesses. While starting to recover in 2018, the Covid crisis hit them hard again. These two downturns burned through about $1 billion of FET’s tangible book value. It’s completely understandable if the market is slow to trust FET again after struggling for so long. But the recent price action tells me that the market is starting to believe.

Revenues:

Market Capitalization:

Share Price:

FET does have competition, but in several categories they are one out of just three suppliers globally. In order to grow their market share, FET has a specific strategy. The first part is to focus on niche markets, this is highlighted by their recent acquisition of Variperm, the leading provider of sand and flow control products for the Canadian tar sands market. By acquiring the established dominant provider in a niche market, and by maintaining a technological advantage by innovating and patenting those innovations to create barriers to entry, FET believes they can create a business with resilient cash flow.

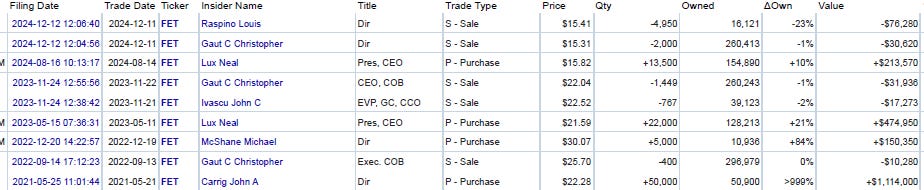

Their competitive position will have to be defended through innovation and acquisitions, which is why it is encouraging that their CEO, Neal Lux, was the founder of one of their acquired subsidiaries, Global Tubing. The founder and former CEO of FET, Chris Gout, is the current Chairman of the Board. Having the founders in the management team and having a history of creating innovative products and patents is a positive sign. Upon becoming the CEO, Neal Lux has engaged in a couple of insider purchases, although the rest of the insider behavior is very mixed. Regarding incentive alignment, between Neal and Chris, there is only about a 3% ownership of FET. This contrasts with ACDC where the founding family owns over 70%, so much that rumors of them taking it private weigh on the stock price.

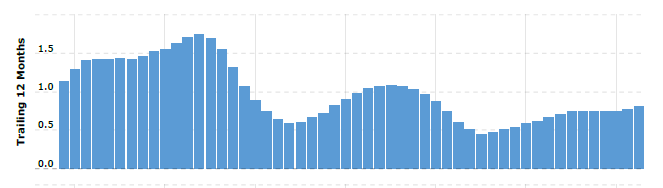

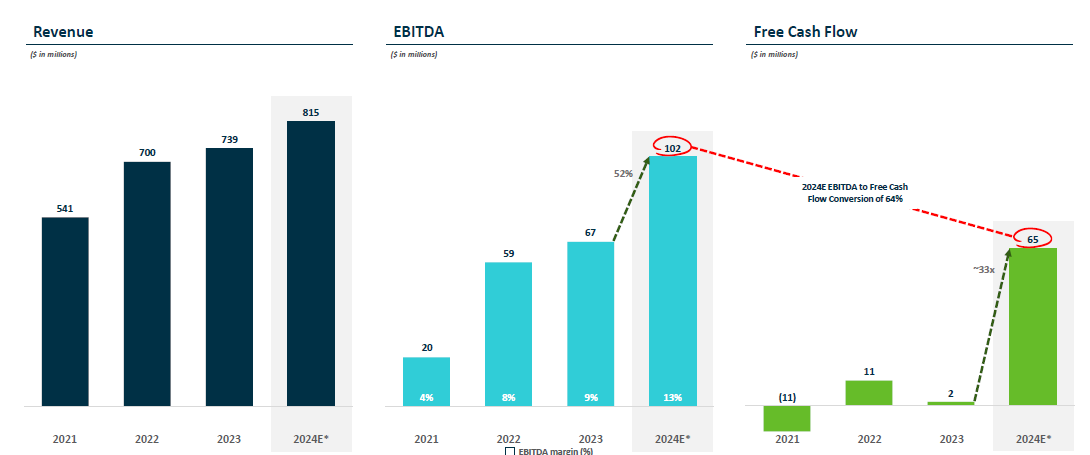

If I were to pick out one advantage of Forum Energy Technology that would be a deciding factor of why I would want to add them to the portfolio, it would be the relationship between their revenues and the recent phenomenon of expanding lateral drilling. Over time, fracking has undergone a transformation toward three-mile laterals and octopus wells. This has led to a falling rig count and relatively stable oil production. But FET doesn’t make their money on the number of rigs deployed, they make their money on how many consumables are used while drilling out those laterals. Look at how FET’s revenues are growing in 2023 and 2024 despite a falling rig count.

Baker Hughes North American Rig Count:

FET: Revenue, EBITDA, Cash Flow

Management is guiding for free cash flow of $50 million to $60 million for 2025. This projection is based on flat performance, while most of us are predicting a rebound in activity given the rising natural gas price. It’s always a good sign when management gives conservative guidance. Management also refinanced their long term debt, extending maturities to 2029 on their $100 million secured term loan at 10.5%. FET still has about $60 million of 9% convertible debt outstanding as well that matures in August of 2025, and has a conversion price of around $27. Those interest rates are hardly attractive, and management is not focused on paying it down, instead, they are focused on a pipeline of what they believe are attractive acquisitions. If this does turn out to be the upswing in the drilling cycle, this aggressive strategy will pay off. But if we find ourselves in a drilling downturn, well, this is how they landed themselves in trouble in 2014.

With a current market capitalization of $234 million, and 2025 projected free cash flow of $50 to $60 million, you would be buying FET at between 21% to 25% free cash flow yield. However, management separately guided toward around a 15% annual increase in revenues. The increase in EBITDA and Cash Flow could be beyond that, but it would require further margin expansion, which is a priority for FET, but they gave no guidance toward it. With a 15% annual revenue growth, the current market capitalization is closer to a 28% to 33% 2026 free cash flow yield. This 15% revenue growth would be based on the current trend of falling rig counts but expanded laterals, and is not relying on a rebound in shale activity due to new natural gas export terminals or the rising electricity demand. It also does not take into account margin expansion, which while not without an upper limit, the management team will probably be able to beat their current 13%.

The recent price runup was fierce, and while FET is undervalued here, there are good odds of some price retracement downward in the short term. This isn’t preventing me from starting a position on Tuesday morning when the market opens, but I expect the price to fall some, especially if next earnings call misses due to the extreme caution that management warned about in the US shale basins given the uncertainty surrounding new policies from the incoming administration. I don’t have the infographic handy, but the recent frack fleet data supported that drilling activity has been falling rapidly in the last few weeks.

When the market believed in FET, they traded at a price to sales ratio of 2.0x, as well as price to book ratio of 2.0x. Now that they are more capital light, those ratios have diverged, but FET has room for a multiple rerating of between 4x and 8x. However, management is likely to deter that multiple from rerating fully by engaging in aggressive acquisitions. I could see FET ending 2026 with over $1 billion in revenue, and trading at a price to sales multiple of between 1.0x and 1.5x. From the current share price, that would be a 4x to 6x. While FET does have an announced share buyback program it is of about the same size as their convertible debt due in August, so I presume the share count will be a wash.

I do like FET, and I am not deterred by the recent stock price runup from $14 to $19. It still has a long way to go. Would I sell some of my ACDC in order to buy some FET? That’s a tough question. I am not seeking capital light businesses to the same extent that some other investors are. In order to reap the benefit of the multiple expansion from being a capital light business, management would probably have to calm down on their aggressive acquisition goals, and that was not their guidance. But after the recent runup of ACDC from $5.50 to $9.00, FET is cheaper by a few metrics. I plan to start a small position in FET, and with any luck, next quarter’s earnings call will give me a dip to buy.

Forum Energy Technology (FET) $19.09: $81.58 by end of year 2026

Good write up you have a new subscriber - appreciate the attention, have owned and followed FET since 2020.

I'd just clarify that the only debt outstanding is the $100MM notes just issued and the line of credit balance, everything else was cleared with the closing of the new notes (they paid off the 8/2025 and a variperm seller note) - net debt was $199 at 9/30, $179 post sale/leaseback.

I think an important part of this story is why did the stock go from low $30s in early 2023 to $14 this year despite EBITDA 2.5x and op CF from (17MM) in 2022 to +60-70MM in 2024?

The conversion of ~50% of their notes triggered right at the end of 2022, this put an extra ~4.5mm shares on the market, the variperm transaction created another 2 million. You can look through the filings but the largest PE holder sold 830k shares in Q4 2023 2H 2024 volume was nearly 2x 1H 2024 volume), large bond holders sold throughout 2023 & 2024.

The stock has been fighting exit liquidity which is not fundamentally driven. It feels like 12/31/2024 was a turning point. Anyone selling to clear shares from YE statements is gone (it seems).

Agreed on all your analysis - setting the floor here into what is an improving macro environment driven by power demand is the perfect multi-year setup as OFS activity troughs. Thanks

Seen you have a mention on Yahoo Finance. Hopefully it brings you more subscribers and we can still get a position in FET now. haha.

https://finance.yahoo.com/news/forum-energy-technologies-inc-fet-172723238.html