Milling About with Deep Value Part II: UNIFI, Inc $UFI

On June 3rd of this year, I wrote about Rayonier Advanced Materials (RYAM), which subsequently doubled, and I recommended selling, because if you double your money on something as ugly as a papermill, get out while the getting is good. My opening from that writeup still applies:

“As a value investor and as a bit of a contrarian, I have to admit I occasionally get interested when a cyclical industry is aggressively not sexy. Why is the stock cheap? Nobody loves it until that part of the cycle when the earnings peak.”

Milling About with Deep Value: Rayonier Advanced Materials $RYAM, Mativ Holdings $MATV, and Magnera $MAGN

As a value investor and as a bit of a contrarian, I have to admit I occasionally get interested when a cyclical industry is aggressively not sexy. Why is the stock cheap? Nobody loves it until that part of the cycle when the earnings peak.

Well, courtesy of Lone Wolf Investing on Twitter, I have another aggressively not sexy mill for you, but instead of a paper mill, it’s a textile mill. Allow me to introduce UNIFI, Inc (UFI), which is similar to RYAM in so many ways. In order to survive in a terrible industry and a high cost jurisdiction, they embrace innovation. UFI’s big innovative product is REPREVE, a polyester made from recycled bottles.

While ESG is somewhat in retreat, the world of fashion is an interesting space where the cost of materials can be disconnected from the sales price. I suspect that these recycled textiles will maintain traction and return UFI to profitability when their cycle turns again. Many large brands still have targets focusing on recycled polyester, and have not rolled them back. Time will tell if those goals are abandoned or not.

Brands using REPREVE:

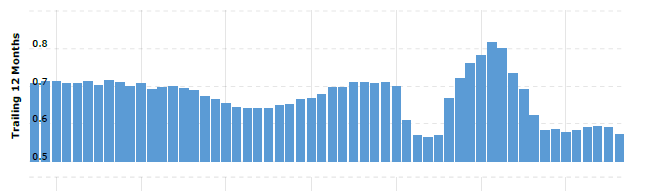

Textile Mills have suffered under recent cyclicality, but odds are good that things start to turn in their favor. You can see from UFI’s revenues below, they had an enormous Covid bullwhip, where retailers built up excess inventory after they suffered from the supply chain crisis. The subsequent destocking period has been a textile depression, which management believed was ending in 2025, up until Liberation Day and the Trump tariffs placed a layer of uncertainty on the cyclical textile rebound.

UFI Revenue:

But I believe that the rebound is delayed, not destroyed. When the tariff uncertainty is gone and business can get back to normal, retailers will have to restock what they have been destocking, and UFI should have a day in the sun again. Recently Scott Bessent gave an interview to the Financial Times where he indicated that this uncertainty was both intentional, and temporary. Plus, whatever market share UFI may have lost to lower cost Indian competitors, those competitors now have to compete against tariffs while UFI has enormous US manufacturing capacity.

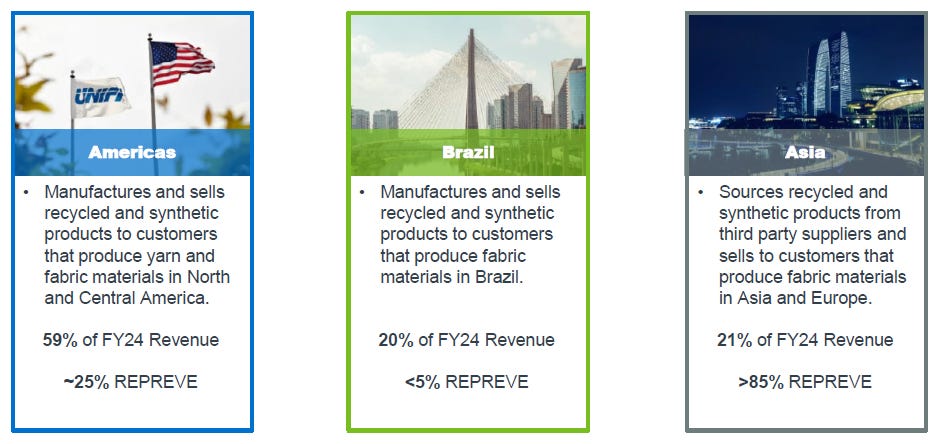

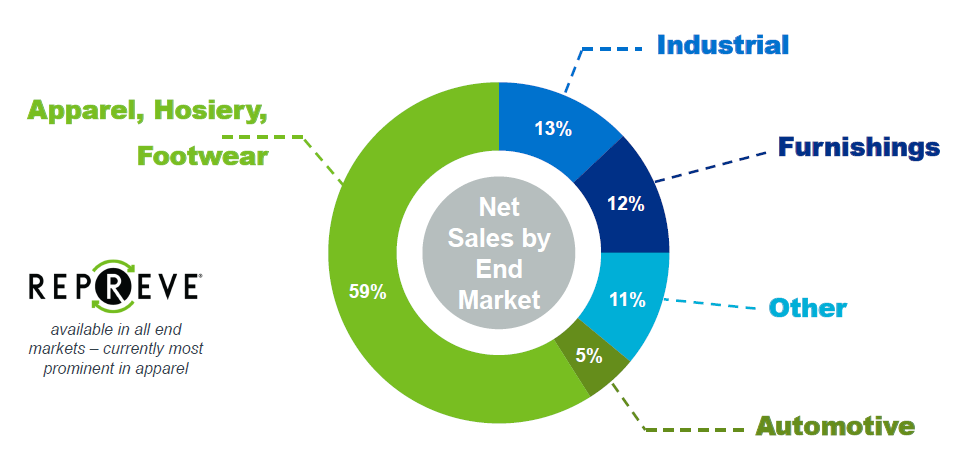

The US is almost 60% of UFI’s revenue, and their recycled products haven’t fully penetrated the market here yet.

Apparel is the majority of UFI’s end market, but the margins are better in the smaller market segments. Interest rate cyclicality is affecting automotive demand and furniture demand, while tariff uncertainty and a weak consumer are affecting apparel demand. All of those headwinds could flip in 2026, and management is predicting at least 10% revenue growth next year.

During this down part of their cycle, UFI has dramatically reduced capex, and even recently closed and sold an underutilized manufacturing facility in Madison, North Carolina. Production was shifted partially to the Yadkinville, North Carolina facility, and partially to El Salvador. Management believes that the sale of the Madison facility should lead to about $20 million of annual cost savings, due to the facility’s high cost structure.

This asset sale retired over $40 million of debt, leaving UFI at an $80 million market capitalization, with $95 million of long term debt, and about $165 million of working capital, mostly inventory. Trailing twelve month revenues were $571 million, but in a normalized environment, were usually closer to $700 million. Trailing twelve month GAAP net income was a $20 million loss, but if management is accurate with a $20 million annual cost savings, then 2026 should be breakeven at worst. UFI was capable in the past of earning over $30 million annually of net income, but after cost cutting initiatives, that number could end up being higher in the next cyclical boom.

Unlike RYAM, which was at best case probably better than a double but worse than a triple, UFI has the potential to be a five bagger. From 2013 to 2018, UFI traded at a price to sales ratio of 1.0x, but today sits at 0.14x. A return to past valuations and past revenues would imply a return to 2013 to 2018 price levels, which ranged between $22 and $35. That’s not a bad potential upside for a company that currently trades at $4.46.

UFI Stock Price:

The risks to UFI would include continued loss of market share to Indian competitors, continued cyclical weakness for US apparel demand, an abandonment of ESG and recycled polyester demand, and all the usual vicissitudes of potential mismanagement or the business environment. With UFI not being too terribly levered, they probably can survive to get to the other side of this current cycle, especially when we have visibility to rate cuts and a new Fed Chair. Is Trump going to stop cutting rates before we have a new auto boom to grease the palms of the United Auto Workers Union? I don’t think so.

This particular down cycle has been ongoing so long that the insider buying took place a couple of years ago. I maintain my position that insiders know when their company is cheap, but they often have no clue about the timing for when their company will recover. In 2023, there were inside purchases from the CEO, CFO, and General Counsel, as well as significant purchases from a director and 13.7% owner, Ken Langone, a co-founder of Home Depot.

On one hand, Mr. Langone’s inside purchase of 500,000 shares accounted for 2.7% of shares outstanding, and increased his ownership stake by 25%. On the other hand, he is worth over $8 billion, so a purchase of $2.875 million might be pocket change to him. But Langone has a business philosophy similar to Warren Buffett’s, centered around investing alongside good people of good character. This is a pretty strong green flag regarding the quality of management.

Either way, Ken Langone’s presence on the board and continued insider purchases should provide some modest bit of comfort. That and a relatively healthy balance sheet should instill confidence that however long it takes, UNIFI should survive to see the other side of this cycle, and when it does, it could be a five bagger.

UNIFI, Inc (UFI) $4.46: $22 by the end of 2028

Here is a recent interview with Ken Langone for your pleasure:

Sepatown! Love this one!

Do CULP next! (Especially now that you move markets and it trades 20k shares a day📈)

Nice pick!…had started a small position last week.