"I don't like sand. It's coarse and rough and irritating and it gets everywhere" - Anakin Skywalker: Smart Sand $SND, Atlas Energy Solutions $AESI, and Alpine Silica $ACDC

As rig counts and frac fleet counts fall, but well laterals and perforating charge density keep growing, another possible way to invest in the shale revolution is to own the sand, or proppant in their jargon. The cracks in the shale are wedged open by a very specific type of sand, and there are several public companies that own and operate the mines and the logistics for delivery. One was even acquired last fall by Apollo, US Silica was taken private at 1.2x 2023 revenue.

The Covid lockdowns were particularly rough on the sand miners, it’s a thin margin business, but usually a stable one. Several of the public sand miners went through bankruptcy and have since re-emerged as private entities or have been acquired. All that remains are Atlas Energy Solutions (AESI), Smart Sand (SND), and possibly soon Alpine Silica, the proppant spinoff of ProFrac Holdings (ACDC).

For full year 2024, AESI had revenues of $1.1 billion and adjusted EBITDA of $288 million, or 26% EBITDA margins. For SND, revenues were $311 million, and adjusted EBITDA was $38.8 million, or 12.4% EBITDA margins, and Alpine Silica had $247 million in 2024 revenue and $86 million of adjusted EBITDA, or 35% EBITDA margins. I always take adjusted EBITDA with a grain of sand, or salt, but in comparing across the three companies, let them have their accounting gimmicks. The margins on Alpine Silica might be somewhat fictional, ProFrac Holdings sells an integrated solution, and internal prices might not be indicative of what could be charged to the open market after a spinoff. But, in 2023 70% of Alpine Silica sales were to external unaffiliated companies, so the numbers might not be that squishy.

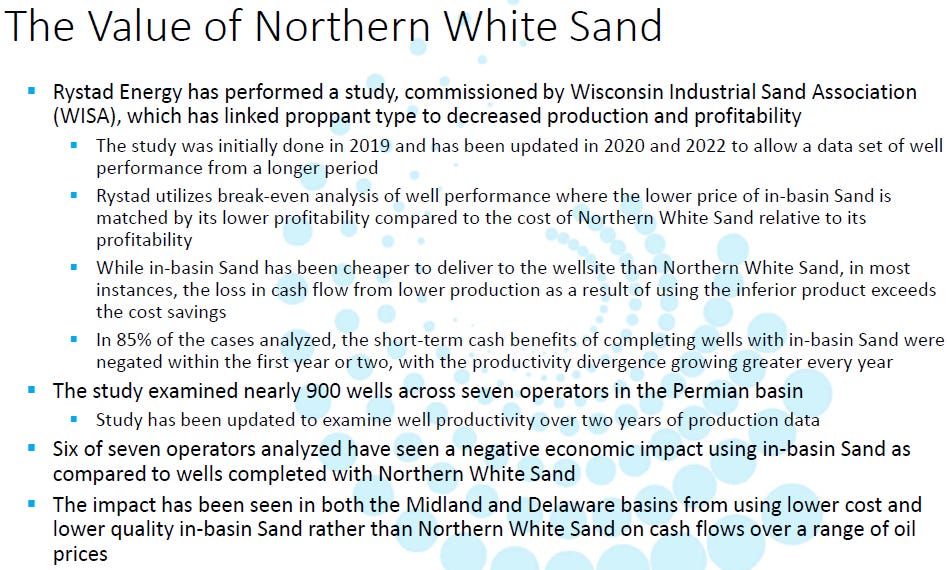

The standout for margins is SND, and the reason is that their sand mines are in Wisconsin and Illinois, and incur significant transportation costs to reach the shale basins. Both AESI and Alpine Silica produce proppant from mines that are within the basin, dramatically lowering logistics costs. The in-basin sand isn’t of as high a quality as the premium Northern White that Smart Sand produces, but it appears that the customers are somewhat indifferent for now. Northern White does fetch a premium price, but sand is heavy and difficult to transport. It’s always possible that further innovation in the shale patch could lead to stricter sand requirements, but for now the quality doesn’t seem to matter enough for SND’s profitability.

This difference in margins, and possibly the difference in size as well, leads to a huge valuation gap between AESI and SND. AESI trades at 1.67x revenues, and was at 2.3x revenues as recently as February, while SND trades at 0.3x revenues, and reached a prior peak of 1.2x revenues in 2021. It’s hard to say where Alpine Silica would trade after a spinoff as it would get the size penalty for being a small cap stock, but it is still a much higher margin business than SND. It wouldn’t be unreasonable to think that Alpine Silica could trade at 1.2x sales, the price at which Apollo took US Silica private. US Silica had EBITDA margins of around 26%, the same as AESI, but less than Alpine Silica, if the internal numbers are accurate.

With SND trading so cheaply, the possibility emerges that in the next shale oil boom, proppant prices could surge and give SND some operating leverage over their higher margin competitors. But it is unlikely that a sand shortage could squeeze prices high enough and for long enough to make a big difference. I had heard that in 2022 even sand became hard to come by, and while it did lead to a short term squeeze in proppant prices, it didn’t last long enough to have much of an impact on earnings for sand miners. Instead we see a steady march higher from $11.50 a ton in 2020 to $22 a ton in 2024 driven by the ever increasing need for more sand as laterals get longer and longer. The brief spike to $55 a ton in 2022 was less impactful than the full year at higher volumes of 2023 at stable higher average prices of over $21 a ton.

So without much hope of the benefit of operating leverage, is SND still underpriced despite the thinner margins? At current prices, SND trades at an Enterprise Value to EBITDA of 3.3x. For AESI that number is 7.7x. Taking leverage and margins into account, SND has room to double to catch up to AESI. Or AESI still has room to get cut in half to catch down to SND.

While the recent share price crash of AESI from $24 to $14 looks like a buyable dip, I’m not entirely certain that the multiple has hit rock bottom yet. AESI did something recently that the market doesn’t like, they did a scope expanding acquisition. In January of this year, AESI acquired a power generation business to expand their offerings in the shale basin. We saw from Kodiak Gas Services (KGS) that this power gen business can fetch high multiples of its own, but companies can fall under a conglomerate discount. The conglomerate discount never made much sense to me, but it is a force in the marketplace that I don’t ignore. It is worth noting that AESI’s share price didn’t fall on the announcement of the acquisition, it only fell later in February when the tariff uncertainty hammer beat down every small cap stock.

So what will happen next for AESI, will it trade down to a price to sales ratio of 1.2x because the market hates diseconomies or scope, or will it bounce back to 2.0x price to sales because of their aggressive growth and stable dividend? I don’t have an answer for that. But I do believe that Atlas Energy Solutions is a well-run company with a long runway of organic growth ahead of it. For 2025, management is guiding toward selling 25 million tons of sand as opposed to 2024’s 20 million tons. And that should be on top of rising proppant prices, leading to a more than 25% increase in revenues year over year.

Beyond that, AESI is an innovative company, they just finished a 42 mile conveyor belt, the Dune Express, the second largest conveyor belt in North America, and the first to deliver sand in the Delaware basin. They are also rolling out a fleet of autonomous trucks to deliver sand remotely, and they innovated a multi trailer system where a single driver can deliver 105 tons at a time instead of the standard 23.5 tons. Since upwards of 70% of trucking costs are labor, all of this points to lower costs, which should be a driver of expanding margins. And the 7% dividend yield should provide some share price support.

Regarding capital allocation, AESI is committed to maintaining a growing dividend, and they have authorized share buybacks in the past, but they are on the lookout for more acquisitions. With the recent power generation business acquisition, about 20% of the acquisition price was paid for with stock, which is often necessary to keep acquired management teams motivated. But the market hates dilution, and it hates conglomerates. The founder and executive chairman of the board, Bud Brigham, owns a little over 13% of the company, so that should provide some incentive alignment to only engage in accretive acquisitions.

Smart Sand is also about 18% owned by the founder and CEO, Charles E. Young, and also initiated a dividend in October of 2024, but it was a special dividend with no guidance as to whether or not it would be repeated. SND did allocate $10 million for share buybacks last quarter as well, and with a current market capitalization of $91 million, that is large enough to have an impact. In 2024, SND’s sand volumes grew by 17% year over year, so even though in-basin Permian sand volumes are growing aggressively, it does appear that there is a robust market for higher quality long distance Northern White Sand as well.

If the stars align, and SND has growing revenues, a multiple rerating, and an aggressive share buyback program, the current $2.12 share price could reach $8.88 on a rerating to a price to sales ratio of 1.0x. For AESI, the upside potential is a bit more limited. Without a multiple rerating, just on the projected EBITDA growth for 2025, AESI could go from a share price of $14.30 to $21.81. Of course a multiple rerating would add to those returns, but with the potential of the market assigning Atlas a conglomerate discount, it is hard to anticipate a multiple rerating when it already trades at 1.6x sales when US Silica went private at 1.2x sales.

And then there is ProFrac Holdings (ACDC) which is over 86% owned by the father and the uncle of the CEO. And insiders keep on buying more at these low prices. The inside ownership is so high that the threat persists of ACDC going private. The eventual spinoff of Alpine Silica is one reason to stay public, it makes the process easier to already be a public entity. Also, if the share price ever catches a sustained bid, the plan is for the Wilks family to sell some shares eventually.

Alpine Silica could easily represent a value of $300 million to ProFrac Holdings on a spinoff or a sale, and ACDC only has a market capitalization of $735 million. In other words, the sand mines which are responsible for 11% of revenue account for 40% of the market capitalization. This is a classic goodco badco framework where value can be unlocked through spinoffs which would allow the market to value the high quality goodco, Alpine Silica, at a much higher multiple than the parent company, ACDC. And management knows this, and has been discussing the eventual spinoff of Alpine Silica for over a year. In the meanwhile, Alpine will probably deliver around $100 million of EBITDA for ACDC in 2025, providing some much needed cash flow while the frac fleets themselves are in supply destruction pricing.

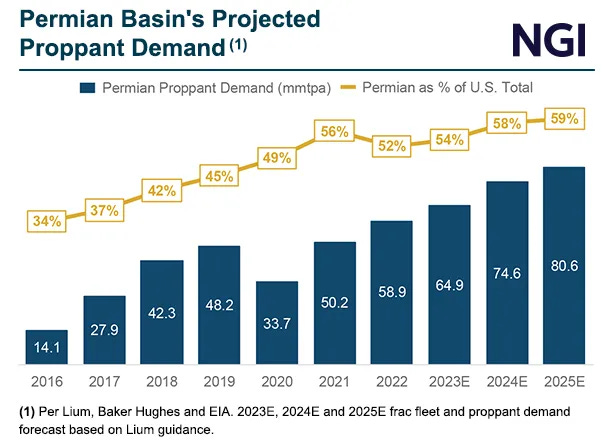

It’s a cyclical business, and the cycle is short, so not much patience is probably needed for oil services in the shale patch. But unlike the demand for frac fleets and drilling rigs, the demand for sand has only been growing and is projected to keep on growing. The percentage of sand demand for the Permian basin has also been increasing, and both AESI and Alpine Silica have exposure to that Permian demand. There isn’t a bad company out of the three, and I already own ACDC in my portfolio. For small cap value degens there is SND, for quality growth market leading degens there is AESI, and for masochists there is ACDC.

Smart Sand (SND) $2.07: $8.88 by the end of 2027

Atlas Energy Solutions (AESI) $13.69: $21 by the end of 2026

ProFrac Holdings (ACDC) $4.23: To the moon Alice, unless they go private first

i own snd since a few years as a 3% position. its a bit lonely due to not much happening to the share price but offers good diversification from my mostly healthcare/junior gold miner portfolio and at this valuation is hard to ignore.

my price target is 8 in 5 years. it is growing revenues (6xed in 10 years) now it just has to figure out profits.

the chart has upside potential with the triangle formation.

Can ACDC go bankrupt? What’s there margin of safety?