Haunted by Ghosts From the Past: B Riley Financial $RILY

Starting next week, I will be taking the family on a road trip for the second half of July. If there are any posts at all, they will be done with my thumbs on the phone around a campfire. I will look forward to returning to my normal writing schedule in the beginning of August. Thank you for your forbearance.

B. Riley Financial (RILY)

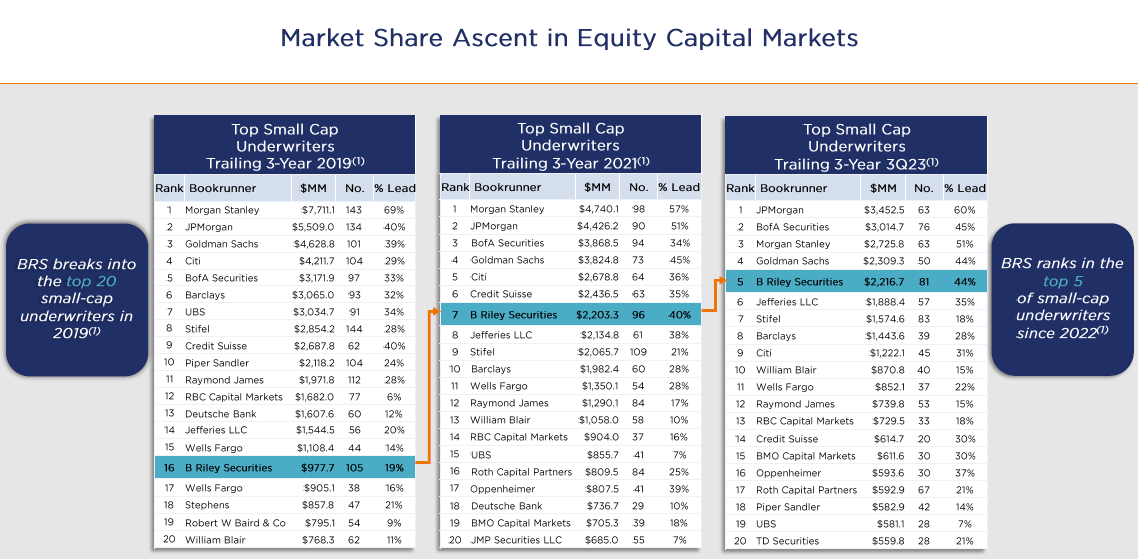

One of my early posts was about a merchant bank with a focus on small caps, B. Riley Financial (RILY). RILY had a lot of great things going for it, starting with a good market niche. Most of the large investment banks don’t want to underwrite any capital markets activity that is less than $500 million, so if you need to raise $200 million, there aren’t many places to turn. At that smaller size, commissions are much higher, while the large investment banks might charge 3% to underwrite a large bond issuance, for small issuances, that number can be as high as 7%. RILY is still controlled by the founder, Bryant Riley, and it has a long history of aggressive insider buying. RILY had been taking significant market share for small cap capital markets activity.

The company had aggressive growth, fat margins, and incredible incentive alignment. I asked all my colleagues that work in finance if they knew anyone that worked at B Riley, and the answer was always the same, the best people they knew worked there. That was because RILY had an “eat what you kill,” commission structure. That type of incentive attracts high caliber employees who want to be able to earn more through their own ability. It also gave RILY a very flexible cost structure, in lean years there wasn’t huge payroll costs dragging them down.

Years of aggressive growth and fat profits had led to RILY making several acquisitions, some were core to their business, creating a flywheel of referrals, but others were purely for income, hopefully income that would be counter-cyclical to capital markets activity. As a market participant, RILY acted a bit like a publicly traded private equity firm, occasionally buying distressed firms out of bankruptcy, rehabilitating them, and selling them later for a fat profit. Other times, if RILY really liked a company they were underwriting, they would eat their own cooking, buying a stake in the company at the IPO. Their years of experience was their guide for which companies to buy into instead of just clipping the 7% commission from underwriting small caps.

This made analyzing RILY an adventure, there were an awful lot of parts for the sum of the part analysis. There still are a lot of parts, but many have since been sold off as the firm has passed through eighteen months of duress.

RILY reached a bit too far with leverage for two large acquisitions, Targus, the leading laptop case brand for North America, and The Franchise Group, formerly a publicly traded franchise conglomerate. As the firm has survived these last two years, the leverage wasn’t fatal. But while RILY was in a weakened position, one of the more skilled short sellers targeted RILY for an attack.

I once believed that short sellers were trying to find overvalued companies and to uncover the truth, bringing the company to fair value. I no longer believe that. Short sellers try to find opaque companies with black boxes of information, and then muddy the waters with fear, uncertainty, and doubt. Two companies I was following were targeted by short sellers at the same time, RILY and Medical Properties Trust (MPW). The short sellers couldn’t really hurt MPW, their revenue was based on 20 year master leases. The uncertainty from the short seller’s accusations may have caused MPW to refinance their debt at a percentage point higher, but it probably isn’t fatal for the company.

But RILY is a financial firm, and financial firms operate on trust. Short sellers accuse their target of fraud, repeatedly, and in a country with freedom of speech it is an uphill battle to sue for defamation. When people start to do their due diligence on a financial firm, if the first news article is accusations of fraud, the pipeline of new business suffers.

In both cases, MPW and RILY, the fraud accusations were absurd. The largest tenant of MPW was accused of bribing officials in Malta to privatize their hospitals. That this would reflect on their landlord is laughable, and yet that is what short sellers do. In the case of RILY, the CEO of the Franchise Group was a portfolio manager for a hedge fund that lied about how many portfolio managers they had. That principal of the hedge fund was prosecuted for fraud, and maybe there would be a case against the CEO of The Franchise Group, but the idea that liability would transfer to the corporate entity of The Franchise Group, or RILY for lending to them and acquiring their stock, never really held much water. Still, short sellers are very good at making sure the first thing everyone reads about a company is fraud accusations, and for a financial firm, this is devastating.

Not all of RILY’s problems were caused by the short sellers, they did reach too far with acquiring both Targus and The Franchise Group. With interest rates high, small cap values low, and consumers weak for more years than most people predicted, RILY found itself in trouble. But I have a strong suspicion that they could have made it through if the fraud accusations didn’t hurt their ability to do business. The Franchise Group needed to sell a couple of assets to survive, and The Vitamin Shoppe, while not an amazing brand, could have probably been sold for enough to make the group solvent. But nobody wanted to touch it with the fear, uncertainty, and doubt of the accusations.

The Franchise Group formally filed for bankruptcy, and RILY blew a billion dollar hole in their balance sheet. On top of that, with their employees unable to do business under the accusation cloud, some of RILY’s key executives left, the head of M&A left with clients and was sued. The budding financial advisory division, the hope and future of the group, was sold off at an enormous loss. And at that point, I told my subscribers that while I still like RILY, and while I believe the short sellers are the mayors of liartown, it’s not the type of content that I want to have on my substack, it belongs in the “too hard” pile, and the risk / reward isn’t what I want to keep following.

Since that time, another value investor extended RILY a lifeline, Howard Marks of Oaktree Capital acquired a majority stake in a part of the RILY flywheel, their liquidations business, and made a senior secured loan to RILY to help them bridge the chaos. The partial asset sale of the liquidations business was actually pretty good for RILY, they got to keep their referral channel, and they got the cash for selling half. But the liquidations business got access to Oaktree Capital, and now could bid on liquidations of any size. They won the Joann Fabrics liquidation, and RILY did not have deep enough pockets on their own to win business that large. It isn’t a victory for RILY, but it isn’t a loss either.

They also were able to sell some non-core businesses that they had acquired, but if you’ve been in small caps these last two years, you know the valuations weren’t amazing. Long story short, RILY is about half finished digging themselves out of this hole, and the fraud accusations are starting to lose their sting, because nobody’s been arrested, and it’s going on two years.

One advantage of having capital markets be their core business, the physician can heal himself. I have seen companies be caught off guard by debt maturities, debt covenants, etc., but not RILY, they know what they are doing, and they are proactive. In the last six months, they have negotiated deals with some of their bondholders to redeem 2025 and 2026 debt in exchange for less face value of 2028 debt at a higher coupon, and a handful of warrants with a strike price of $10 a share. This has reduced debt by $108 million, extended maturities, and kept interest payments flat.

Some of the asset sales have been at decent valuations; they sold Atlantic Recycling, a company that I missed on my first writeup, for $70 million. But just recently, RILY announced the sale of a core asset, GlasRatner advisory services, for $117 million, logging a $66 million gain from the acquisition price. This piece of their referral flywheel does hurt to lose, but RILY has bills to pay.

On top of that, due to the amount of transactions occuring, SEC filings have been late for the last three quarters. RILY is starting to catch up, but the most current data is still a bit old, and some of it is unaudited. I know that can be a red flag, but if you go through the 10-K and see how many moving parts there are, the most likely explanation is that there’s just a lot of work to putting together those filings with so many things changing.

But the market is starting to sniff out the resurrection of B. Riley Financial. The stock price has started moving up. Yesterday in particular, the stock price moved 19% on no news. It doesn’t take much to move the price of a $119 million market cap company, but the size of the move for one day did surprise me.

RILY is a company with a lot of subsidiaries but their core capital markets business alone generated $272 million EBITDA in 2021 when the capital markets were hot. Will we have a hot year again when Trump replaces Powell in ten months?

So where does that leave RILY today? The most current SEC filing was filed in February of 2025, and covers the quarter ending in September of 2024. The most current earnings call was in March, and it covered through the end of 2024. Due the late filings, they are not in compliance with NASDAQ, but they have obtained a waiver, and do not appear to be at risk of delisting. Filings have been late for almost a year now, but they have been submitting them eventually.

The preliminary unaudited results for Q4 2024 indicate a positive net income of $48 million, or about $1.57 per share. Not bad for a stock that closed at $3.92 after rallying 19% from $3.29. But most of that net income is gains on the sale of assets, and operating income was a loss of $178 million. But most of that loss is non-cash goodwill impairments and unrealized losses on investments, so really operating losses were closer to $50 million. A $119 million market cap company losing $50 million in one quarter from operations is a bit terrifying. Operating adjusted EBITDA for the quarter is projected to be around $12 million.

The company still has about $1.78 billion of debt, which is after they paid off $700 million over this past year through asset sales. They do have about $150 million of cash on hand, and that is after retiring the 2025 maturity in February, so at least the liquidity situation is decent. But to make a decision on RILY, we need to know more about which assets remain, and what kind of income they can generate.

RILY still owns 28 million shares of the company I wrote about yesterday, Babcock and Wilcox (BW). At today’s stock price, that is worth around $28 million, but as I mentioned in yesterday’s writeup, they have a pretty decent path toward reaching $7 a share, which would put RILY’s stake at $196 million, a big difference. Assuming that RILY is not a distressed seller and can wait for the rerating, which is not guaranteed.

They also own over 4 million shares of DoubleDown Interactive (DDI), that’s worth about $50 million today, but it could easily rerate to be worth $150 million in a few quarters. There’s another $10 million of Synchronoss shares (SNCR), but if small caps are rallying, it traded at triple the current price in 2022.

RILY has another $127 million in private equities, it’s black boxes like these that make it a target of short sellers. I don’t know what that contains, but I do know that those assets are not marked to market and reflect cost. Some of this is an oil limited partnership in California, but this is how the Atlantic Recycling sale snuck up on me, I don’t know what’s in their private equity holdings.

RILY still owns a bundle of communications companies, United Online, magicJack, and Marconi Wireless which are shrinking year over year, as well as Lingo and Bullseye which are growing year over year. The whole group did $225 million of revenue in the first nine months of 2024. Conservatively, a handful of communications companies that generate $300 million in annual revenue is probably worth at least $100 million, and probably closer to $200 million.

The consumer products segment is, I believe, Targus, the laptop case company. They had $150 million in revenue in the first nine months of 2024. In 2022, Targus generated $50 million of EBITDA. If they tried to sell it, I would guess the floor valuation would be at least $75 million, but in a good year, it could fetch closer to $200 million.

It’s not pretty, but RILY still has levers to pull. The next time capital markets are hot, if RILY hasn’t permanently lost small cap market share, they could earn upwards of $300 million in a year, or $10 a share. This is a company that paid $12.50 in dividends in 2021. They have sold a lot of assets, but most of those weren’t contributing to EBITDA in 2021, most of the core business remains intact, or has even grown with several acquisitions made over the last few years.

RILY had over $150 million of cash on hand six months ago, but I don’t have a good estimate on their burn rate. Management has successfully extended maturities and reduced debt. If the last two years didn’t kill RILY, I think odds are good it survives until the next boom. And in the next boom, the earnings power could surprise everyone. Will RILY return to $40 a share in the near term? I have serious doubts. But I wouldn’t be surprised to see it hit $20 a share at some point within the Trump administration if we really see interest rate relief and we have an IPO wave.

This is not an investment for the faint of heart. The ride has been so bumpy, I would say that only investors with a serious stomach should consider it. Heck, maybe it’s even only appropriate for masochists. It still isn’t the right risk / reward for my Substack, but I know the company better than most, and the stock price has suddenly awakened from the dead. If you are a hardcore value degen, bon appetit! For everyone else, I think there is easier money to be made from Sibanye Stillwater (SBSW), any of the three major deepwater offshore Transocean (RIG), Valaris (VAL), or Noble (NE), as well as the equipment dealerships Alta Equipment Group (ALTG), Custom Truck One Source (CTOS). There are still opportunities with the Silver Tsunami, you could buy Jackson Financial (JXN), Abacus Life (ABL), or Finance of America Companies (FOA). Or many others that I have written about and don’t have a highly skilled short seller spreading uncertainty about them.

B Rily Financial (RILY) $3.96: $20 before the end of 2028.

I'm a member of the Capital Mindset community (this is how I discovered and subbed to you) and RILY was a big short candidate in the community last year. I'm a bit surprised on your stance, I think the short seller's thesis was very warranted. You didn't mention the adverse opinion that they got from their auditor (that they had since 2009) that I believe had to do with the way they were accounting for the value of their internal businesses like FRG. I don't remember all of the details, but the big picture idea was that RILY was inflating the value of their assets (if I remember correctly) and becoming increasingly overleveraged in an unsustainable interparty way that led to the deterioration of the business but the majority shareholders (mainly B Riley himself) getting paid a fat dividend. Marc Cohodes was all over this one. Would be interested in hearing your rebuttal to this as respectfully, I think this thing is a pile of garbage. Long JXN

Excellent write-up!

RILY's baby bonds and preferred units are quite an interesting proposition. After the April drama, prefs (RILYP and RILYL) traded at nearly a 100% current yield.

For now, I am staying on the fence, but I may soon take a position.