Frac Services Thunderdome: ProFrac Holdings $ACDC vs. Trican Well Service $TCW.TO

Two Stocks Enter, One Stock Leaves

ProFrac Holdings (ACDC) was one of the first stocks I wrote about on this subtack. The stock price has been sideways for a year, but with large ups and downs. They are a vertically integrated frac services company that has been aggressively rolling up competition during this trough of the frac cycle.

The ballad of $ACDC, why ProFrac Holdings is a green AI story that could easily triple in the near term.

Edited 11/2/2024: Operating cash flow for 2Q 2024 was $113 million. They did indeed do that acquisition in Midland, Texas. I was early on this one, but I think it has a high probability of inflecting going in to 2025. There is still a good chance it will be the victim of tax loss harvesting for the last two months of 2024. With the Permian Basin ba…

Trican Well Service (TCW.TO) is, in some ways, the Canadian version of ACDC. But while ACDC is currently in third place in the US for frac fleets, TCW is far and away the market leader in Canada. The market leader in Canada, however, generates about one third of the revenues of the third place frac services company in the US, so Trican is a good bit smaller than ACDC.

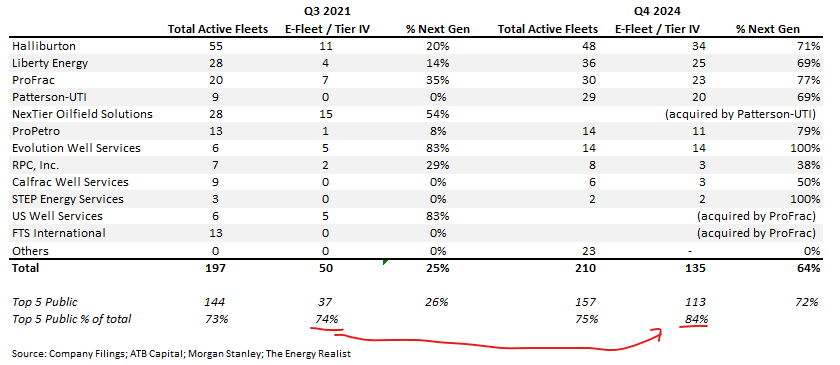

Industry Consolidation and Fleet Electrification in the USA:

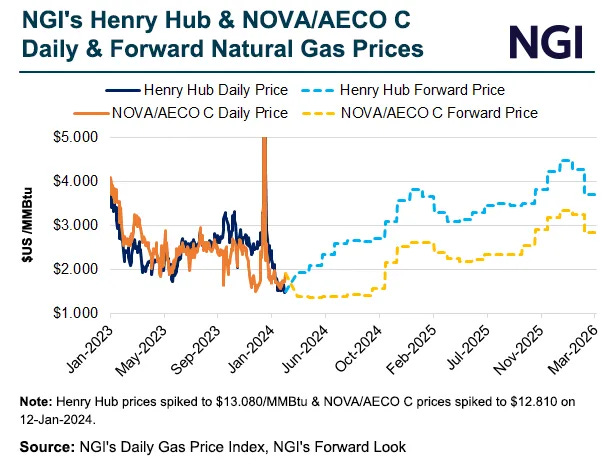

In attempting to compare the two companies side by side, it’s worth noting that Canada and the US are not identical markets. Even though energy is a fungible commodity, the storage and transportation difficulties of natural gas makes for a segmented market. In the US, producers have cut back on drilling during this down cycle, especially in the Haynesville where ACDC has a disproportionate market share. In Canada the producers have been much more aggressive, and have driven down natural gas costs far below the US price. There is an almost perpetual discount for AECO-C gas vs Henry Hub.

In other words, despite how much we complain about them, the American producers are more responsive to shutting in production in response to weak prices than the Canadian producers. While this is bad for Canadian producers, this has benefitted Trican as their customers don’t pull back on activity as much as their US counterparts. Trican has maintained a GAAP net income positive position throughout this entire two year oil and gas cycle, meanwhile, ACDC has been able to show operating cashflow, but not GAAP net income.

Trican is debt free, and has been able to return capital to shareholders in the form of share buybacks, retiring 47% of the float in the last 7 years. ProFrac Holdings has about $1.1 billion of long term debt, which is good and bad. Good because leverage can increase returns, but bad because it increases the chance of bankruptcy at the bottom of a cycle. I believe we are already at the bottom of the frac cycle, most management teams are guiding toward growth in 2025 as natural gas export terminals come online, so the debt risk of ProFrac Holdings is probably mitigated. Frac fleet counts have risen in the last week, but this may be more due to the effects of the cold winter than true evidence that the cycle has finally turned.

ACDC’s management is guiding toward a bad result next quarter when they announce in a couple of weeks, but a stronger 2025. Trican is guiding toward a strong next quarter, but a flat 2025. Both are managing their fleets toward running on natural gas over diesel, but ACDC is farther ahead in this process.

Trican’s stock has outperformed ACDC’s over the last year, up from 4.00 CAD to 4.59 CAD. This is likely due to the GAAP net income positive results and the share buyback, but even so, the recent value selloff has brought the stock price down from 5.39 CAD to 4.59 CAD. Trican is currently trading at 1.00x price to sales, and 1.83x price to book. Due to the constant upgrade cycle of equipment and depreciation, I would expect book value to be a reasonable metric. ACDC’s stock price is flat from $6.90 a year ago to $7.30 today, although also down from a recent high of $9.22. ACDC is trading at a price to sales of 0.52x and a price to book of 1.06x. So Trican has the benefit of momentum, but ACDC is a cheaper stock that has the potential to double just to match Trican’s multiples.

ACDC has two major advantages over Trican, the ownership of 8 sand mines, and the ownership of a frac truck maintenance, design and manufacturing company. The sand mines are intended to be a spinoff when the market prices justify it. But the frac fleet manufacturing and maintenance allows ACDC to grow into demand as the cycle inflects while their competitors would be scrambling to acquire more capacity.

I find both companies to be very reasonable investments. Oil services is a much better slice of the energy pie than short-lived shale explorers and producers. Trican is much more of a quality name, maintaining positive GAAP net income, paying a dividend, and executing an aggressive share buyback program, but there isn’t much room for a multiple rerating going forward. Even Halliburton (HAL) only trades at a price to book of 2.5x, so how much more expensive can Trican get without growth, and management is guiding toward a mostly flat 2025? Profrac could easily double from multiple expansion alone, and revenue has a much greater capacity to increase if the activity in the Haynesville accelerates to accommodate the new natural gas export facilities.

As for me, I am going to stick with ACDC as it has the bigger potential from here. Putting multiples on the frac services companies at the trough of the cycle is dangerous, because it’s impossible to tell what those services will cost at the top of the cycle. An enormous amount of capacity in the US has come offline, meanwhile, Canada still has significant excess capacity. At one time, ACDC management guided that with their vertical integration, in a boom scenario, each fleet could generate $50 million of EBITDA alone. Since that time, ACDC has retired around ten older diesel fleets, but they still operate 30 fleets, have a few others to deploy, and can build more as needed. That would put peak cycle EBITDA over $1.5 billion. Meanwhile, Trican operates 7 fleets, and they don’t appear to have the immediate capacity to add more. That would put Trican’s peak cycle EBITDA around $350 million compared to ACDC’s $1.5 billion. Trican is already at about 44% of that peak cycle EBITDA, where ACDC is operating at around 24% of peak cycle EBITDA. When I think about the potential torque, Trican could do a bit better than doubling at the next cycle peak due to increased earnings, multiple expansion, and the cumulative effects of buybacks. But ACDC could be a five bagger in the same time period.

Trican Well Service (TCW.TO) 4.59 CAD: 9.32 by end of year 2027

ProFrac Holdings (ACDC) $7.30: $34.38 by end of year 2027

acdc has a long base but no volume driven break out yet.