For Deep Value, Please Press 1 Followed by the Pound Sign: TTEC Holdings $TTEC

Ten Bagger or Two Bagger or Bust

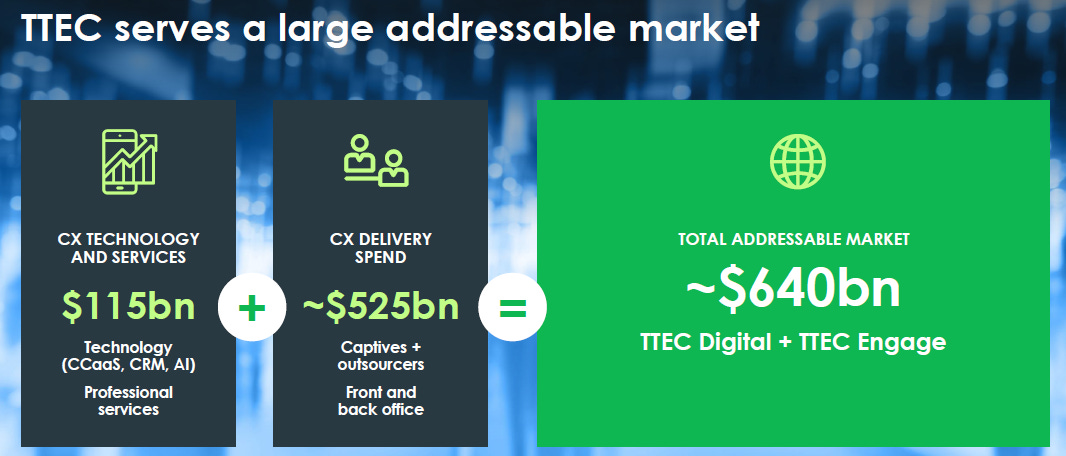

TTEC Holdings (TTEC) is a customer service outsourcing company. Within that industry they call themselves customer experience, CX for short, and it is approximately a $600 billion annual global industry. Of that $600 billion, TTEC did $2.26 billion in sales in the last twelve months, which is incredible for a $166 million market capitalization company trading at 0.07x price to sales.

There is a lot of competition within the CX industry, Concentrix (CNXC), Teleperformance (TEP.PA), Genpact (G), TaskUs (TASK), and many more that are either private or are subsidiaries of much larger companies. TTEC has a reasonable position in the market with clients across different business segments such as finance, healthcare, automotive, municipal governments, etc. But what makes TTEC stand out is that it was founded in 1982 by Ken Tuchman who is still the CEO, Chairman of the Board, and 58% owner who has made an offer to the board of directors to take TTEC private at $6.85 a share. The stock is currently trading at $3.49.

I’m not one to turn my nose up at a 96% return over a short time frame, but as I dig into the fundamentals of the company, I can’t help but feel that a ten bagger or better is being ripped from my eager grasp.

First things first, why is TTEC priced for bankruptcy? Most of the CX industry has a similar stock chart due to the perceived threat from Artificial Intelligence. I believe that this is a mistake, because every one of the companies in this space has an AI integration plan which is much more likely to succeed than the plan of a pure AI company which would try to poach their client relationships. Rumors of these companies’ deaths are greatly exaggerated. But, revenues are mostly flat across the whole industry for the last two years. This isn’t due to AI, but do you remember Tech’s year of efficiency? Well, it wasn’t just tech, and it wasn’t just about hiring. With higher interest rates, suddenly capital has a cost, and every industry is tightening the belt, and has been for more than two years. I’m not sure what it would take to snap corporate America out of this mindset, but we can even see it on this quarter’s earnings, out of the S&P 500 companies that have announced, revenues are up 5% and earnings are up 10%. The belt tightening continues.

On top of a tight market for CX services, TTEC chose to take a $250 million goodwill impairment within the last twelve months, so their GAAP earnings per share are a trainwreck. But that was a non-cash event, and I do believe those are all of the forces dragging down the stock price. TTEC is not in any imminent risk of bankruptcy, with trailing twelve month operating income of $79 million, interest expense of $84 million, and $280 million more current assets than current liabilities, TTEC is in a mostly stable position for now.

TTEC’s competitors have less debt, and their margins have held up better, but their revenues are in a very similar position. TASK’s trailing twelve month sales are below 2022 levels, and Genpact’s are up, but only slightly. Based on the best interpretation of the evidence I can give, it is the market that is tight, and it is not the case that TTEC is losing out to competition in a big way.

Due to Ken Tuchman’s status as founder, CEO, Chairman of the Board, and 58% shareholder, I do believe his take private bid will be successful, which is unfortunate, because I would rather own the stock for the rerating from a 0.07x price to sales to a 0.50x - 1.0x price to sales. But without imminent bankruptcy as a possibility, this isn’t likely a “Ten Bagger or Bust” situation. It’s an odd sort of “Ten Bagger or Two Bagger” situation, with the two bagger dramatically more probable than the ten bagger.

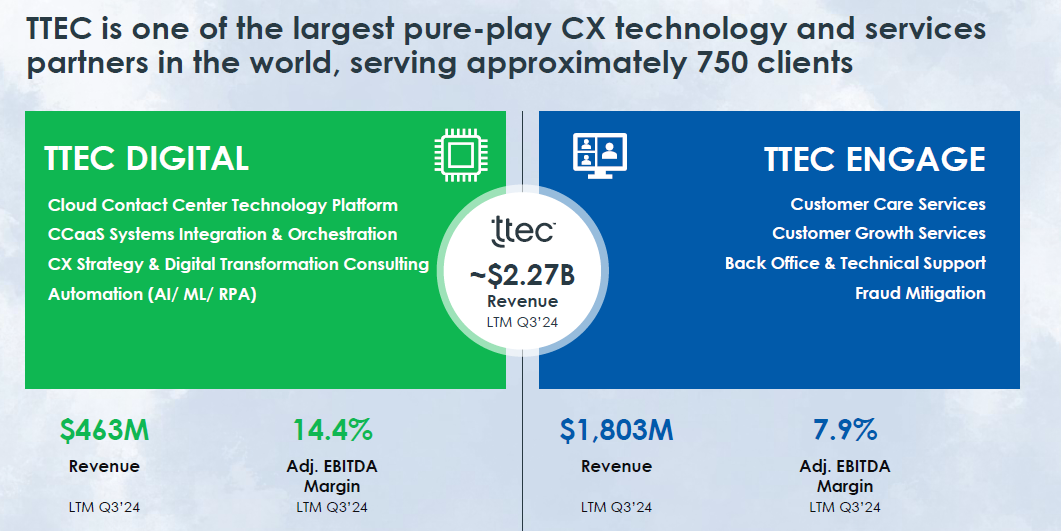

The rest of the analysis really isn’t that important, given that the future is mostly known regarding TTEC, but just for the sake of argument that the take private bid is rejected, TTEC has two main business segments. The traditional CX business, the one with over 50,000 employees doing things the old fashioned way, this is about $1.8 billion of trailing twelve month revenue. And the Cloud, AI, SaaS, automation part of the business, which is about $463 million of trailing twelve month revenue. Can you imagine what kind of multiple the half billion revenue, 14% margin SaaS business would fetch as a standalone enterprise?

But putting multiples on TTEC is a frivolous endeavor until we know what kind of growth rate it will return to in normal times. Of course management assures us that there is a plan in place to turn the ship around, and the overall macro environment will likely improve with the start of the global interest rate cutting cycle. But if TTEC isn’t taken private, this is a stock that I would have to watch more closely to ascertain once and for all if the management team really does have what it takes to return the company to growth. For now it’s a mystery, and based on the earnings calls, I don’t have a good guess as to whether management has what it takes to bring TTEC back to their glory days. What really comforts me is that many of their public competitors are struggling as well, and this is most likely an industry-wide problem, and not a TTEC specific problem.

In Q2 of 2021, TTEC had trailing twelve month earnings of $3.45 per share, traded at a price to earnings ratio of over 27x, and had a share price of $96.56. Today it trades at $3.49 a share, and there was no dilution in between. We probably won’t experience a repeat of the 2021 stock market environment, that might stay in the past along with the zero-interest rate policy that fueled it. I don’t anticipate a return of TTEC to its prior $5 billion market capitalization, but it could easily return to the $1.5 billion market capitalization that it traded at for years. For that to happen, all that would be needed would be a credible rollout of AI products such that the market no longer feared obsolescence, and a return to normal operating margins. Is that so far-fetched? But I don’t believe that will happen, not because TTEC is a bad business, but because Ken Tuchman will have taken it private for $6.85 a share. Well, here’s to 96%. Cheers!

Why is the stock price not converging with the takeover bid price? Does nobody take the offer seriously?

I’ll put this comment here in case anyone else is following this stock. In your most recent post, you mentioned you had a feeling the privatisation deal might be announced soon. What makes you think that? I emailed IR at the company to ask where it was at. They had formed whatever advisory committees they are required to, so they should be able to tell us something about when they expect them to report.