Equinox Gold Merging with Calibre $EQX & $CXB.TO; Q4 Earnings Update Part III: $JXN, $RIG, $HOEGF, $HAUTO.OL, $ECO

Apologies for the slow pace of publishing this last week. I have had a lot of life events recently, and things might just get more exciting as I have been called in for jury duty.

I am borrowing a slide from Warren Pies at 3Fourteen Research where he shows graphically what I was talking about in my last writeup, the market is in “shoot first, ask questions later” mode.

This is in stark contrast to how things were just three months ago:

I believe the biggest driver of this is the partisan nature of consumer confidence and inflation expectations. The two parties really do live in different worlds with opinions formed by different echo chambers. As Trump surged in the polls, Democrat confidence in the economy fell from 90% to 50%. But since the stock market and stock market active participants are mostly located in the wealthy coastal cities, the blue view of the world is affecting equity prices. It is probably safe to expect an unfriendly stock market until enough bullish hard data comes out to chase away the bearish soft data.

Jackson Financial (JXN):

If there’s any value I add through this substack, listening to Jackson Financial’s earnings calls is probably at the top of the list. If you suffer from insomnia, just download the Quartr app on your phone and add JXN to your watch list. Those lady bean counters do an excellent job at managing Jackson Financial, but listening to them is a special kind of torture.

Jackson’s stock absolutely did not deserve to sell off with the rest, and having a chance to buy it at $84.50 is a gift. At a $5.995 billion market capitalization, JXN trades at 0.65x price to tangible book, this makes their share buyback program highly accretive. For full year 2024, Jackson had guided toward returning to shareholders between $550 million and $650 million. They delivered $631 million returned to shareholders through a $415 million share repurchase program and a $216 million dividend for the full year. Looking forward, management is guiding toward a 2025 return to shareholders of $700 million to $800 million.

Jackson’s management has guided toward 23% growth in return of capital to shareholders for next year, and the stock sold off from $95 to $82.50. Amazing. At the low end of guidance, JXN will distribute an 11.6% yield from buybacks and dividends for 2025, and as their book of business grows, the company just gets better and better. When insurance-like companies are growing, their return to shareholders is less due to the amount of money that has to be continually set aside to maintain liquidity ratios. For the duration of the silver tsunami, as baby boomers buy their variable annuities, JXN’s free cash flow and return to shareholders will understate their improving business. JXN earned $18.76 per share, but only returned to shareholders about $8.60 of that (I am using their operating earnings due to the mark to market effect of derivatives.) The rest is sunk into the working capital of the business. If you hold JXN until the silver tsunami is over, the distribution to shareholders will inflect as they will no longer need to keep sinking money into their working capital account. But in the meantime, the dollar value of new variable annuities sold increased 39% in 2024 over 2023.

Based on operating income of $18.61 for 2024, JXN trades at a price to earnings ratio of 4.44x, but more established and mature financial firms trade at a P/E ratio of 15x to 20x. There is room for JXN to triple from here at least, but the rerating will likely take years as the market slowly figures out what a cash cow this business is. As the customer base grows and growth slows naturally as a percentage of business, the payout ratio will increase, and JXN’s multiples will catch up with it. And while you wait for the triple from a rerating, shares are being bought back currently at below price to book value. Eventually price to book will pass 1.0x, but JXN will most likely maintain a solid share buyback program, their capital return strategy is to use share buybacks to create an inorganically growing dividend, to complement the fact that they are organically growing their earnings per share anyway.

If you focus only on the capital returned to shareholders, JXN’s yield is 11.6%, growing at 23%. But if you include the capital that needs to be sunk into the business during the silver tsunami, that will eventually be able to be unwound when JXN reaches a more mature size, the earnings yield is 22%, and it grew by 14.6% in 2024. Either way you slice it, JXN is an amazing quality compounder, and if management doesn’t break anything, you could probably own it for at least the next 20 years and be quite happy with the outcome, or the income (pun intended).

Transocean (RIG):

Transocean announced the retirement of Jeremy Thigpen, CEO since 2015. Thigpen navigated RIG through the offshore bear market of the last decade without wiping out shareholders and declaring bankruptcy. A heroic feat. He will be succeeded by the current President and COO Keelan Adamson, who no doubt has been preparing for this transition for several years. It is unlikely that a change in CEOs will dramatically change Transocean’s overall strategy, especially with Frederik Mohn as a 10% shareholder sitting on the board.

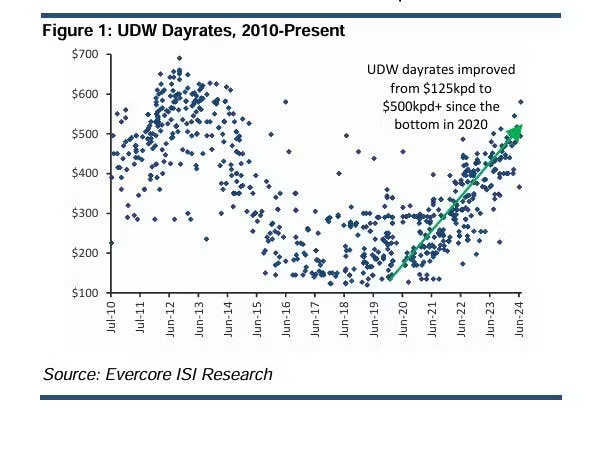

For the prior quarter, revenues are $952 million vs $741 million in Q4 of 2023, that’s $211 million or 28% higher than they were last year. Old contracts keep on rolling off, and new contracts at higher day rates keep rolling on. It’s amazing how the price of RIG climbed so high when the contracts were announced, but before the earnings materialized, and now it trades at the same price as in October of 2022, when day rates were still $300,000 per day. I know that the market is disappointed that the day rates didn’t keep on moving higher in a straight line, but the thesis hasn’t changed, there is no orderbook for drillships, oil remains the most important global commodity, and it will remain the most important global commodity for decades.

EBITDA was $338 million for Q4 2024, up from $105 million for Q4 2023, a 221% increase. Interest expense for the quarter was $152 million, a terrible burden, but that still leaves a lot of cash flow afterward for a $2.95 billion market capitalization company. It’s not free cash flow, because RIG has some amortizing debt, but with $55 million of taxes, $131 million is still a 4.44% return for the last quarter. Hardly a company heading toward imminent bankruptcy. And the backlog is still $8.3 billion.

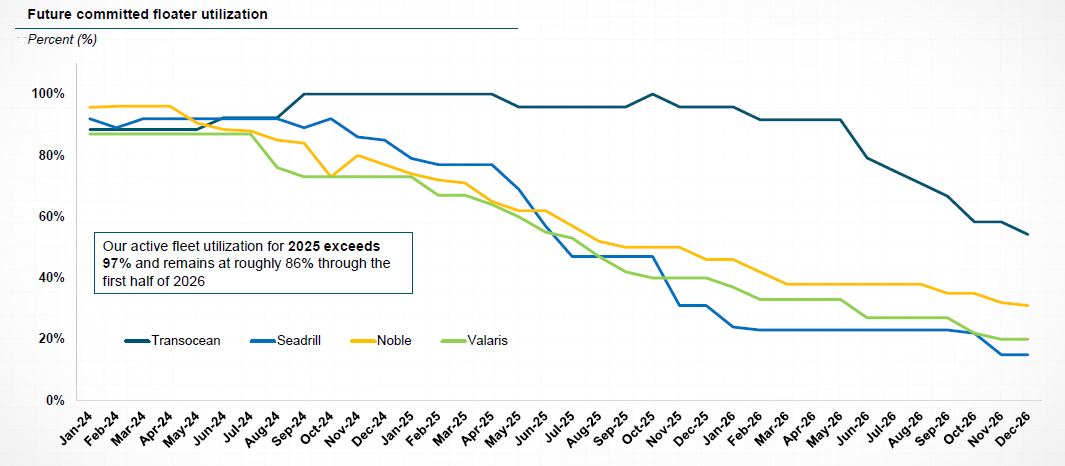

There has been a sudden shift in the discussion now that the new contracting cycle has started to slow down. Surprisingly, RIG went from the offshore driller with the most whitespace to the one with the least. I do suspect that there will be some new contracts handed out sometime this summer or fall, but in the meantime, RIG is sitting in the best position for 2026. Management was maligned after several small dilutive acquisitions, but I still think odds are good that this is the best management team in the business. Rumors of the Seadrill acquisition are still hanging over Transocean’s share price. At current valuations, the dilution necessary would be disastrous for RIG shareholders. But Seadrill’s share price might start to feel the pressure from their whitespace, and Transocean’s share price might start to anticipate the transition to free cash flow positive and bridge the gap between the valuations. The acquisition is still fundamentally a good idea, but at the moment the valuation gap is still too wide.

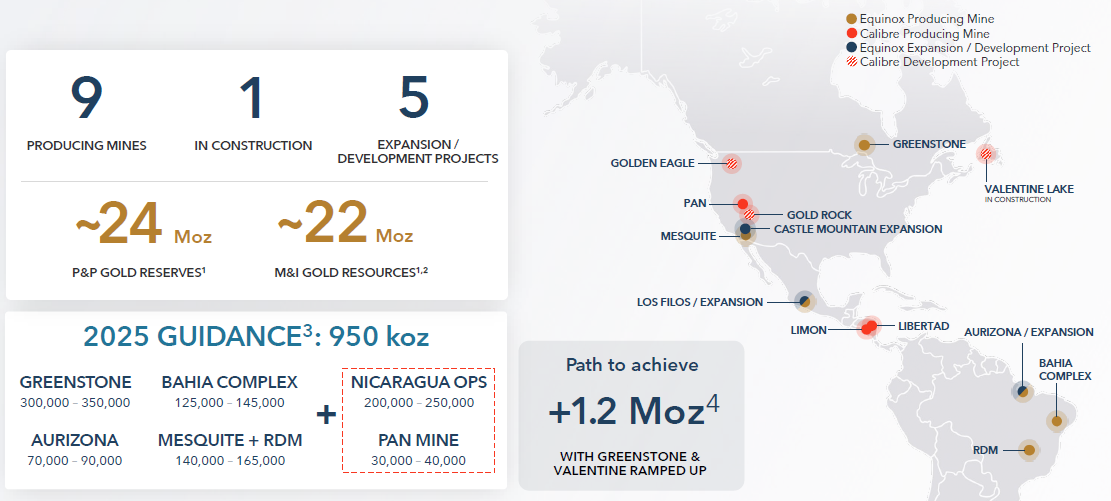

Equinox Gold (EQX) and Calibre Mining (CXB.TO):

At current gold prices, with the Greenstone mine coming up to full production, Equinox Gold’s revenues should increase by about 50% for 2025, and EBITA should increase by about 50% as well. That is based on the lowest end of management’s guidance of 635,000 ounces of gold mined, and assuming the gold price doesn’t rise further from here. It is true that 2024 production was below management’s guidance that was put forward in 2023, the ramp up period of Greenstone was underestimated. This is not enough of a mistake to cast doubt on management in my opinion, EQX has been operating well as miners go.

There is room for an upside surprise, rare in mining. The Los Filos mine in Mexico is shut down until further notice as EQX cannot operate without permission from three local communities. As of the last earnings call, two of the three have signed a long term contract with EQX, but there can’t be any mining without the third. Last year, the Los Filos mine generated 170,000 ounces of gold at an AISC of over $2,100. The requests of the third community seem based more around negotiating a price rather than some sort of insurmountable environmental concern, so my best uneducated guess is that Los Filos will be back into production at some point. But even with new long-term agreements in hand, with an anti-mining socialist president at the helm, it’s not immediately obvious that EQX would prioritize their prior planned expansion of Los Filos to 280,000 ounces of annual production.

Now that Greenstone is finished, the next capital intensive project is somewhat on hold, as the Los Filos was a major potential expansion project, and Castle Mountain is waiting for more permitting to begin Phase 2. In the meanwhile, EQX only has about $100 million of expansion capex planned for proving reserves and expanding the Bahia Complex in Brazil. That’s a slow growth trajectory for Ross Beatty, who is in a hurry to put a cherry on the top of his career.

Management had guided toward focusing on paying down debt organically, however, surprise surprise, leverage ratios can be improved inorganically as well. Just yesterday Equinox announced that they entered into a merger agreement with Calibre Mining to merge in a stock-based transaction. Dilution to Equinox shareholders will be 35%, and in exchange for this, Equinox gets Calibre’s management team on their board of directors as well as about 200,000 ounces of annual production in Nicaragua, and the fully funded greenfield tier 1 development project of Valentine Lake in Labrador Newfoundland which is projected to produce another 200,000 annually starting in about four months, but with a ramping up period as well.

Is 35% dilution worth it to acquire Calibre? Usually we would expect the acquirer to overpay for an acquisition. But in this instance that doesn’t appear to be the case. It appears that the valuations were pretty clearly split down the middle with neither party demanding a premium. This could be because the founders of both companies will remain involved in the joint company, and it is a mythology in gold mining that once production surpasses 1 million ounces a year, multiples expand. Perhaps the management teams of both companies wanted to hit the 1 million ounces a year milestone before this gold bull market reaches its climax?

Based on 2026 projected production, valuing EQX at 65% for 800,000 ounces and CXB at 35% for 450,000 ounces seems pretty reasonable. Based on trailing twelve month revenues, $1.2 billion for 65% and $410 million for 35% seems less so, but it’s not an apples to apples comparison with Greenstone at about half production, and Valentine not yet started production. Book value is never terribly accurate in mining, but based on tangible book value, $2.4 billion for 65% and $673 million for 35% seems very uneven. But the quality of the assets is important to take into account as CXB’s Nicaragua production has an AISC of around $1,500, while EQX’s Mexico and Brazil production has an AISC closer to $2,100.

When you see a merger agreement with such round numbers as in this one 65/35, as opposed to 62.7/37.3 or 66.4/33.6 etc., it’s clear that the principals made a handshake agreement for the merger without getting too bogged down in the spreadsheets. If they aren’t crunching the numbers too aggressively, why should we? Both parties get to be a part of the 1 million ounce annual production club much faster. Equinox gets to inorganically de-lever the balance sheet, as their debt is now spread across more assets. This will free up Equinox to spend more aggressively on growth and to focus less on paying down debt, as Ross Beaty isn’t getting any younger and he wants to make another world class mining company before he expires.

Do shareholder’s benefit? That will depend on whether or not the multiple re-rating from being larger and less indebted actually materializes. Equinox trades at 0.7x price to NAV while Lundin Gold trades at 1.4x, Gold Fields trades at 1.3x, and Kinross trades at 1.0x. I am noticing a concerning pattern in valuations, however, the price to NAV ratio doesn’t have a meaningful cutoff at the 1 million ounces of annual production threshold, but it does have a meaningful cutoff at 2 million ounces of annual production. Oh what cruel fates when data doesn’t support mythology! But give Ross Beaty a few more years, he’ll hit that 2 million ounce threshold soon enough. A fully expanded Los Filos, Castle Mountain, and Aurizona is almost enough to get the merged company to 2 million ounces by 2028 give or take.

In the meanwhile, if gold prices stay at $2,950 an ounce, 2026 estimated EBITDA is about $2.4 billion. Trailing twelve month EBITDA is about $1.63 per share, but 2026 projected diluted EBITDA is $3.42 per share. That’s more than a double over the next two years if gold prices don’t move any higher and without a multiple rerating. I would happily buy more EQX here at 4.2x trailing price to EBITDA, or 2.0x price to 2026 projected EBITDA.

Höegh Autoliners (HOEGF, HAUTO.OL)

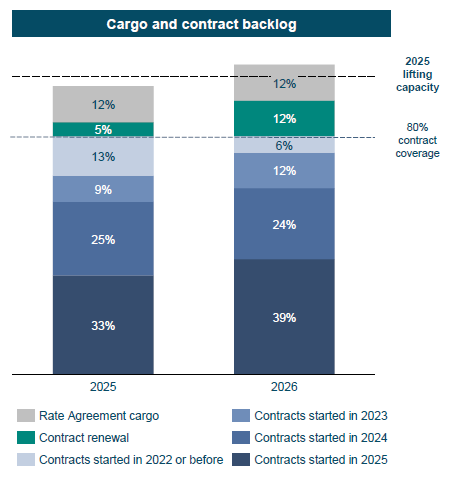

My timing is never perfect, any stock I write about can easily fall in price after I buy it. But it is a surprise that Höegh now trades at $7.72 a share. Höegh’s management timed their cycle perfectly, locking in fixed contracts at the peak of the cycle. They now have a 3.5 year backlog with 80% of their fleet contracted. And the 20% that aren’t contracted are the high and heavy category which are a stronger market and management chooses not to contract them. Beyond that, they contract volume, not day rates, so peace with the Houthis would be good for Höegh unlike most shipping companies. While any small cap investor has gripes about executive compensation, the timing of this cycle was where leadership added serious value.

Due to the delivery of three newbuilds in 2024, the dividends in that year were elevated by the sales of three older vessels. Also, this most recent dividend was slightly lower due to a $26 million capex payment for the rest of the ordered newbuilds, which are now fully financed except for an $11 million payment likely to take away from next quarter’s dividend. This $1.47 billion market cap company just declared $90 million in dividends. My rough estimate for the next three quarters would be, $105 million, $116 million, $116 million. That would generate a 29% yield. Again, this estimate comes from the fact that last quarter had a $26 million capex payment, of which only $11 million is remaining. It might even understate things as capacity is increasing due to the arrival of newbuilds, and costs are decreasing due to the energy efficiency of the newbuilds as well as the upgrades that were implemented last year through expensive drydocks; 2025 has about half as many drydocks for upgrades as 2024 did.

There is still some room for income and dividends to increase (although not much) as some 2022 or older contracts have yet to roll off. The day rates for charters are down from their peaks, but that doesn’t mean that Höegh will suffer proportionately. Höegh contracts cargoes, not day rates. And their European customers will pay up for the environmental upgrades. As the day rates fall, so does the resale value of the older ships. As more newbuilds are delivered, don’t expect Höegh to be able to get over $60 million for a 19-year old vessel again.

One advantage to being a jack-of-all-trades (an expert in none), is that I can glean some useful information from one sector that applies to another. Höegh mentioned that auto exports from China to Europe were surprisingly strong due to the Chinese ability to switch rapidly from electric vehicles to hybrids in response to EU electric vehicle tariffs. This increase in hybrid production is a key part of the platinum group metals thesis, as hybrids use 15% more PGMs than internal combustion vehicles. It’s probably still early to buy Sibanye Stillwater, but there are vibrations in the spiderweb.

Okeanis Eco Tankers (ECO):

Okeanis is another company that sold off in the recent market rout, understandably so as earnings are down for the moment. But in this case, Okeanis isn’t desirable because of the backlog of fixed contracts that protect earnings, it’s desirable because it’s the youngest fleet on the market. The investment thesis is that at some point in the future, crude oil tanker prices will enjoy a cyclical high, and when they do, the youngest fleet on the water will still be floating to take advantage of it. As for how long that will take, it’s anybody’s guess.

Crude oil tanker day rates are back up under Trump after falling last quarter. Cutting off Iran from the world market ties up old tankers for floating storage, and it adds ton mile demand to the global marketplace. While day rates were around $39,000 for last quarter, they are already back up around $50,000 in the last month. This doesn’t help immediately, as 80% of the fleet had contracts locked in around the $39,000 range. But the orderbook for crude oil tankers is still low, and so as long as oil remains the most important global commodity, Okeanis will have their day in the sun again. In the meanwhile, management earned about $30 million in operational cash flow for the quarter, or about $13 million in net income, which is not amazing for a $700 million market capitalization. Expect next quarter to be similar, but to see improvements after that as day rates stay high due to the maximum pressure strategy on Iran.

I loved reading this "When you see a merger agreement with such round numbers as in this one 65/35, as opposed to 62.7/37.3 or 66.4/33.6 etc., it’s clear that the principals made a handshake agreement for the merger without getting too bogged down in the spreadsheets." this is the world that I have lived my life in.

Great writeup. Can you expand on HAUTO that they contract cargo volume and not rates? I thought that when they make a contract they stipulate volumes AND rates for those volumes.