Engineers, Good with Numbers, Bad at Deadlines, Hawkward at Parties: $ECG Everus Construction Group

I took a shallow dive this weekend into engineering firms. In a recent podcast interview, Peter Boockvar argued that municipal spending would be declining in 2025, and this had the potential to slow down the economy. This didn’t jive with the forecasts of Alta Equipment Group (ALTG) and Custom Truck One Source (CTOS) that state and local infrastructure spending was going to be strong in 2025. In search of a tie breaker, I turned to the earnings calls and forecasts of engineering firms.

Typically I would not be fishing in the pond of engineering firms for opportunity. Thin margins in a cyclical business are not particularly enticing to me. But I find the commentary on earnings calls to give me a lot more insight into the economy than survey data, seasonally adjusted data, hedonically adjusted data, think tank research, etc. The big threat to using earnings calls to get the pulse of the economy is that occasionally one firm is just underperforming. A couple of years ago, FedEx blamed their poor earnings on an economic slowdown but UPS and Amazon both said that things were fine. It turned out that FedEx was just flailing, and blamed it on the overall economy.

Well, the engineering firms which cover Department of Transportation construction and Utilities power grid construction have backlogs that are exploding. Most important to ALTG is that Construction Partners Inc (ROAD) has a backlog that grew year over year by 11% organically, AECOM (ACM) has a US backlog that is up 7% year over year, and Jacob’s Solutions (J) has a backlog that is up 18.9% year over year. If Peter Boockvar is correct and state and municipal spending are shrinking, it’s not showing up in road projects.

Important to CTOS is that Everus Construction Group (ECG), a spinoff last November from MDU Resources Group (MDU), has a backlog growing 38% year over year organically. ECG is much more exposed to the power grid maintenance and expansion.

I think the reason why Boockvar might be off is that it takes so much time between when government money is allocated to a project until the time that those projects actually begin construction. The projects being built in 2025 are the ones whose budgets were allocated when state and local infrastructure spending was much higher. And it isn’t obvious that state and local spending should slow down anytime soon. During Covid, home sales at new peak prices locked in higher property taxes, and the massive inflation spike de-levered municipal balance sheets in real terms. The states and counties can now issue new debt on top of their higher tax base, and that debt can be used to fund infrastructure projects for years.

So I remain confident in my prediction that 2025 will be a good year for the equipment dealership businesses ALTG and CTOS. And perhaps more importantly for the rest of the portfolio, construction employment is a strong leading indicator of recessions. Well, how close can we be to a recession when engineering firms have an 11% to 38% organic increase to their 2025 backlog compared to 2024? I think we won’t see construction employment weaken to signal a recession warning anytime soon.

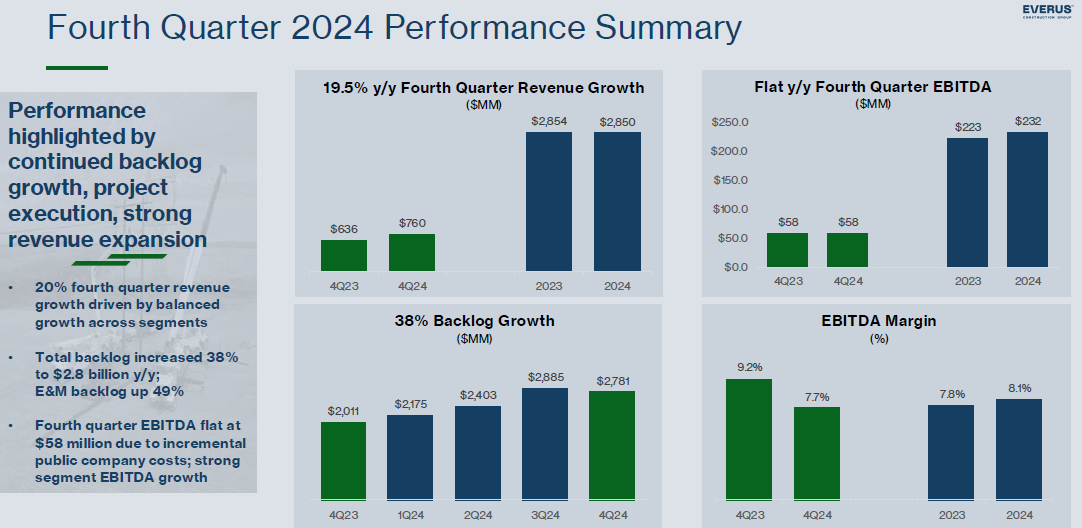

Everus Construction Group (ECG):

But now on to looking at Everus Construction Group (ECG) more specifically. Even in a sector as unattractive as engineering firms, there is usually something undervalued. Since ECG only spun off from MDU last November, the market hasn’t had much time to value them appropriately, especially since small cap stock prices have been falling since… last November. It looks like the spin off was a 100% distribution of equity, with MDU not retaining any stake in ECG. One possible reason for this is that potential clients don’t wish to be the customer of their direct competitor, and MDU believed that ECG would be able to win more contracts without the MDU affiliation. So far there have been three insider purchases, two from directors, and one from the CFO.

I place a lot of weight on inside purchases from a CFO. The amount is relatively modest, but they are from someone who has all the numbers, and is typically a pessimist by nature. Inside purchases from a CEO carry a bit less weight for me personally, optimism is a trait that makes for better leaders, but it clouds judgement. The CEO is allowed to drink his own cool-aide, but the CFO is not.

ECG currently trades for about $1.8 billion, with $2.8 billion in 2024 revenue, and guidance for between $3.0 and $3.1 billion of revenue for 2025. Despite very mediocre profit margins, engineering firms typically can trade for 1.5x to 2.0x price to sales, or 20x to 30x price to earnings. I wouldn’t typically go out of my way for a thin margin cyclical business, but investors like the capital-light nature of the business, the barriers to entry that come with technical expertise, long term relationships with clients, and potentially long-term contracts with utilities and governments. Even after falling 30% from the November highs, Construction Partners (ROAD) is trading at a price to sales of 2.0x, and a price to earnings of 66x.

ECG had $2.8 billion of sales in 2024 compared to ROAD’s $1.99 billion, and they both have the same operating margins at the moment. ROAD has higher gross margins, but ECG has higher profit margins for 2024. Otherwise, it’s hard to tell the two apart, except that ECG has the better claim to the hype of the Artificial Intelligence revolution and the data center buildout with their expertise in expanding and hardening the grid.

ROAD has higher historical growth for the last five years, but ECG has 20% revenue growth for their last quarter, and a 38% year over year increase in their backlog. We don’t know what kind of a growth rate that ECG will be able to sustain as a standalone entity apart from MDU, but ECG can now concentrate their focus, and can take on MDU’s competitors as clients where they likely couldn’t before.

Also, ECG mentioned on their last earnings call that growth through acquisition is a top priority now that they are a standalone entity. They have a relatively clean balance sheet with only about $321 million of debt, and a guidance for $210 to $225 million of 2025 EBITDA. Based on management’s desired leverage ratio, ECG will probably rush out and spend around $200 million on acquisitions in the near future.

Following ECG forward in time over two years, I would expect to see a company with around $3.5 billion in revenue, assuming $200 million of organic revenue growth and $200 million of revenue growth through acquisitions. If it trades at 1.0x sales, that would be a $68 stock. If it trades at 1.5x sales, that would be a $102 stock. And if it trades at 2.0x sales, where ROAD trades today, that would be a $136 stock. That’s not too bad for a company that trades for $36.18 today.

I am not an expert on engineering firms by any stretch of the imagination. But recent spinoffs are often mispriced, and ECG has a specialization and focus on engineering for the power grid, which has a secular tailwind for at least the next ten years. Electricity demand in the US was flat for 20 years in the era of globalization as our factories shut down offsetting population growth. Now with reshoring and the AI revolution, the grid needs to grow for the first time in decades, and Everus Construction Group is here to surf that wave.

Everus Construction Group (ECG) $36.18: $102.67 by the end of 2027 (1.5x price to sales)

I really like your writing style and approach. At some point, it would be interesting to hear you do a pod on what is under the hood in your work to get to the informative distillation in your articles. I'm sure tons more work. Thank you

The word you were looking for in the first paragraph is jibe, jive is a type of dance.