Cutting the Gordian Tariff Knot

Oh no, not macro musings!!!

My apologies for macro musing and delving into geopolitics, but sometimes I just have to do it. My highest degree is in economics, and the conversation around Trump’s tariff announcement was too hysterical to leave it alone. Tomorrow I will return to my usual duties of writing about undervalued small cap stocks.

The Announcement:

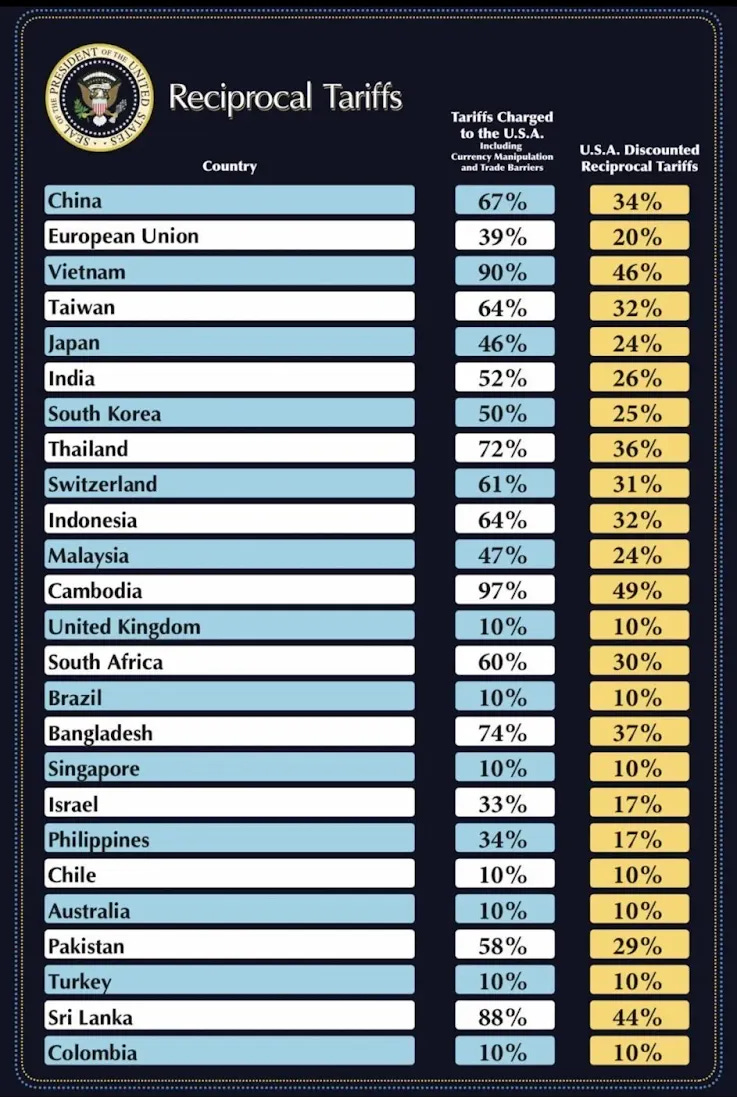

There seems to be a narrative floating around that Trump’s execution of reciprocal tariffs is some sort of failure due to the way he is calculating the effect tariff rates. I’m not sure how this narrative got started. Trump’s Council of Economic Advisors is basing their calculation on trade imbalances, rather than the data from the World Bank. For example, based on trade imbalances, the economic advisors say that South Korea has barriers to trade equivalent to 50% tariffs, but the World Bank says they are closer to 24%.

The complaints against a quick and dirty use of top-down trade imbalances as opposed to a desire for a bottom-up careful reconstruction of all tariff and non-tariff trade barriers must come from a place of ignorance regarding how impossible these numbers are to calculate. Consider the example below:

Let’s take a look at a single trade relationship, Canadian imports of US dairy. Canada has price controls on dairy products at the farm level, which is not totally unusual, the US has an abundance of agricultural programs and price stabilization measures as well. Every country has their pet industries that they want to protect, and it is the nature of government creep that over time, almost every industry becomes a pet industry.

Before the World Trade Organization, tariffs were the common form of protecting pet industries. Foreign competition was either priced out of the market entirely, or if the tariffs were moderate, raised revenues for the national government. After the creation of the WTO, governments still wanted to protect favorite industries, but they had agreed not to raise tariffs. So instead of tariffs, non-tariff barriers or import quotas grew in popularity. Canada has such an import quota on US dairy products.

One big difference between a tariff and a quota is that the revenues don’t go toward tax receipts, the profits go to the business that wins the quota. This becomes a vehicle for corruption, the business is willing to pay a lot to the bureaucrat in order to win a share of that quota. Of course in the US, the corruption is usually not as obvious as in countries like Indonesia, but how many bureaucrats pass through the revolving door and go on to be hired for enormous salaries at companies who were assigned a part of an import quota, and how many hours a week do those bureaucrats actually work in those new jobs? If we are really living through a moment of great change, one of the best changes would be to move away from quotas which are a vehicle for rampant corruption.

But back to Canada, who has an import quota on US dairy as follows:

Fluid Milk: 50,000 metric tons (MT), with 85% reserved for further processing.

Cheese: 12,500 MT, with 50% available for any kind of cheese and the remainder for industrial cheeses.

Cream: 10,500 MT, with 85% of the initial volume reserved for further processing.

Skim Milk Powder: 7,500 MT.

Butter and Cream Powder: 4,500 MT, with an initial reservation for further processing that decreases over time.

Concentrated and Condensed Milk: 1,380 MT.

Yogurt and Buttermilk: 4,135 MT.

Powdered Buttermilk: 520 MT.

Products of Natural Milk Constituents: 2,760 MT.

Ice Cream and Ice Cream Mixes: 690 MT.

Other Dairy: 690 MT.

Whey: 4,134 MT

Any quantities above this amount are subject to tariffs of between 241% for milk and 300% for butter. Those high tariffs are the prohibitive kind, not the revenue raising kind. But the bureaucrats who assign these quotas do so at their own discretion, and their discretion is to reduce US dairy imports to Canada. The import quotas are assigned to a handful of large dairy processing companies, who only order the lowest value goods, and likely at the request of the bureaucrats, do not purchase their full allotment of the quota. The International Dairy Foods Association claims that this reduces the value of the quota allotment to around 26% of its potential.

So I ask you, dear reader, what is the effective tariff rate on US dairy products in Canada? It is an unknowable counterfactual to estimate how much dairy Canada would import in a free trade situation, and without that comparison, how much trade is lost by the quotas and the discretionary implementation of the quotas? Is keeping American yogurt off the grocery store shelves the equivalent of a 23% tariff, a 37% tariff? It is a ridiculous question and an incalculable quantity. I posit to you that the effective tariff rate cannot be known. You could do an econometric regression to estimate it, but I wouldn’t place a lot of confidence in the answer. There are too many categories of goods and the reality on the ground is often different from the quota system on paper. The World Bank has their estimates on average tariff and quota impacts above, and they put Canada at around 3% tariffs and 15% total tariff equivalent barriers, but I know those numbers are bad, not because I am a partisan hack, but because I have peer reviewed research in Economics. We can still discuss these bad numbers in a rough fashion, but the narrative that Trump’s numbers are worse because of the way in which they chose to calculate effective tariff rates doesn’t carry much water once you see how the sausage is made. Still, the narrative that Trump’s team is incompetent has spread rapidly. Stephen Miran has his economics PhD from Harvard, and an undergraduate degree in Mathematics from Boston University. The Twitterati who find his estimates to be “ridiculous,” “an embarrassment,” or “a joke,” do not.

The Council of Economic Advisers, by making a top-down number that is based purely on the goods trade imbalance is putting the burden on the other country to figure out what kind of American products they are willing to buy. Rather than filing another complaint at the WTO that Canada is violating their quota agreement again, Trump is just telling them to figure out some American goods to buy, or else. The labyrinth of tariffs, non-tariff barriers, and selective bureaucratic enforcement of every category of trade good for every country in the world is a Gordian Knot. When the Phrygian king told Alexander the Great that whoever untied the knot would rule Asia, Alexander chose to cut it with a sword instead. I think that Trump just took a sword to Gordian Knot of intractable trade barriers.

Trump’s Likely Goal:

Taking the World Bank data, which is bad, but we can still use it roughly, the US has the lowest effective tariffs in the G20. Why? After World War II, the US took it upon itself to help rebuild the world, and we allowed other countries to charge us, without charging them back. Is Orange Man so bad for questioning whether this legacy charity program is appropriate in 2025 when we suddenly have a peer rival for the first time in a century? (I have searched through declassified CIA documents estimating the size of the Soviet economy, and even though the public believed the USSR was a peer rival, it most certainly wasn’t.)

Would it be so terrible if tariffs between G20 countries were equal? Trump takes it a step further and claims that other countries should pay us for access to our market, and our tariffs should be higher than theirs. He loses my support there, there is something about reciprocity that strikes a moral chord, and there is something about the bully pulpit that I find distasteful. But I am not naïve enough to insist that politics and morality overlap, I have read my Machiavelli, and I am comfortable in my armchair.

Even a move toward reciprocal tariffs is met by the legacy media as something that will plunge the global economy into darkness and chaos. I don’t know how much of this is due to fear of the unknown, and how much is due to the free-trade zeitgeist that has dominated the West for decades. But the fearmongering is way overdone. Using the World Bank’s estimate, which is bad but I use it anyway, if the rest of the G20 can have 10% to 25% effective tariff rates on the US without the global system falling apart, then certainly the US can have 10% tariffs on them as well. I’m not saying there won’t be some short term dislocations, but we did just spend years becoming supply chain experts.

Trump revealed his goal in his presentation today. Trump’s goal is for the US to have 10% revenue generating tariffs on everyone, and 20% on China because they are our peer rival. All the rest of the numbers are negotiable, and can be brought down to 10% if other countries make some concession to the US such as lowering their own tariffs against us, or whatever it is we need from them.

Some countries might be reluctant to make concessions to the US. Europe in particular might have a hard time exempting US goods from VAT. Does it make sense that US companies should fund the US government domestically through income taxes and then also fund the EU government through VAT? Well, the 50 states in the US have their own sales tax, some as high as 9.5%, so is the EU’s 21.8% VAT really so different? Will the EU demand that European goods be exempt from US state sales tax in exchange for exempting US goods from VAT? Will they split in the middle and have a 9% VAT on US goods to match our sales tax? Or does Trump just want some other concession in order to bring the tariff rate down to 10%, such as placing a certain number of orders for new F-35s or committing to opening a certain number of factories in the US? I think we will see the EU come up with some ideas of what they can do, in fact they already started working on it.

Argentina has the highest tariff barriers in the G20, and Trump gave Argentina an effective rate of 10% just based on the relationship with Milei, and the belief that Milei is currently working on reforming Argentina. Is it really so far fetched to believe that every country except China can have the flat 10% rate, if they just say nice things, come to Trump and kiss his ring, and make some token effort to cooperate with the US’ goals?

The Results:

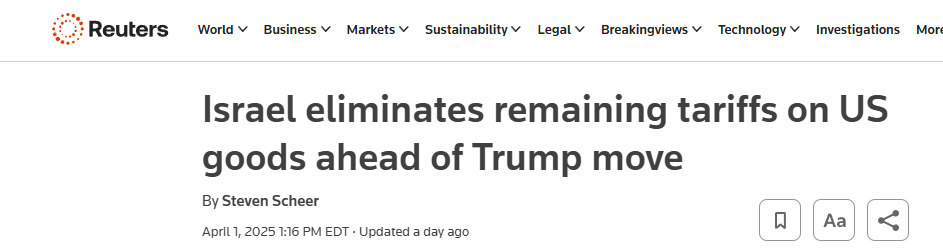

Other countries not being run by total idiots have already picked up on this and are taking action.

Two down, about sixty countries left to go. There are only about sixty countries with a GDP big enough to matter; Israel and Vietnam are numbers 29 and 32 respectively. As I took a break before proofreading this, Thailand just became the third country to step forward and come to the negotiating table, and South Korea is holding an emergency meeting to figure out a plan.

It is also worth noting that there are several industries which are exempt from the tariffs, of particular note are semiconductors, copper, and critical minerals.

The consequence of Trump’s reciprocal tariffs will probably be a long parade of global leaders flying to Washington DC to negotiate a reduction in their own tariffs and quotas against US goods. I think that Trump made it very clear that anybody except for China can have the 10% flat rate if they want it. And again, the burden is on them now to figure out just which American goods they are happy to buy, we don’t have to sue at the WTO over every unfair practice, the number of which are uncountable and all countries are guilty of them.

Is it likely that other countries will increase tariffs against the US in retaliation to Trump policy? I think Trump is trying to avoid this by pointing out that other countries already have much higher trade barriers on the US than the US has on them, and by making the system formulaic, that US tariffs will increase proportionately if the other country retaliates and their trade imbalance increases.

Canada and Mexico were not a part of this big tariff reveal, they are being handled separately. Surprisingly, Canada is the most belligerent towards this new US tariff policy, despite our close relationship and long history; Doug Ford saying that he will cut off electricity to upstate New York, Chrystia Freeland saying that Canada should ask the UK for nuclear weapons, and Mark Carney saying that our relationship is over. Well it’s not very neighborly to have 15% tariff barrier equivalents on the US either (again using bad numbers even when I know that they are bad and are directionally correct).

Just playing armchair psychologist, anger is really easy to misdirect, and Canadians are angry that their GDP per capita is almost flat since 2007. Canadians have always thought of themselves as better than Americans, and it’s unsettling to learn that their economy is stagnant, their banks are laundering money for Chinese organized crime, and the cartels have built fentanyl fabrication labs on their soil.

Geopolitics:

The recent meetings between China, Japan, and South Korea are touted by some as a failure of Trump’s trade policy. I think it reflects something deeper. In a world with only one great superpower, smaller countries could pretty much do whatever they wanted and court relationships with whomever they wanted. But in a multipolar world of two competing superpowers, it becomes increasingly important for each superpower to control their immediate region.

China will be focusing on gradually bringing Japan and South Korea into the Chinese sphere of influence, and the US will probably abandon Asia eventually and escalate the Monroe Doctrine in North and South America.

While I have a fondness for Canada, I grew up in Maine, maple syrup was always a special treat, and I always loved finding a Canadian penny mixed in with my pocket change, the US cannot allow their Northern neighbor to harbor Chinese organized crime syndicates, launder their money and manufacture their fentanyl. The Canadian public might be angry, and they might be misdirecting their anger against the US as opposed to themselves for keeping Trudeau in power for so long, but if whoever wins the next Canadian election doesn’t come completely into the US sphere of influence there is a real possibility that Canada will suffer under the full effect of tariffs. Since exports to the US is 25% of Canada’s economy, and exports to Canada is 1.8% of the US’ economy, the suffering wouldn’t be even. Canada would suffer about ten times as much as the US would suffer from that trade war. But Canada is probably the trade war that is the most likely to escalate, because the US cannot back down, controlling their neighborhood is an existential risk.

This isn’t a reflection of what I think should happen, this is my realpolitik interpretation of the consequences of the multipolar world. And you can already see the steps being taken in this direction with Trump’s emphasis on kicking China out of the Panama canal, and securing the Northern Passage via Greenland. I also believe that Trump is doing whatever he can to get put into history books as one of the greats, and I don’t find that personal ambition particularly admirable. But I suspect that the emphasis on the Panama Canal, Greenland, and Canada has more to do with realpolitik than to do with his ego.

The Criticism:

Trump is being criticized for his use of goods trade imbalances only, but the US is a service based economy, and the US exports a lot of services all over the world. This is going to throw off the goods trade imbalance calculations. Well, Trump is the champion of the blue collar man, so if his goal is to re-shore manufacturing, then why not focus on only goods? It’s not an accurate measure of the total trade imbalance, but it is an accurate measure of the problem that Trump wants to address. Also, it probably doesn’t really matter if the number is accurate, the goal is 10% revenue generating tariffs, and all the other numbers are there to get governments to come to the negotiating table and make concessions.

The other criticism is that focusing on trade imbalances ignores the effect of foreign investment. If a foreigner receives US dollars in exchange for exporting goods to the US, he has to spend those US dollars somewhere. Ignoring services, if he doesn’t buy US goods, he will probably invest in the US. Foreign direct investment is typically seen as a good thing, we want an accumulation of capital stock to drive up our own wages. Even passive investment, buying the S&P 500, drives up stock prices for the 401K retirement balances of wealthier Americans.

However, nothing happens in vacuum, there are three other major trends that contributed to the hollowing out of blue collar wages over the last two decades. The first is illegal immigration. Average wages are capital per capita, overhead per head. When the capital is diluted with more people, wages go down. The second is closed union shop laws. One would think that increased investment in the US should lead to more manufacturing, and it did in the Sun Belt. From 2019 to 2023 Florida added 37,000 manufacturing jobs, and Texas added 49,000 manufacturing jobs, all while Michigan lost 12,000 manufacturing jobs, and Ohio lost 13,000 manufacturing jobs. The entire narrative that globalization hollowed manufacturing in the US is mostly a bias of what is seen vs what is unseen. The empty textile factory is an eyesore, it is noticeable, and globalization takes the blame, but the Hyundai factory in Alabama is taken for granted, and those excess dollars in South Korea from our trade imbalance doesn’t get the credit for funding that factory.

And the third cause of the hollowing out of the blue collar economy was the zero interest rate policy. If you listen to resource executives talk about the period from 2003 to 2005, they will tell you that they got a lot done, and it is amazing how many mines got build at a cost of capital of 9%. This isn’t an accident. The net present value of a project is affected by the interest rate, and lower interest rates make projects more valuable, but not equally. Friedrich Hayek called this “both ends pulling against the middle;” the longest term projects, silicon valley venture capital, and the shortest term projects, shale oil, are much much more attractive than medium term projects. At zero interest rates, we got lots of silicon valley venture capital, and a shale revolution, but no new mines, no new offshore drilling, and few new factories.

So I would point to three conflating factors that helped to destroy American manufacturing, but as I said before, anger is easy to misdirect. There are an awful lot of blue-collar folks in flyover country who have a family member who lost a job when a factory closed. I had three uncles become unemployed when a factory closed in a town of 10,000 people. That particular factory closure wasn’t due to globalization, those products are still made in America, but my Uncles don’t know that.

So the biggest criticism of Trump isn’t that his tariffs are crazy, or his calculations are wrong, it’s that he’s slaying a dragon that probably doesn’t even need to be slain. If we had twenty years of moderate interest rates, low and legal immigration, and right to work states, we could easily have built more new capital-intensive factories to offset the old labor-intensive factories that went overseas, and blue collar wages could have risen the whole time.

Conclusion:

As I write this the futures markets are all down between 2% and 4%. I had anticipated a sell the rumor, buy the news event, especially after his last month of the market selling off. There is a lot of uncertainty leaving the market, especially as Israel, Vietnam, and Thailand have already come to the table to make sure that they enjoy only the 10% minimum tariff. Most countries, I believe, will follow suit. Over the next few days, the market should come to realize that end result of the tariff situation is that most countries will make some concessions and have a 10% tariff, and that isn’t enough of a disruption to crash the market. I could be wrong, but we just saw prices move 40% from the Covid lockdowns, we can easily digest 10% price changes and the substitutions effects that follow.

Meanwhile, the 10-year treasury just fell from 4.2% to 4.05%, which is a huge part of Trump and Bessent’s plan to lower the interest expense of the outstanding debt. This could provide an excuse for the Federal Reserve to end Quantitative Tightening, and possibly to cut rates at the next meeting. The odds of a May interest rate cut were down to 10%, now they are back up to 25%. The chances that we see a 3.5% 10-year treasury, which unthaws the housing market are getting better and better. If consumers can access their home equity at attractive rates, I think the economy will be running very hot.

So the selloff might continue for tomorrow, or dip buyers might start to come back in when cooler heads prevail. But I wanted to set the record straight regarding the many criticisms floating around about Trump’s reciprocal tariff announcement. His data isn’t that bad, his plan isn’t that bad, and the US economy probably not hurtling toward an imminent recession.

I'm not surprised about Canada being the most angry. You left out the whole part where President Trump threatens annexation and degrades the Prime Minister to a Governor in his speeches.

Also the argument on VAT needs some expanding. You make it sound like its a tariff which is wrong.

An disappointingly unbalanced take from you but certainly a new view for me.

Regards, a guy from Switzerland.

Personally I think the equivalent tariff is just mislabeled... And should really be trade imbalances and the reciprocal tariff is just the rate the make it balance... If that's what he said, then no one would be laughing at it.

Though this flies in the face of comparative advantage and probably a worse quality of life for everyone in the long run.