“Curse Your Sudden But Inevitable Betrayal” - Navios Maritime Partners Investors Probably: $NMM

Those knives, they keep a falling

“Timeo Danaos et Dona Ferentes”

”I fear the Greeks even when bearing gifts” - The Aeneid by Virgil

Thank you to Judd Arnold of Lake Cornelia Research who went public with their research on Navios Maritime Partners LP (NMM) this past June. I first came across Lake Cornelia with their work on Tidewater (TDW), but at the time, I preferred Transocean (RIG). If I were less set in my ways, Lake Cornelia was correct in their assessment that TDW would benefit before the other offshore names due to their very short contracts. Since releasing their writeup on NMM, with this recent selloff in shipping, NMM prices are now below where Lake Cornelia originally wrote about them, but hey, that can happen to anybody. I won’t be throwing any stones from my glass house.

You can listen to Judd Arnold from Lake Cornelia on the Value Hive Podcast with Brandon Beylo here:

Whenever a stock is so hated that the valuation is low, I have to ask myself why. In the case of Navios Maritime Partners LP (NMM), there are an abundance of reasons, but are they all still lingering?

First off, Navios Maritime “Partners LP,” NMM LP, is a Limited Partnership, but it chooses to be taxed as a C corporation. This means that shareholders do not receive a K-1 form, but instead receive a typical 1099-Div form. As a Limited Partnership, NMM can choose its tax treatment, and the risk is always there that they could switch back to tax passthrough treatment. They probably won’t switch back, but they could, which means that it could someday create an unpleasant surprise for someone with a large holding of NMM in a tax sheltered IRA account, as once you reach $1,000 of a very specific kind of income through an LP, you could risk having to pay taxes from your tax sheltered account, which people hate with a burning passion. I would love to promise that NMM would never do this, but this is shipping, and in shipping, betrayal is always an option.

Secondly, did I mention that this is shipping, and betrayal is always an option, especially from the Greeks? That’s not my original opinion, people who have invested in shipping for a long while have all lost money to a Greek at some point. Greek shipowners and managers have a reputation for choosing themselves over their shareholders. Fiduciary is a Latin word after all, maybe the Greeks just aren’t into it. But in the case of NMM, founder, CEO, Chairwoman, and 16.75% owner Angeliki Frangou has a reputation of engaging in complex transactions and corporate structures that left people burned. Are the days of Angeliki’s questionable behavior behind her? Maybe, but this is shipping, and betrayal is always an option.

In defense of Mrs. Frangou, the transactions that left people feeling burned revolved around the shipping bear market which lasted from about 2012 to 2020, depending on the type of shipping. During this time, there were several different Navios companies, one for tankers, one for containerships, and one for dry bulk. The transactions to consolidate these companies into one, the current NMM, could be argued to have been a slow rolling bankruptcy. Investors would have lost money in just about any outcome, but there is no shortage of shipping investors who feel a special personal bitterness toward Angeliki Frangou.

The real question is, will she abuse shareholders again? It’s possible, did I mention she is a Greek shipowner? But all jokes aside, Angeliki has Incentive Distribution Rights (IDRs) as the General Manager of NMM, and these IDRs are a bit like the performance based fees of a hedge fund, except larger but with a higher hurdle rate. Without getting too far into the nitty gritty, if NMM pays a quarterly dividend of $6.03, Angeliki gets no incentive distribution, but with escalations, if NMM pays a quarterly dividend of $7.87 or more, Angeliki personally gets to keep 48%. That is a powerful incentive, and on top of that, she has been buying common stock in the open market, bringing her ownership from below 5% after the restructuring to over 16.75% today. She got mostly wiped out as well during the slow rolling bankruptcy, but she had enough cash to buy back in afterward.

So, will NMM ever be able to pay more than $24 per share in annual dividends? The stock currently trades at $43.78, if so, that would be one heck of a transformation. Things have been moving for NMM, the stock price tripling since the fall of 2023, but now giving back much of those gains in this shipping price collapse since October. Again, I believe this is due to the market being overly pessimistic on shipping day rates once peace is achieved in the Red Sea and the Suez Canal is once again open for business.

In order to reach this target of paying over $24 of dividends a year, there are three likely stages of capital allocation policy; first deleveraging, second share buybacks, and third maximum cash distribution. So far, NMM is still in stage one, bringing their debt to equity ratio down from 0.7 in 2022 to about 0.5 today, all while engaging in an aggressive newbuild fleet refresh. Shareholders did not like it when NMM took out enormous debt in order to fund newbuilds, but now that the ships are arriving and the debt repayment has started to begin, things are looking a lot better, and are on track to keep on improving:

Management has the stated goal of reaching a net loan to value ratio of between 20% to 25%, and NMM is at 32.9% at the end of last quarter. And this goal will likely be reached before the end of 2025 as more newbuild ships are completed and can be counted as asset value, even if debt repayment is a bit slow. So stage one of the capital allocation policy is nearly complete.

Once debt ratios are reached, what kind of earnings is NMM capable of generating in order to buy back enough shares to start paying out $24 of dividends a year, and how long will it take to get there? So far in 2024, NMM paid out $4.6 million in dividends, and bought back 1.2% of the float for $18.3 million. This is a trickle at first, but again, NMM hasn’t hit their debt targets yet. Trailing twelve month revenues for NMM are at about $1.3 billion, and net income is around $386 million or about $12.89 per share. That’s a price to sales ratio of just under 1.0x, and a price to earnings ratio of 3.4x. But, with the newbuild orderbook, more ships are coming. And day rates are relatively low on these last few years of China weakness. This is one way of getting a huge exposure to China, without investing in the Chinese market directly.

The current fleet of NMM is 179 ships, 73 dry bulk, 50 containerships, and 56 tankers. The newbuild orderbook is another 8 containerships and 19 tankers, with two containerships to be delivered this quarter. There has also been second-hand fleet replenishment activities, with 8 older vessels sold so far in 2024, and 5 newer second-hand vessels purchased.

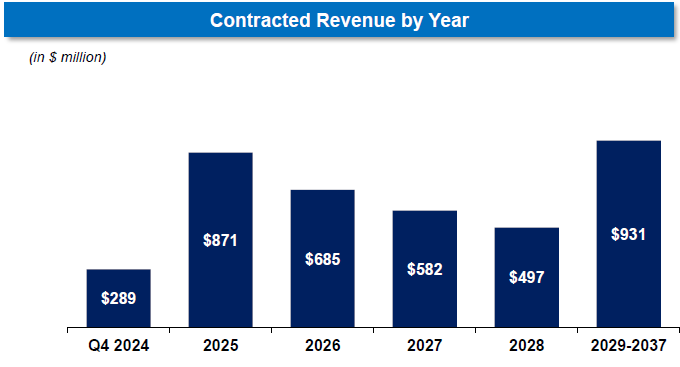

In my other writeups for shipping stocks, I talked a lot about the long term fixed contracts, as they significantly mitigate the risk of falling dayrates after the normalization of trade routes if and when peace is achieved. NMM has been balancing between fixed contracts and spot rates, for example, on their newbuilds, they routinely lock in five-year fixed contracts to derisk the upfront newbuild cost, but on the rest of the fleet, contracts terms are much shorter, usually between two and three years. NMM has a total contract backlog of $3.9 billion, or about 3x their trailing twelve month revenue.

This backlog is not equally distributed, and again, is primarily to offset the risk of the newbuild upfront cost, so the backlog is more heavily weighted toward tankers and containerships. Also, as the containership market is an oligopoly, longer term charters are more typical.

This strategy is very prudent, if and only if we really are in an environment of broadly rising day rates. And with China announcing that they are stimulating, and Trump rubber-stamping all permits for investments over $1 billion, we just might be heading into a global economic boom, ex Europe. If we are heading into boom times, day rates for shipping all have the capability of spending several years at many multiples of the current rates. This is caused by the large amount of time that it takes to build new ships. Take a look at the Baltic Dry Index, one measure of dry bulk prices:

One advantage of having exposure to three sectors, it is a bit like spreading your chips across the roulette table, there is an increased chance of getting lucky. It’s hard to know exactly which shipping sector will have a day rate squeeze, but in NMM, you can get lucky if that happens in containers, tankers, or dry bulk.

However, there is a well established conglomerate discount, investors prefer to execute their thesis in a pure way. This is another reason NMM is cheap, over $140 of net asset value for a $43.78 share price. But the conglomerate discount never really goes away, the only hope for a multiple rerating would be if NMM consistently delivered results good enough for people to forget how much they hate Angeliki. This process has already begun, with the runup from $20 to $65 and back down to $43, the price to sales ratio increased from about 0.5x to 1.0x, and the price to book ratio increased from 0.26x to 0.45x. The price to earnings ratio is up from about 1.5x to 3.3x. So time really will start to heal all wounds after all, even the hate that shipping investors feel for Mrs. Frangou.

As a shareholder in NMM, you can have returns in a number of ways. First, any one of the three sectors could have a several year long price squeeze. Second, the multiple rerating of NMM has already begun, and has a lot of room left to go. Third, the progression to stage two of capital allocation, aggressive share buybacks, followed by stage three, aggressive dividends. And fourth, the newbuild program has already been partially paid for, but 27 ships are still yet to be delivered, increasing book value per share on delivery.

In conclusion, Navios Maritime Partners, NMM, is a very interesting lottery ticket on three different sectors, and it has very decent odds of performing very well, even if the roulette wheel doesn’t come up with a price squeeze. It might take three to five years or longer for NMM to buy back enough shares for Mrs. Frangou to realize her $24 annual dividend, but NMM would be a pleasant stock to hold in the meanwhile. While past investors might feel that management abused them, the current incentive alignment is very strong, with the founder buying over 10% of the company in the open market, and the Incentive Distribution Rights that might be guiding the overall NMM strategy. Do I like it enough to buy any shares of NMM when I could buy more Höegh Autoliners (HAUTO.OL) instead? At this moment, no. I have been looking for a dry bulk name for a while, and I am glad to have found NMM, but I won’t be buying any until I own so much Höegh that I can’t stand it anymore. Maybe this is a sign that the seduction of quality is slowly starting to creep into my thinking. Höegh doesn’t really have anywhere near the lottery ticket potential of NMM after all. Or maybe these last two weeks of value selling off have left me temporarily shell-shocked. If the price of NMM continues to fall, I will be tempted, and I wouldn't fault anyone for buying it here. NMM still has a trailing price to earnings ratio of 3.4x and earnings growth projected for next year, the average analyst estimate for 2025 earnings puts the forward price to earnings ratio at 2.44x!

How value investors transition to quality investors, the seduction of Jackson Financial $JXN.

“I wanna tell her how hot she is but she’ll think I’m being sexist. She’s so hot, she’s making me sexist. Bitch.” - Flight of the Conchords

AF is cold blooded AF, but it seems like those IDR’s line up nicely with shareholder incentives.

Buffet’s lesser known 2nd rule: never trust the Greeks.