Coming to the nuisance with Burford Capital $BUR. What is going on?

A Fintwit Favorites Series

What do you call a hundred lawyers on the bottom of the ocean? A good start.

What do you call a hundred lawyers headquartered in Guernsey and treating lawsuits like investments? Burford Capital (BUR).

Burford Capital is a founder-led international corporate litigation finance firm which for the last fifteen years has been financing large corporate lawsuits, $30 million average size. They use a buy and hold strategy because there is no secondary marketplace to sell half-finished lawsuits. They use not only their own money, but they also have external investors whose capital they deploy for a management fee alongside their own capital. A Saudi family office as a major shareholder gives them practically unlimited pockets if they can find the deals. Their current litigation portfolio stands at around $7 billion, and they do about $1 billion a year of new business. The CEO and CIO are cofounders, own about 4% of the company each, and occasionally buy more shares on the open market. There is also occasional insider buying from other corporate officers.

Corporations seem eager to use external capital in order to finance their lawsuits as typically investors do not put any value on pending litigation. By outsourcing to BUR, corporations can preserve working capital and Burford can use their expertise and their capital to earn a percentage of the winnings from the lawsuit. The main source of their value added comes from expertise in predicting the outcomes from potential lawsuits in every jurisdiction and for every type of corporate litigation in the world.

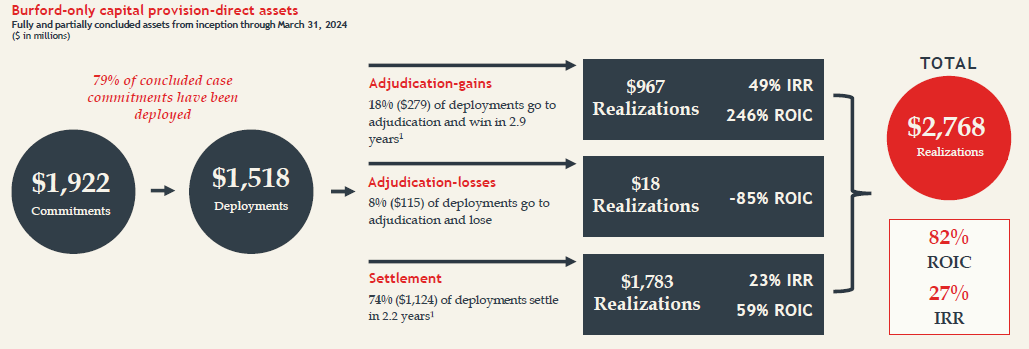

Since inception in 2009, BUR has achieved realization on $1.5 billion of deployed capital which resulted in a return of $2.7 billion. About 74% of lawsuits are settled out of court, and for those the average duration until settlement was 2.2 years. About 18% of cases were tried and won, and the average duration until a court victory was 2.9 years. The remaining 8% of cases were tried and lost. The duration is about to increase on average as Covid has caused an enormous disruption to this industry. With the increased duration, the 27% IRR may be a less useful guide than the 82% ROIC.

During Covid, we were all exposed to just how diligent and hardworking civil servants can be. Video recordings of public school teachers holding their lectures from a beach in Puerto Rico went viral. Court systems around the world shut down, and years of pending litigation were frozen in time. Most jurisdictions are trying now to clear their backlog, and are doing so in a two pronged approach. New cases are moved to the front of the line and handled as before Covid so that new litigation isn’t given a huge delay, and the backlog of cases is being worked through as quickly as public servants are able or willing to do so. For BUR this means that they under-earned substantially during Covid, but since have entered a time period of dramatic over-earning. If the results of $1.5 billion deployed capital were a return of $2.7 billion, then the current portfolio of $7 billion worth of cases if worked through over the next two and a half years, could generate about $12.7 billion of inflows for this $2.8 billion market cap company, if success rates hold. But then earnings should drop off dramatically after that as the business returns to a normal run rate.

Regarding the 74% of lawsuits that are settled out of court, the results of these settlements are confidential, which means that large participants in the litigation market have proprietary data for the accurate prediction of the outcomes of new lawsuits. The market leader just gets better and better over time. BUR has been using data science since 2017 to better anticipate the outcome of potential litigation. Management claims that this will lead to a reduction in the 8% of BUR’s cases ending in a loss in court. It’s always healthy to be skeptical of management’s promises, but the confidential nature of court settlements lends credence to the idea. There are peer competitors of size in the litigation finance business, but not publicly traded. BUR is the publicly traded market leader with the only other publicly traded competitors being Litigation Capital Management LIT.L with a market capitalization of 10% of BUR, and Manolete Partners MANO.L with a market capitalization of 5% of BUR. Since I avoid microcaps, BUR is the only game in town for this niche market for me.

Is this niche market worth participating in? Well, the timing of litigation coming to completion should be uncorrelated to market phenomena. Unlike Private Equity which needs a bustling capital market to have their exits, litigation finance can have big paydays even in down markets. This potential of uncorrelated returns is extremely enticing to portfolio managers, so the eventual multiple received could easily outdo any expectations. The stock price is half of where it was at the 2018 peak, and in 2018, revenue was half of 2023. Unlike most of the degenerate garbage I am usually attracted to, this has the potential to reach a Price to Earnings ratio of 20 or higher. And even off of the peak, the stock price has compounded at 26.6% annually for the last 10 years, matching the 27% IRR of their litigation outcomes.

Stock Price of BUR.L since BUR was dual listed in 2020:

Now for the juicy part:

BUR became a FinTwit favorite when it was announced in September of 2023 that a New York judge found against Argentina in the nationalization of an energy company, YPF Sociedad Anonima (YPF) and awarded damages of $16 billion. However the case is still under appeal with an estimated timeline for the conclusion of that appeal being sometime in 2025. If Argentina’s appeal fails, BUR’s portion of the $16 billion is described by the CEO as “considerable,” and estimated to potentially be somewhere between $1.4 billion and $6.2 billion depending on the news source. The market cap of BUR sits at $2.8 billion, for comparison.

The new president of Argentina, Javier Milei, has made statements that indicate he intends to pay BUR in order to reinforce rule of law, however his government is still appealing the verdict anyway. The market cap of YPF is only $10 billion, and the Argentine government only owns 51%, so it’s hard to say exactly how much will be recovered and in what timeframe if at all. On announcement of the initial ruling, BUR’s stock price doubled, but has since retraced 30%, possibly due to the market being unable to calculate the odds of this major outcome. But, even without YPF, BUR is compounding at 27% and has raised debt to put a turn of leverage on top of that 27%.

From my point of view, a founder-led business with insider buying that compounds at 27%, has a chance to double in a multiple rerating, has an enormous backlog about to be pushed through the system, and has an embedded $6 billion lottery ticket is one hell of an investment.

My only criticism would be capital allocation, the share buyback program appears to be just enough to sterilize executive stock grants, and not a penny more. The dividend is variable, perhaps to encourage a risk sharing investor base. That sort of capital allocation doesn’t lend itself to higher multiples. But, given the extremely unpredictable and volatile nature of litigation cashflows, and the under-earning during Covid, it is not the worst capital allocation I have ever seen.