Bloody Friday and 2024 Q4 Earnings Update Part II: $HBM, $BTU, $HCC, $JAKK, $MTLS

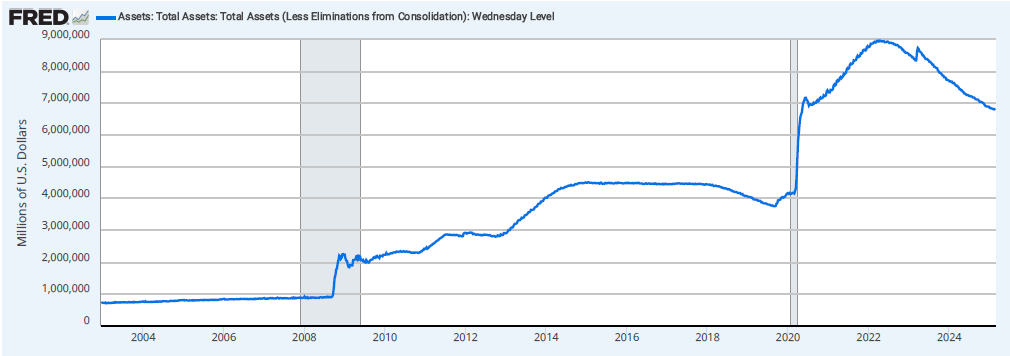

The market feels like it’s looking for any excuse to sell off. Companies with very moderate earnings, or even somewhat positive earnings, are rewarded with double digit collapses. I believe that the reason for this is the recent inflation data, employment data, consumer sentiment data, and the Federal Reserve minutes which have convinced the market that the Fed has officially paused rate cuts. The benchmark interest rate for the market is the opportunity cost, and if interest rates are going to be higher for longer, then stocks would need to be a bit lower. Not only do I believe that the market is wrong to think that the Fed has paused, but the Fed has also just signaled that they are about to pause Quantitative Tightening.

The reason I believe that the Fed will continue with rate cuts is that we are in a global cutting cycle, and if the interest rates in the US and the rest of the developed world diverge too much, it risks financial stability. I know officially the Fed has a dual mandate, but when you add financial stability, it’s more of a triple mandate. The EU is at 2.9% with the market projecting a terminal rate of 2.1%, Canada is at 3.0%, South Korea is at 3.0%, China is at 3.1% and announcing stimulus, and even though the UK and Australia are at 4.1% and 4.5% respectively, the US cannot stand alone against the cutting cycle without consequences.

Both Trump and Bessent have stated recently that they are focused on bringing 10-year treasury rates down. Elon Musk has mentioned interest rates on Tesla earnings calls as a primary reason for slow sales. The consensus of the marketplace seems to be that these three gentlemen will not be successful in lowering interest rates. The least accomplished of the three was the leader of the team that made $1 billion breaking the British Pound with George Soros. Why are people underestimating them? It boggles my mind.

Regarding the end of Quantitative Tightening, I think a lot of market participants are surprised that the Fed was able to reduce their balance sheet by over $2 trillion without crashing the market. Depending on how QT ends, whether Mortgage Backed Securities are maintained or replaced with treasuries, we might enjoy either a lower 10-year treasury or tighter mortgage spreads later this year.

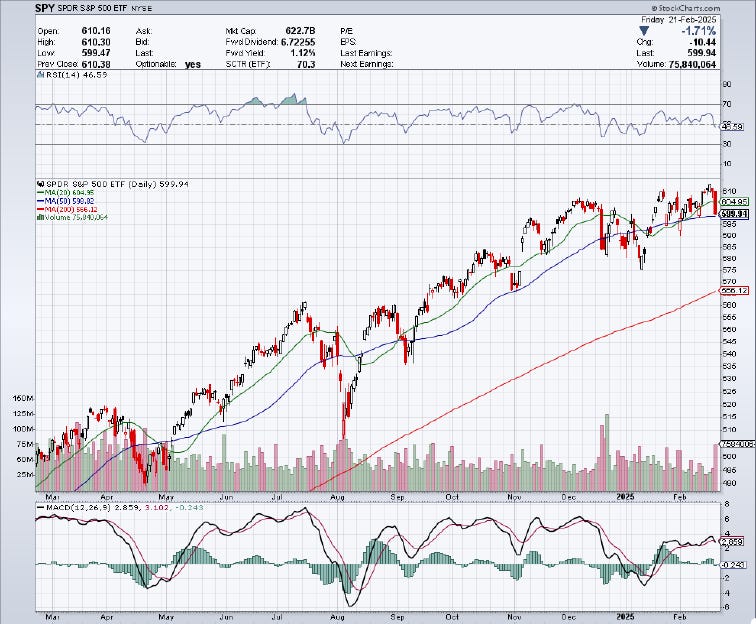

But this is a market that shoots first and doesn’t ask questions. Almost every earnings call results in a massive selloff. As for Friday in particular, it was painful, but it was orderly. With options expiration and a market driven by algorithms, the indices sold off, but only to important resistance lines. The S&P 500 is resting perfectly on the 50 day moving average, and the Russell 2000 is resting perfectly on the 200 day moving average. It’s what you would expect from a market dominated by computers programmed to take those thresholds into consideration.

The S&P 500 looks a lot better than the Russell 2000, but that’s hardly a new phenomenon. While January was starting to make me wonder if 2025 would be the year that small caps outperform, it looks more as though it was just the effect of investors re-entering positions after tax-loss harvesting the month before.

As investors take the weekend to look for bargains, the most likely path forward is for the market to retrace some of this selloff on Monday from dip buying. But if Monday isn’t green, I would start to be worried about the possibility of a bigger correction if these resistances are violated.

Hudbay Minerals (HBM):

Hudbay Minerals sold off from $9 a share to $7.15. There are two things here that might be driving the selloff, first is the projected All-In-Sustaining-Cost (AISC) of mining copper in 2025, $2.25 up from $2.00 originally projected for 2024. It should be noted that during 2024, guidance was lowered from $2.00 to $1.75, and the final number came in at $1.62. This current management team is an operational efficiency powerhouse. But it is the perennial problem of mining that costs always go up over time. If you own HBM, it’s because you believe that copper prices will go up more in the future, as I do.

The second reason that the stock might have sold off is the production guidance. Management is guiding for lowered production in 2025 than in 2024. This is due to the decline rate of a satellite pit, Pampacancha, which gave the Constancia mine in Peru a three year boost of production. As that satellite pit declines and is exhausted by Q4 2025, production at Constancia reverts to the normal 18+ year life run rate. Even though production is increasing at Copper Mountain and Snow Lake, Pampacancha’s decline was even larger. I feel the market is short sighted on this selloff because even though the projected production declines by weight, given the recent move in the gold price, revenues and profits should increase. For 2024, management guided toward 263,000 ounces of gold mined, and the average market price that year was $2,386. For 2025, management is guiding toward 247,000 ounces of gold mined, and the market price is already $2,950. Would you rather have $627 million or $728 million?

HBM has been stockpiling cash, and is extremely close to their stated target for starting development at their new mine, Copper World. They have acquired all permits, and promised shareholders that they would not start development until they had $600 million of cash in hand. Today HBM has $582 million. There is still some legwork for acquiring project financing, a JV partner, and selling a royalty stream, but it seems as though Copper World isn’t as far away as it was when I first bought some shares of HBM.

I did not create a price target for HBM when I first wrote about them in June of 2024. But at current copper prices of $4.56 per pound, gold prices of $2,950 per ounce, and silver prices of $32.81 an ounce, 2025 revenues should be between $1.9 billion and $2.4 billion. Any increase in metals prices would improve those results. HBM trades at a price to sales ratio of 1.36x, but it has in the past traded at a price to sales ratio of over 3.0x. From today’s price, HBM could be a double on multiple rerating, or much more if commodity prices rally.

Peabody Energy (BTU) and Warrior Met Coal (HCC):

Both Peabody Energy and Warrior Met Coal sold off on earnings. Of course this is due to coking coal prices, which are down right now. This is the nature of cyclical commodities, they go up and down. Peabody is especially hated as the market did not like their recent acquisition. But the selloff in Warrior Met Coal was surprising as that company has a management team which is much more aligned with shareholders. Again, this is a market that sells first and asks questions later, or never.

Commodity investors have told me time and time again, commodity markets are not forward looking. While we are accustomed to the stock market looking six months ahead or more, this is not the norm for commodity spot prices. China is stimulating, India is growing at 7% per annum, Trump is in the Whitehouse, and coal is making new 52 week lows. The prices aren’t generational buying opportunities like they were in 2021, but I would be shocked if either company isn’t a double from here over the next two to three years. Of the two, Warrior Met Coal is the safer bet. But, Peabody has the potential benefit of domestic thermal coal production.

Peabody’s management claims that they were approached by multiple parties regarding the possibility of generating power for data centers. While I was initially skeptical that silicon valley would power a data center with coal, GE Vernova has stated publicly that their order book for natural gas turbines is full, and if they don’t have your order already submitted, you won’t get a new natural gas turbine until after 2030. I had initially predicted that natural gas could satisfy the increased power generation demand more easily, but if the data center buildout occurs as projected, odds are good that some of those data centers will be powered by coal.

I was recently listening to a podcast interview of

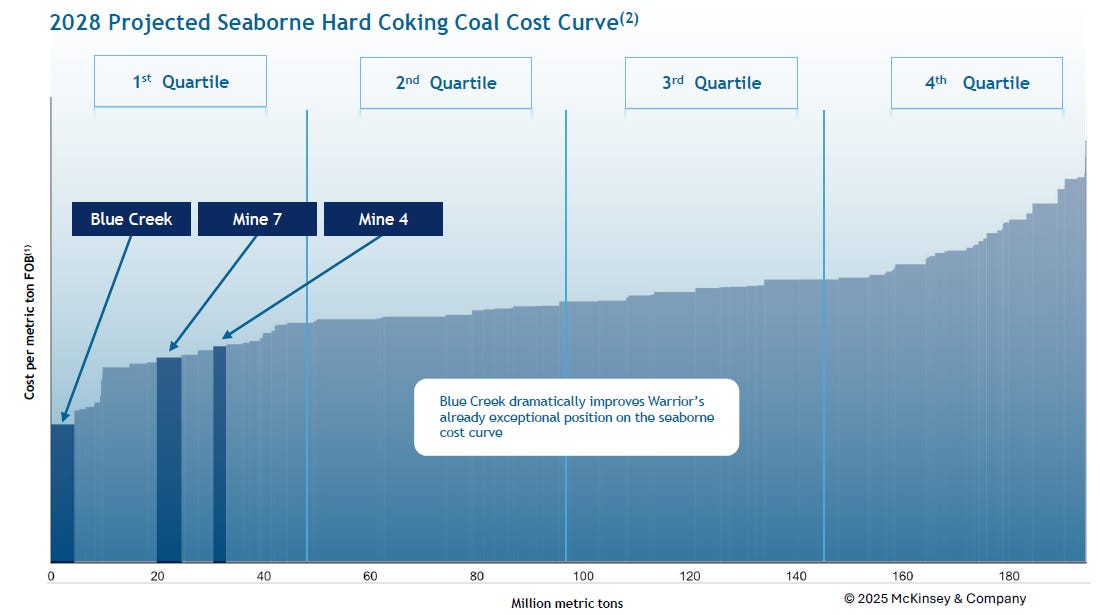

on ’s channel, and in it he gave a devil’s argument defense of Peabody’s recent acquisition. Peabody can’t control when those top tier assets come to market, and without throwing too much shade on management, it was understandable for Peabody to bid on them. As for the fear that multiple rerating will always be kicked down the road due to future delays of returning capital to shareholders from future acquisitions, there is no guarantee that large coal assets will be available to be acquired a few years from now. Peabody might not be my favorite management team, but I wouldn’t jump to the conclusion that they are a bunch of scoundrels.Warrior just released a presentation detailing their Blue Creek project under development. Aside from the shocking 35% IRR that Blue Creek is projected to deliver at $250 per short ton, one slide in particular caught my attention.

For those of us who are less degenerate, the strategy in commodities is to buy the lowest cost producers with low levels of debt. Without having the ability to forecast commodity prices, and knowing that commodities are cyclical, just buy the companies that will survive. With only $150 million of long term debt, and three mines that are in the 1st quartile of the cost curve, Warrior Met Coal (HCC) is the absolute best thing to buy. It may prove to have less torque than Peabody, but torque isn’t everything. If the way to beat the market really is to buy great companies below their 200 day moving average, maybe we should all be buying more Warrior Met Coal. This company could easily fit at the top of anyone’s buying program. Every share purchased at $50 should be bought with the confidence that within a handful of years the price will reach $125.

JAKKS Pacific (JAKK)

JAKKS reported full year 2024 earnings per share of $3.79. Not too bad for a company that was $18.02 when I wrote about it on July 2nd of 2024. On the earnings announcement, the stock price sold off from $35 to $30 per share, disappointing, but this market is looking for things to sell.

EPS for 2023 were $4.62, so the $3.79 is a bit of a disappointment, but the key to understanding JAKKS is to understand the children’s movie cycle. Disney’s Wish was a flop, and it was released in the Fall of 2023. After initial release, the film moves to streaming the next spring. It is when a movie moves away from the theatres and into people’s homes that it drives the merchandise sales. Disney’s Wish was still affecting full year 2024 earnings.

Looking forward, Moana 2 and Sonic 3 were huge successes. And those films were released in the Fall of 2024 and will be streaming this upcoming Spring of 2025. So we can expect JAKKS to have a pretty substantial increase in earnings for full year 2025 over full year 2024. The next time Disney makes a hit, like Encanto in 2021, EPS could easily be over $10 for the year. But until then, the next three years should have EPS in the $4 to $5 range, unless I am underestimating Sonic 3 and Moana 2.

Management initiated a $0.25 quarterly dividend. That’s about 1/3rd of JAKKS net income, and 1/5th of their EBITDA. The rest of the cash flow will go toward rebuilding their cash stockpile after the sudden redemption of the preferreds. Would share buybacks have been better? Maybe, but the price to tangible book is 1.37x, so I can’t hate on management too badly for choosing dividends over buybacks.

Growth should come from Europe, South America, and a new licensing agreement to produce Minecraft costumes. JAKKS still is an organic growth story, and in a capital light way. But the upside potential is limited here. At best, JAKKS could return to a price to sales ratio of 1.0x, which is only a double from here. I am considering selling calls until the position is called away from me, the deep value was to be found last summer when the stock was trading at $18. Is the Minecraft Movie in April 2025 going to be a hit? Do I really want to own JAKKS until Frozen 3 is released in November 2027?

Materialise (MTLS)

On my writeup for MTLS just a few days ago, I mentioned how their Q4 earnings are likely to be weak due to capex for the US expansion. I had no way of knowing that the stock would sell off by 40% on those earnings!

“Management is predicting weaker results for next quarter due to the capex for their US expansion. As a value degen, short term bad, long term good, is within my comfort zone.”

I am genuinely shocked for a company that had GAAP positive net profit in the quarter and the full year, which doubled over the previous year, sell off by 40%. But that’s what makes a market.

The biggest lesson that I keep learning again and again is to size the initial position small, and to leave room to add to the position. Nothing has fundamentally changed about MTLS to invalidate the thesis, the medical segment is growing at 14.3% annually with 30% margins, and the US expansion will accelerate that.

Thank you. Looks like I have a lot of catching up to do! The main reason I subscribed was because we are interested in so many of the same stocks. I must also say, I very much like your style of writing and analysis.

Thank you for these great macro and wider market insights Steve. Was wondering why I had been taken out to the woodshed…