Baby It’s Cold Outside - Natural Gas Edition: PHX Minerals $PHX, and Blackstone Minerals $BSM

Hey ChatGPT, can you create a satire of “Baby It’s Cold Outside,” but as a conversation between a retail investor and a natural gas company?

I really can’t stay—

But baby, it’s cold outside!

Been burned twice this way—

This winter’s a bullish ride!

My portfolio’s been such a mess...

But forecasts show snow, no less!

Two warm winters in a row—

That streak’s over, don’t you know?

My friends will think I’m unwise—

Natural gas futures don’t lie!

The price could just crater again—

Supply's tight, we’ll win in the end!

The charts don’t look that great—

But baby, just calculate!

Maybe I’ll buy... one share more—

That's the spirit, open the door!

I simply must go—

But baby, it’s cold outside!

The markets could blow—

This forecast’s your trusted guide!

This risk might be far too extreme—

Oh, but just picture that gleam!

Two winters burned me before—

This one’s primed for profit galore!

I’ve got to resist the hype—

But demand's just the bullish type!

Okay, maybe just a small bet—

Now you’re on the right track, don’t fret!

This better not fail—

Oh baby, it’s cold outside!

I first started getting interested in natural gas after the start of the Ukraine War. To the relief of Europe, there was an unusually warm winter that year. What are the odds of two warm winters in a row? I asked myself at that time. Pretty good actually, Europe had two warm winters in a row. What are the odds of three warm winters in a row? I said to myself while laughing in the face of the gambler's fallacy. (The gambler’s fallacy doesn’t apply here, most natural forces are not independent events, but have a mean-reverting tendency.)

Well, we might just be having our first cold winter in three years. Europe is depleting their gas reserves at the fastest pace since 2016, and Dutch TTF prices have doubled off of the February lows. Henry Hub is up over 50% in the last six months, and forward prices are starting to adjust upwards as well. If these forward prices continue to rise, then natural gas producers can lock in derivative hedges to ensure their profitability for years into the future. This price relief is coming just as old hedges are rolling off after Henry Hub spent the last two years frequently flirting with $2 prices.

I had previously written about Blackstone Minerals (BSM), a limited partnership focusing on mineral rights with ownership of huge acreage, especially in East Texas. If you don’t mind the tax consequences of owning a limited partnership, BSM is still a fine way to own exposure to these rising natural gas prices. Their strategy is to own so much land that drillers have to commit in advance to a certain volume of drilling. During this last two year bear market in natural gas, however, we did see one large operator in the Haynesville produce below their commitment. BSM cut the dividend, but it is still above the 10% threshold for my “Probably Not a Value Trap” series.

Drill Baby Drill, or Else: Black Stone Minerals $BSM

Welcome to the “Probably Not a Value Trap” series where I discuss businesses with a 10%+ dividend yield which I believe probably won’t get cut and why, but don’t come after me on Twitter if they do.

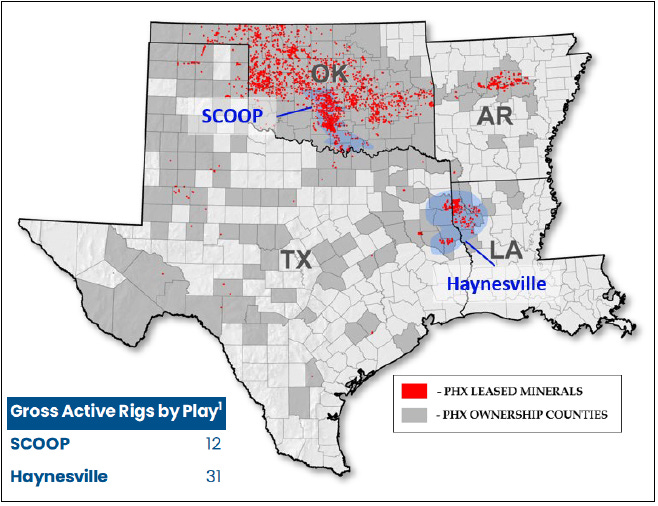

But, if you prefer something smaller, something with a bit more potential torque to natural gas prices, and you don’t need an enormous dividend income yield, Panhandle Resources (PHX), now rebranded to PHX Minerals is very interesting. The typical small mineral rights company does not know where operators are going to drill next. In order to make sure that they have at least some income in the near term, the strategy is to scatter purchases across the bingo card, so that no matter where the operator drills next, at least some small amount of income will be coming in soon. PHX, doesn’t do this, instead they use their own team of geologists, as well as their board of directors who are mostly former executives of the operators, to try and predict which parcel will be drilled next, and to concentrate mineral rights purchases in that spot.

This strategy has worked well enough that total production on PHX’s acreage is up 10% year over year, despite soft commodity prices and their focus on the Haynesville and Anadarko shale basins which are almost entirely natural gas. If they can have volumes up 10% year over year on these last terrible twelve months, imagine how well they can do when natural gas volumes need to ramp up to supply the cold winter, new export terminals, and the Artificial Intelligence electricity demand. That’s one heck of a management team. PHX also has one of the strongest signals of incentive alignment possible, insider buying from the CFO. There is insider buying from the CEO as well, but CEOS benefit from being overconfident. The CFO, on the other hand, is a pessimist by nature, and if he is buying, I will always give the company a hard look.

PHX might not be everyone’s favorite fossil fuel company of choice with 80% of volumes as natural gas, 11% as oil, and 9% as natural gas liquids. The Haynesville and the SCOOP really are gassy basins. But if you believe that natural gas is the energy transition fuel of choice due to its low carbon dioxide emissions, then you might find PHX to be very interesting. With natural gas having the nickname “widowmaker” due to the extreme volatility, PHX should give you plenty of opportunities to enter and exit over the years if you are nimble. But it also probably wouldn’t be terrible to buy and hold with a solid management team and proper incentive alignment. PHX has been growing production volumes by 28% annually since 2020, and reserves by 36% annually since 2020. Although acquisitions are slower in 2024 due to the challenging commodity prices, PHX paid their dividend and even retired about 15% of their outstanding debt.

The key to PHX’s growth is their small size and their willingness to engage in very small acquisitions. Since 2020 management closed on 86 different acquisitions with an average size of $1.6 million. This small deal size typically means that the purchase price is lower, and the internal rate of return higher than what a larger company can accomplish. The CEO even moved the corporate headquarters from Oklahoma to Houston in order to be closer to the deal flow and have better access to these smaller mineral rights.

While PHX trades at $3.97, at current commodity prices, their proven and probable reserves are worth about $6.59 a share. At $80 crude and $5 natural gas, however, PHX would have a net asset value of $10.02. That’s a pretty steep discount for a rapidly growing reserve base and production.

Consistent with what management from ProFrac Holdings (ACDC) said on their last earnings call, activity in the Haynesville is picking up. PHX’s management disclosed that last quarter there were 166 wells waiting for completion on their acreage, up from the low six months ago of 128. The number of drilling rigs is up from 8 to 10 over this same period, and the number of drilling permits submitted is 102 up from 94.

PHX’s stock price has already rallied up from the August lows of $3.11 to the current $3.97. And this rally was on improving fundamentals, the stock price didn’t move much yesterday on the rising Henry Hub despite the 10-day meteorological forecast finally showing a major polar vortex event for the middle of January. One of the best things about small caps is that they are so inefficient that often the price doesn’t move with the underlying commodity. It’s great that we can be just a bit late and still have great opportunities. Of course this can come back to haunt you when you are looking to exit, and the price stays inefficient. Either way, PHX Minerals is an interesting small cap mineral royalty with a concentrated focus on natural gas, an aligned management team, and a lot of potential macro tailwinds.

Curious, what are your thoughts on PHX running a strategic alternatives process and the whole WhiteHawk thing?

Isn't VET also natural gas play? I am assuming this one has higher torque due to the small size. How would you split allocation if one were to basket these two for NG play?