Already a Double, Is There More Gas in the Tank for SoFi Technologies? $SOFI

Thank you for your forbearance these last few weeks as I fell into a bit of a publishing lull. I will be returning to a more diligent writing schedule until mid July when I have a family vacation for a few weeks.

I am finding it difficult to maintain correspondence with so many subscribers. If you have sent a message or left a comment, I will be doing my best to clear out my inbox. It’s a happy problem that I can’t handle the volume of inbound communications, better than the alternative at least.

For the rest of the summer, I will be mixing new writeups alongside re-underwriting old theses to see if any facts have changed. In order of gut feeling, I am starting with SoFi Technologies (SOFI).

I first wrote about SOFI in September of last year when the stock price was $7.52. Today it sits at $13.30, down from $18 at the recent peak.

Chamath’s best performing SPAC: SoFi Technologies $SOFI

Hello and welcome back old friends and new friends. Many of you are onboard with the commodity supercycle thesis, or the “revenge of the old economy.” My portfolio is chock full of the periodic table of the elements. But I have a sinking suspicion that there is a possibility we will see the revenge of Cathie Wood as well, or instead, or first, or after, I don’t know the timing. But I do know that a lot of very interesting small caps crashed into 2022, their fundamental businesses have improved for the last two years, and the stocks can’t catch a bid. At some point that trend will change and the fundamentals will overcome the sentiment.

SOFI is a neo bank, a fully online savings and loan with no physical branches. That idea seemed more revolutionary before Covid, but in 2025, it feels like a bit of an inevitability. I suppose I will be able to tell my grandchildren someday about phones that were attached to walls, full-size spare tires in the trunk of 8-cylinder rear-wheel drive cars, and physical bank branches with lollipops and pneumatic tube transport systems. Traditional banks have been slow to compete through technology, and this has given SOFI an opportunity to take market share in the relatively stodgy and mature market of banking. Will they achieve their goal of becoming a top ten financial firm? There is a path to get there.

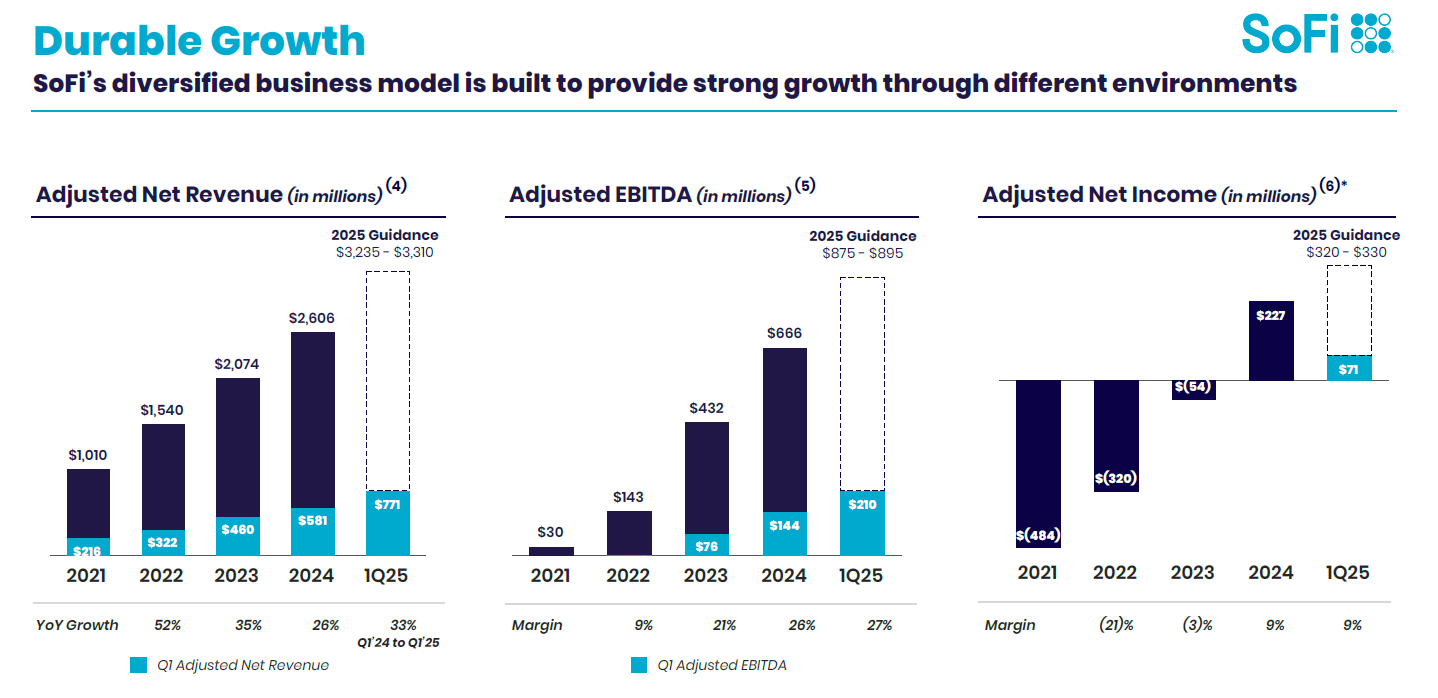

The growth strategy is two dimensional, acquiring more customers, and adding on more products. Acquiring customers is easy to measure, and has been progressing well. But expanding the breadth of offerings to make those customers sticky and to increase total lifetime customer revenue is much harder to measure. Since last September, SOFI has been burning the candle at both ends. When I wrote about them last September, they had added 600,000 new customers that quarter to reach 8.7 million. This last quarter they added 800,000 to reach 10.9 million. The customer growth has accelerated, but the rate has slowed as a percentage from 52% annually a few years ago to 34% year over year. It’s a mathematical inevitability that the growth rate of new customers will have to slow someday, but SOFI probably has several 20%+ customer growth years still ahead of it. In the most bullish scenario, the CEO, Anthony Noto, has a dream of reaching 50 million accounts within five years, but there’s little value in putting price targets that high.

The improvement in breadth of offerings is harder to measure. SOFI provides a measurement of how many new products they added to their roster, 1.2 million last quarter, bringing the total to over 15 million products. The story of George Washington Carver makes me a little skeptical about using internal measurements of product breadth, about one third of his 300 uses for the peanut were minor variations, fourteen different kinds of peanut-based paint, etc. But increased product breadth should show up in increased profitability. SOFI has profitability, this is their sixth consecutive quarter of GAAP net income profitability, but they don’t have increasing profitability yet. Net Income was $71 million last quarter, but it was $77 million in Q1 of 2024; the profitability inflection has yet to arrive. For the moment, SG&A is chasing revenues, and winning, but that could represent increased marketing spend which would benefit future quarters.

Tech companies have the ability to switch from growth mode to profit mode, but as an investor, we have no idea when Anthony Noto will flip that switch. Uber went from losing $10 billion annually in 2022 to making $10 billion annually in the trailing twelve months. Both research and development as well as marketing come out of the accounting statements before net income, so it is easy for a tech company to operate with very little GAAP net income while they are growing and innovating.

I hate using adjusted figures, it’s not a good habit to be too trusting of management. But in order to tease out R&D and marketing, I am relying on adjusted net revenue. SOFI has been on a relatively steady fourteen year journey, and they are predicting the inflection to increased profitability to start this year with between $320 and $350 million of net income, but to really escalate in 2026 with earnings of between $650 million to $950 million. The market is forward looking, and it is always hard to know just how forward looking it is. But I would want to own SOFI at least six months before 2026, which is right about now.

As a value investor, it’s hard to want to buy something at a price to earnings of 45x, which is where SOFI is for 2025 based on management’s guidance. But based on guidance for 2026 earnings, the price to 2026 earnings ratio is somewhere between 30x and 15x. Revenue growth has been in the 33% range for this last year, and management is guiding for it to continue along a 20% to 25% path for the medium term. Looking at price to sales, SOFI comes in at 3.77x, but for a tech company with sticky recurring revenue and that amount of growth, I would expect a price to sales of between 6x and 8x. If growth stabilized below 20%, a 4x to 6x price to sales ratio would be more justified, but at their current growth trajectory, SOFI is selling for about half of where a typical tech company would trade.

If the multiple expansion never comes, as long as there isn’t multiple compression, it’s hard to sneeze at a company that is growing 33% year over year. Without a multiple rerating, two years of 20% growth would put SOFI at $22.41 based on a 4x price to sales ratio. If the multiple expansion does come, and SOFI trades at an 8x price to sales on 2027 revenue, then SOFI would be a $44.82 stock in two years.

There are two major bear arguments against SOFI. The first is that legacy banks will innovate and compete with SOFI for the online marketplace, and the second is the quality of their personal loan portfolio. Regarding competitive pressures, unless traditional banks are undergoing a new wave of innovation, SOFI has been competing against them successfully for many years. Regarding the quality of their loan portfolio, at the moment SOFI packages and resells the large majority of their loans, they are able to originate far more than they can carry on their books at the moment. Tangible book value grew by over $1.3 billion in 2024, and management is guiding for tangible book value to grow by at least $500 million this year. But SOFI originates tens of billions of dollars of loans every year, more than they could possibly keep on their own books.

SoFi Technologies (SOFI) $13.30: $22.41 by the end of year 2027 base case

SoFi Technologies (SOFI) $13.30: $44.82 by the end of year 2027 bull case