AI and Nano Fluids in the Shale Patch: Flotek Industries $FTK

Some of you have suffered along with me as an investor in ProFrac Holdings (ACDC). It has been a bumpy ride with more downs than ups, but I am still holding, and I am still optimistic about the future. I first wrote about ACDC and their ambitious frac services rollup here:

The ballad of $ACDC, why ProFrac Holdings is a green AI story that could easily triple in the near term.

Edited 11/2/2024: Operating cash flow for 2Q 2024 was $113 million. They did indeed do that acquisition in Midland, Texas. I was early on this one, but I think it has a high probability of inflecting going in to 2025. There is still a good chance it will be the victim of tax loss harvesting for the last two months of 2024. With the Permian Basin ba…

As well as their recent share price weakness here:

Stairway to Heaven or Highway to Hell? ProFrac Holdings $ACDC

The market has been very unusual this past quarter. Realized volatility is outpacing anticipated volatility by so much that the buyers of options are making more money than the sellers of options. For the entire history of the options market, this has never happened before. On average, options are a transfer of wealth from the buyer to the seller, but l…

An aspect of that rollup that I had missed was an equity stake and board representation in Flotek Industries (FTK). This type of arrangement is referred to as a toe hold, and toe holds can be a very strong signal of future success. Toe holds are commonly used when a smaller company has a management team that still wants to grow their business under their own initiative, but they recognize the benefits from a strategic partnership. The larger firm provides advice, relationships, and helps in a variety of other ways as well, with the implicit understanding that when the time is right, the larger partner is standing by ready to acquire it.

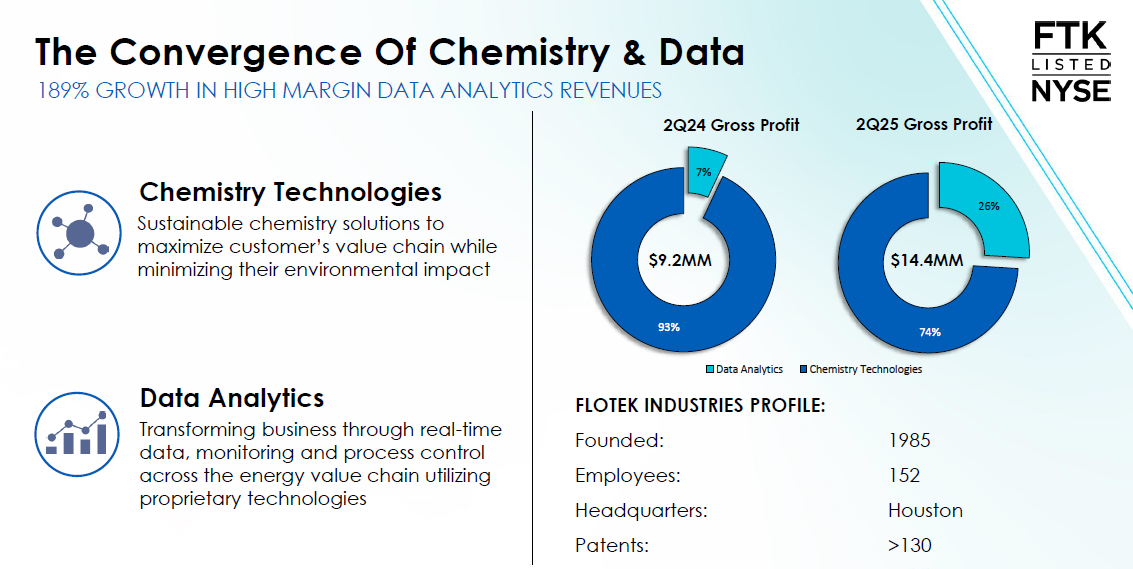

Flotek is a frac services company in two parts, data analytics, and chemical solutions. The chemistry side has over 130 patents covering many products, but their most important product is their Complex nano Fluids, CnF. In a 425 well study, Flotek’s CnF increased oil yields by 22% to 32%, and decreased the amount of water and frac sand used by 50%. It works by making the oil more water soluble, more able to be extracted from the rock, and more able pass through the rock formation without clogging it. In one controlled trial, CnF generated an extra 14,000 barrels of oil per well in the first three months at an incremental cost of less than $1 per barrel.

The data analytics side of the business provides data as a service to subscribing customers, allowing them to get more cost saving efficiencies out of their frac fleets. A combination of sensors, software, and AI turn gas quality and equipment performance data into actionable reports and alerts. This boosts production and reduces downtime as equipment failures can be detected before they become catastrophic and potentially damage adjacent hardware. It is also complementary to the chemicals business, as the live data stream informs what quantity of CnF is optimal for the geologic formation.

The data analytics extends beyond just frac fleets, it can add value at every stage from the drilling rig to the oil refinery. And maybe more importantly, it can monitor power generation equipment, which makes it a cost saving and emissions saving initiative for the Permian data centers which will operate on associated gas.

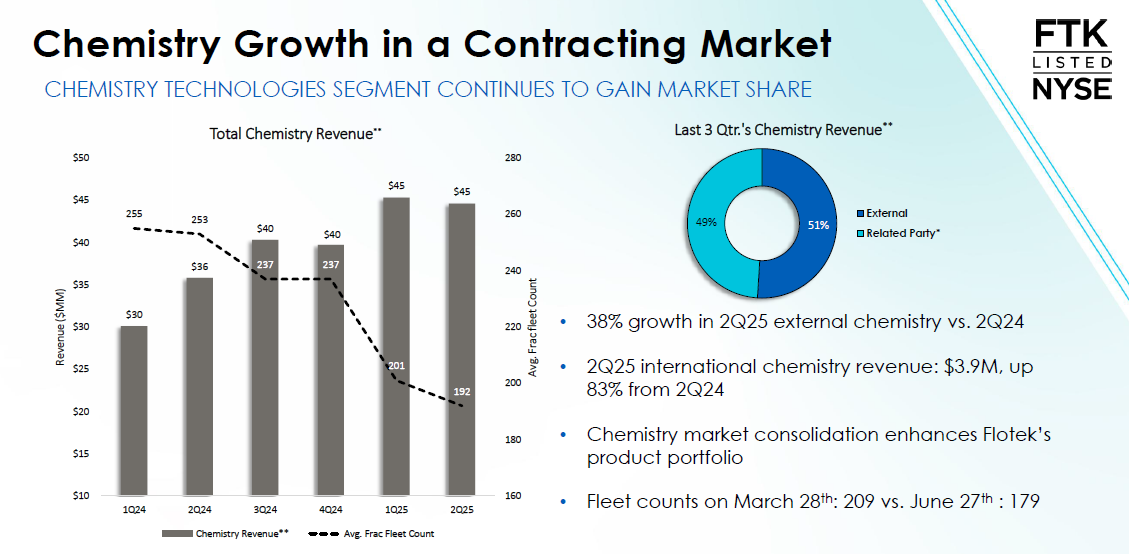

The data analytics business has only just begun to take off, with 189% revenue growth year over year in Q2. It went from 7% of revenues to 26% of revenues in twelve months. Meanwhile the chemistry side of the business also grew at a 26% annual rate over that time period, while the frac fleet count fell from 253 fleets to 192. Clients are searching out for cost saving initiatives, and Flotek’s CnF is taking significant market share.

I wouldn’t go so far as to claim that frac chemicals are counter cyclical. It’s just that Flotek is growing enormous market share at the same time as the market is shrinking. In the next boom, clients aren’t going to suddenly turn their backs on an extra 14,000 barrels of oil per well at an incremental $1 per barrel of oil. I would expect volumes and market share to keep increasing into the next frac boom, unless growth hits a wall of competition.

Doing some back of the envelope calculations, if related party revenue (ProFrac Holdings) is about 50% of total revenue as of Q2 2025, and the frac fleet count was 192 at the time, then Flotek currently serves probably less than 25% of the market. They have room to take more market share, but they are competing with juggernauts like Schlumberger and Baker Hughes who have their own patented chemicals. I have no way to measure the competitiveness of Flotek’s CnF against Baker Hughes SpectraStar, for example, but the 26% year over year chemicals revenue growth is a good indication that Flotek does indeed have a technological advantage for the moment.

One major roadblack to growth, however, is that most of ACDC’s competitors are large, and have an explicit strategy to not rely on outside vendors. Schlumberger and Baker Hughes might stay with an inferior internal product in order to guarantee total control and speed of execution. This could be one of the reasons why Flotek’s growth strategy is to focus on the data analytics side of the business.

The data analytics business can extend far beyond just the fracking stage, for example, Flotek has just recently received EPA approval for their patented JP3 flare monitoring system. A well might only be fracked for three to seven days, but a Bakken well might be flared for three months or longer in some cases. It also is a much larger international market. There are somewhere in the neighborhood of two to three thousand wells being flared in the US at any given time, but worldwide that number is over 50,000 wells.

Also, as electricity prices increase and diesel prices stay strong, there is more of a focus on on-site power generation. The market for data analytics to monitor natural gas power generation and flow metering is enormous and growing, with somewhere near a $5 billion addressable market. There is stiff competition in data analytics in the form of Honeywell and Emerson, and I have very little ability to gauge the competitiveness of AI software offerings.

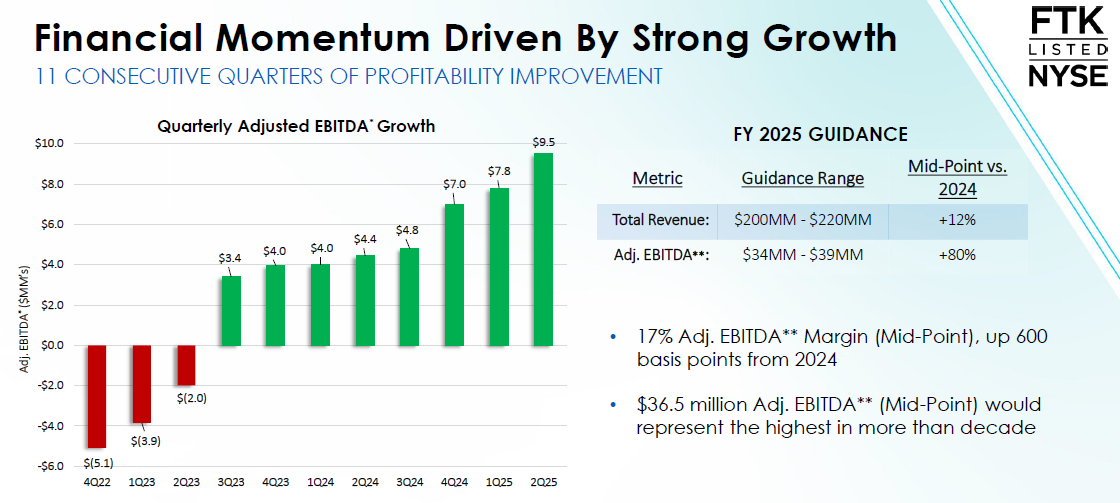

Flotek management is guiding for continued growth, but guidance was updated last quarter, and the growth for Q3 and Q4 is not as aggressive as it has been in the trailing 12 months. Management is guiding toward $200 to $220 million of full year revenue, but the trailing twelve month revenue is already $214 million. Full year 2025 adjusted EBITDA is projected to be between $34 and $39 million, but Q2 adjusted EBITDA was already $9.5 million. This guidance would indicate a serious growth slowdown, however, the new CEO who started in 2023 is apparently an expert in sandbagging, having beaten GAAP earnings guidance for the last eight consecutive quarters.

Perhaps the most important part of guidance is the projection for data analytics to be 60% of EBITDA for full year 2026. And data analytics revenue is recurring and sticky. As an AI driven SaaS company, the data analytics segment has 189% year over year revenue growth and 63% EBITDA margins, putting it squarely beyond the threshold for a Rule of 40 company. This type of Rule of 40 score would typically fetch a 6x to 8x price to sales ratio. With $16.3 million in data analytics revenue in the last twelve months, the market capitalization of a pure data analytics company would be between $100 million and $130 million. Flotek’s current market capitalization is $430 million with an overall price to sales ratio of 2.01x.

Flotek doesn’t appear cheap by most valuation metrics, and it’s hard for a value degen to put a price tag on a rapidly growing AI company. But it is in a unique positive given their patent portfolio, anchoring backlog from ACDC, and recent aggressive growth. It is also interesting that for the last five weeks, the frac fleet count has been growing from the low of 162 fleets in August to 179 fleets last week. Could the frac cycle finally have turned? It’s a real possibility.

The two business units combined are only predicted to have a 13.5% revenue growth rate for the next two years. The market might be pricing in a much more aggressive growth rate due to recent performance, some of which was caused by a drop in revenue from 2023 to 2024. The two year revenue growth rate is much more humble than the one year growth rate. And while ACDC’s business provides a healthy backlog to provide stability, having 50% of revenue from a single customer is considered a major risk. But even with slow revenue growth, Flotek appears to have reached scale and under the new CEO has eleven quarters of sequential EBITDA growth.

I am hoping for a pullback in the stock price, but given the growth in the frac fleets deployed, a pullback might not be coming. Their data analytics business can’t be rolled out quite as quickly as a typical SaaS business, because Flotek needs to deploy the sensors and hardware as well. A traditional discounted cash flow model would anticipate a 2028 end of year share price of $20.47, which is not incredibly attractive given the risks involved and the current share price of $14.43. People buying Flotek today must be anticipating growth far in excess of current guidance, or they must be happy with earnings a 12.36% annualized return.

Given the sandbagging nature of the CEO, and the five week growth in frac fleets, growth in excess of guidance is very possible. It’s not a terrible lottery ticket on the frac ecosystem, but it’s also not an aggressively undervalued company. In a situation like this, I like to buy a tiny placeholder position so that I can watch for dips. If the dips never come, at least I own some and can be happy that I own a winner. If the dips do come, I own so little that I am happy to add more.

Given the exposure to AI through the data analytics component, as well as exposure to the data center buildout to service the natural gas power generation, Flotek has the capability to reach absurd valuations. But I am at a loss to put a price target on the absurd.